A Journey to ETHDenver #1 Mimicry Finance - A Market to Short / Long NFTs

This is the first project in which we started this series, and it looks like an interesting NFT derivatives trading market, but also fragile.

This is the first project in which we started this series, and it looks like an interesting NFT derivatives trading market, but also fragile.

What is Mimicry Finance?

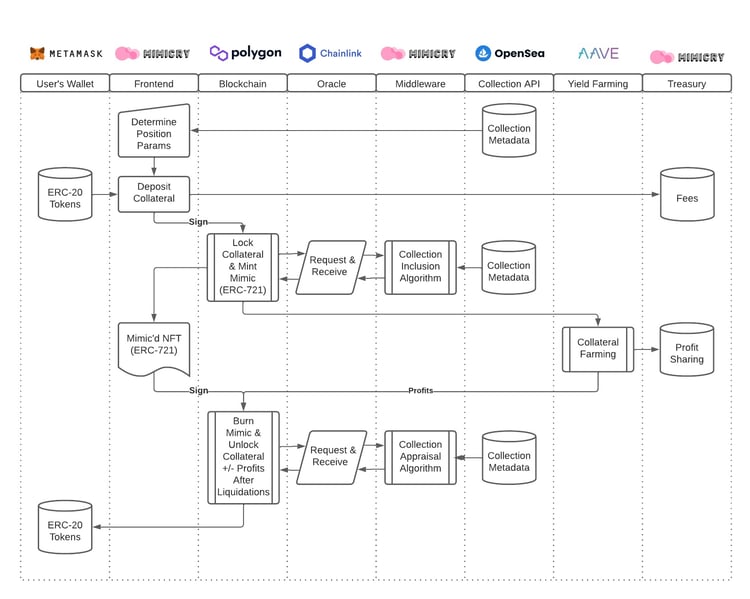

Mimicry Finance is building a derivatives market on Polygon for NFTs. It takes the floor price of NFT from NFT trading platforms such as OpenSea via an Oracle, and feeds it to the platform for users' long/short trades.

Mimicry Finance Architecture, Source: Mimicry Finance

Mimicry Finance is inspired by Synthetix and uses the same structure as Synthetix for its trading model, where all users trade against the protocol pool.

By using Mimicry, users need to deposit their collaterals first, which gives them the right to mint a Mimic (an ERC 721 token), representing the position owned by users. The minting is a process that a user trades against the protocol's pool. All mimics outstanding are positions that are opened by users with their collateral. Users are able to close their positions anytime with Oracle price feed. Closing positions is the same thing as repaying the debt to the protocol and getting back collaterals.

Synthetix minted synthetic stablecoin sUSD by overcollateralizing $SNX, and then users freely trade sUSD into other synthetic assets, such as sBTC. The price of the synthetic asset tracks the actual price of the asset and the user's losses/gains change based on the price asset movement. At any time, the user can sell the synthetic asset to the protocol, exchange it back to sUSD, and then to $SNX.

The key thing in Synthetix is the concept of shared debt pool, where a single user holds sUSD, but if other users' synthetic assets go up in price, then the total debt also goes up, so users who do not hold an average percentage of rising assets actually lose money because all users share all debt in the same proportion as they did at the beginning.

Conversely, if the price of synthetic assets held by other users goes down, that means that the total debt of all users to the protocol also goes down. Thus the amount of money that each person has to pay back to the protocol becomes less, and users who are holding stable coins that are not operating actually make money.

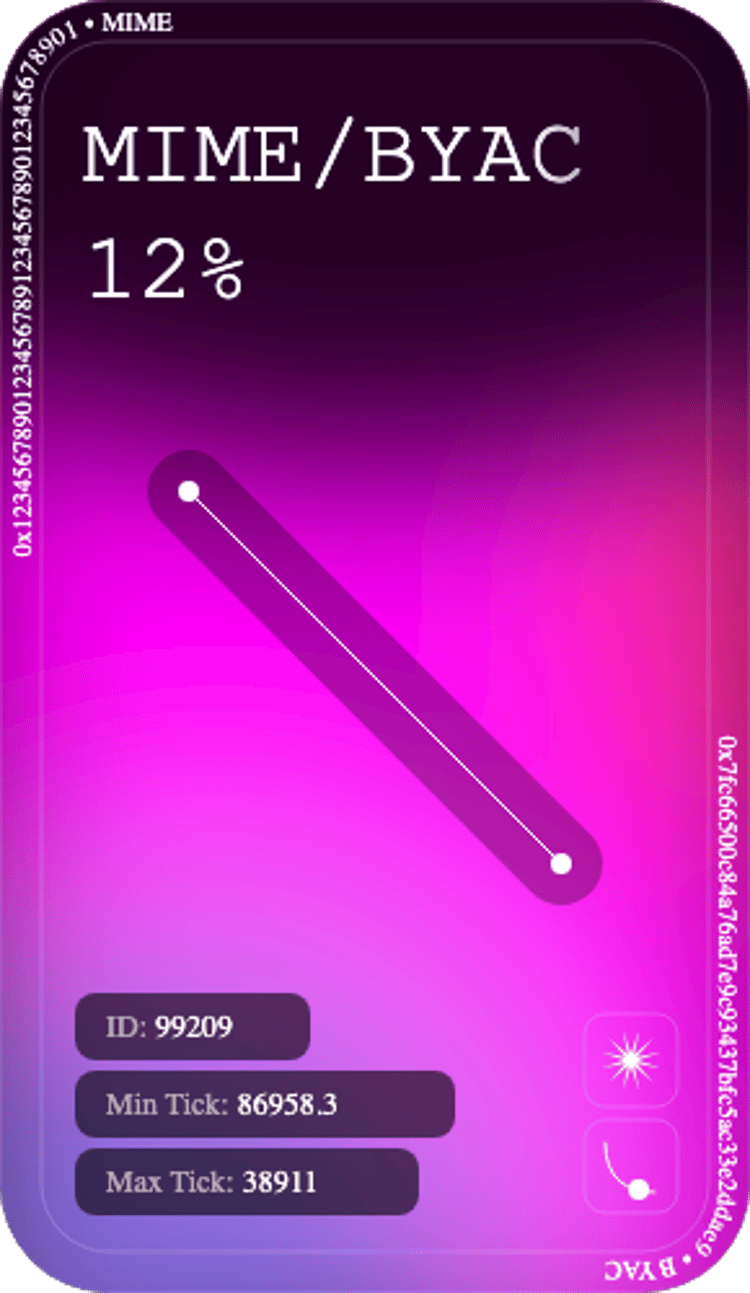

The same applies to Mimicry Finance, where users mint USDm, a stable coin, by staking their own Token $MIME to the protocol, with an initial collateralization rate of 800% (Ratio may be different for other kinds of ERC20s). Users can then use USDm to mint Mimics. Each minted Mimic will contain specialized metadata written to the blockchain. When rendered within a wallet, that data, along with real-time performance information, will be visible in the NFT itself. Some of the data recorded will include:

- The type of ERC-20 collateral deposited, including contract address

- The amount of deposited collateral

- The NFT collection to peg value against, including contract address

- The direction of the price peg (standard or inverse)

- The collateralization ratio

- The time that the position was opened

- The percentage-based gains or losses, relative to USD, if the position were to close right now

A visualized BAYCm, Source: https://docs.mimicry.finance/protocol-architecture

Since opening a position (minting a mimic) and closing a position (burning a mimic) by users are both transactions that go against the protocol pool, there is no slippage at all and the process is always liquid.

Protocol fee

For every transaction in the protocol, there will be a fee of 2.5 bps charged. All the fees will be collected to a fee pool, belonging to communities of Mimicry. So I assume that there will be some staking stuff for users to be able to claim the fees.

What are the risks?

The usual risks that a typical project has, Mimicry has all of them. For example, contract security, the death spiral that can occur with synthetic/algorithm-based stablecoins in a down market, etc. Mimicry also faces the risk that the price fed to the platform will be manipulated, and that risk is significant.

First, NFT trading is inherently an illiquid market. Doing derivatives trading on an illiquid underlying inevitably leads to vulnerability in derivatives trading. In turn, manipulation of the Oracle price / or index price (generally referred to as Mark Price in perpetual contracts) consists of two main scenarios.

- Wash trading to manipulate the price fed to Mimicry.

- Other types of Oracle risk, like downtime, latency.

Closing Thought

This article is just an introduction to Mimicry Finance based on the information available so far, and I hope it will help interested readers to see and understand the project. We will continue to follow up on the ETHDenver series of projects. We will also continue to follow the development of these early-stage projects, and welcome you to download the TokenInsight APP to get the information first.

NFT

Derivatives

DeFi

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open