Aave V3 is Live. Do You Still Believe in DeFi?

Yes, I do.

Yes, I do.

Aave is one of the largest lending protocols in the DeFi market, launched in 2020. Based on the lending mechanism of Compound, it introduces 'flash loan', namely a form of unsecured loan which is done by one block (a transaction). Meanwhile, Aave is deployed multi-chain, with Aave V2 has been launched on Ethereum, Polygon, and Avalanche.

On March 17, 2022, Aave announced the deployment of V3, and is now live on Arbitrum, Avalanche, Fantom, Harmony, Optimism, and Polygon. As of March 18, 2022, the fully diluted market cap of Aave ranks #54 on TokenInsight ($2.42b) with a TVL of $18.83b.

What are the main problems of Aave V2

Low capital efficiency

- The overall liquidity of Aave crossing different networks is close to $20b, but most of the funds are sitting idle in the protocol smart contracts.

- For the sake of security, Aave's asset risk parameters are set conservatively. Because under the V2 model, users can borrow any asset by depositing a supported collateral asset. This means, when listing a new collateral asset, the whole protocol is exposed to it.

- The majority of Aave's assets are concentrated on Ethereum. The high cost of the network can lead to high costs for users. Further, the oracle will also be affected by the high latency.

- On Aave, users' position (eg. total collateral value) is measured in a unified unit, such as ETH. Thus, the user's position might be fairly fluctuated, which would also limit the user's borrowing ability.

User experience to be improved

As a protocol built on multiple chains, it is crucial for Aave to support the asset transfer between different chains.

Inadequate risk management

The V2 protocol has limited risk management and more measures are needed, such as protection against Infinite Minting and Oracle Manipulations.

Inefficient community governance

A community that is fully controlled by the voting governance may affect the governance efficiency of the protocol, so some entities should be set up to deal with part of the protocol’s operations, such as new assets listing.

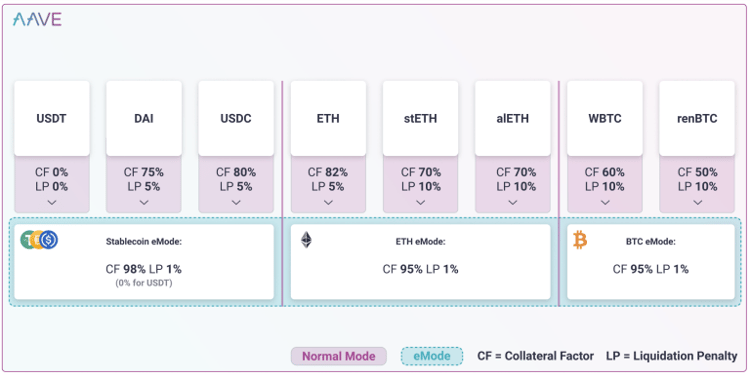

E-Mode(Efficiency Mode)

E-Mode is designed to solve the low capital efficiency problem. Under this mode, assets on the market are classified. And these assets are usually highly correlated in price, such as stablecoins, ETH & ETH staking derivatives, and so on. Generally, Aave claimed that assets in the same category will share a set of risk parameters, and users should enjoy higher borrowing ability when borrowing between these assets, such as higher CF (Collateral Factor) or LTV (Loan-to-Value), and lower liquidation penalty (Liquidation Penalty).

Example1:

The category, 'Stablecoins' contains USDT, USDC, and DAI. The CF for them is 97%, the liquidation threshold is 98%, and the liquidation penalty is 2%. Thus, users deposit $100 USDC as collateral and can borrow $97 DAI or USDT.

However, in the normal Aave market, users can only borrow $80 worth assets against $100 USDC.

(ps: Users can choose to use E-Mode or normal mode, and can switch freely when the position is risk-free.)

来源:Aave

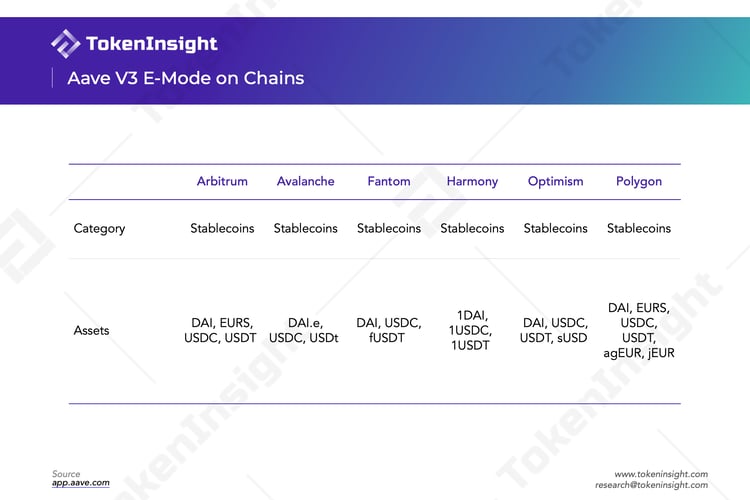

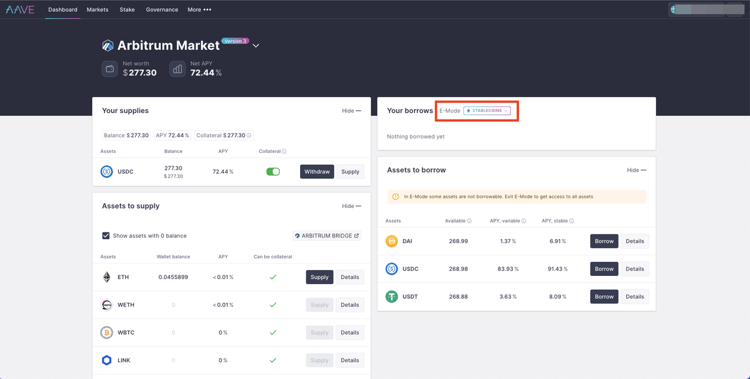

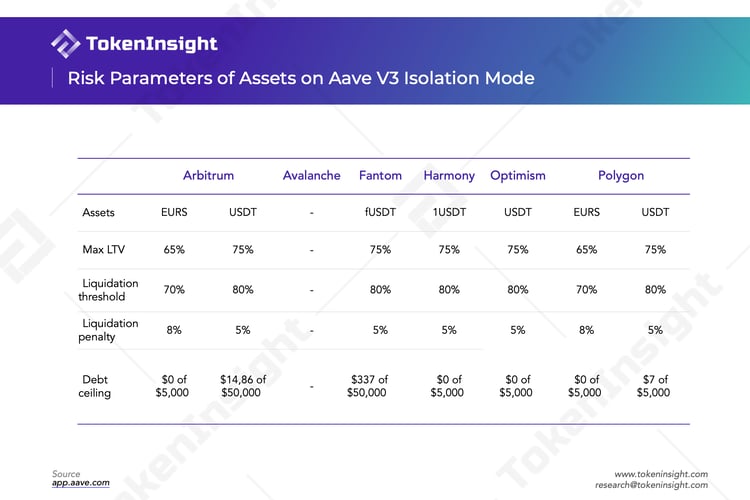

For now, Aave V3 only supports only one category of "Stablecoins", and detailed supported assets for each chain is as follows.

Currently, under the E-Mode mode, users can borrow DAI, USDC, and USDT by staking USDC on Arbitrum, and the Collateral Factor is about 97%.

来源:Aave

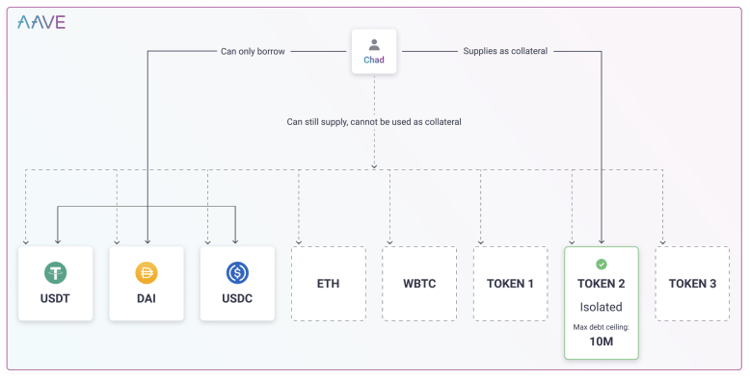

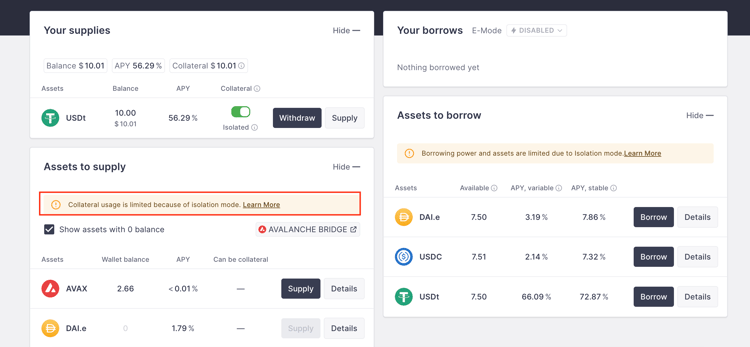

Isolation Mode

In V2, once the community lists a new collateral asset, it means that users can leverage this asset to borrow any asset on the protocol. Thus, the whole protocol could be affected or even be riskier by this. As a result, Aave introduces a Isolation Mode, in which users supply isloated assets can only borrower limited stablecoins with a maximum amount (similar to MakerDAO's debt ceiling).

来源:Aave

Example2:

As shown in the figure below, when users deposit Isolated Asset (USDT), they can only lend out several stable coins (DAI.e, USDC, USDt), and can only mortgage and lend 75% of the value of the asset.

Debt Ceiling for an *Isolated Asset* is represented as the maximum amount in USD that can be borrowed against the collateral with two decimals of precision.

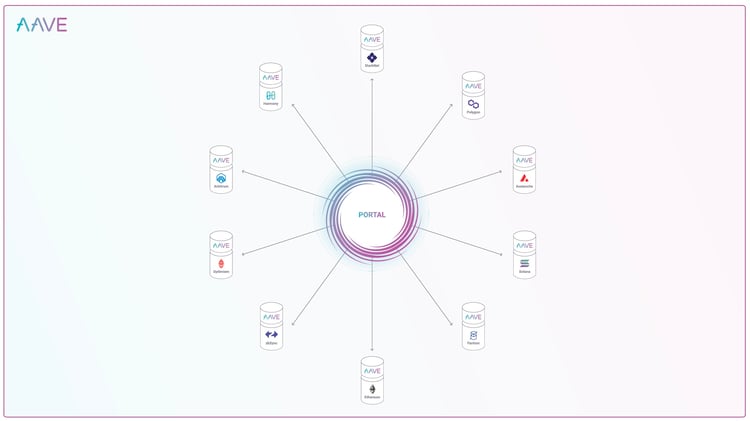

Portal

By partnering with third-party cross-chain bridges, Portal allows users to transfer their position between Aave's marketplaces. When the user submits the need to transfer assets, the aToken in the original market will be burned, and then a new aToken will be minted on the target network. The underlying assets of aToken will be transferred later through a third-party cross-chain bridge, which has a certain lag.

aToken is the user's deposit certificate. For example, if the user deposits ETH, he will get aETH as the certificate. And ETH is the underlying asset of aETH.

来源:Aave

At present, the Portal function is not live yet, but the new Aave interface contains access to the third-party cross-chain bridge, which is fairly convenient.

来源:Aave

Risk Management

To secure the safety of the protocol, the Aave V3 contract has been audited by several institutions, including Certora, Sigma Prime, Trail of Bits, Open Zeppelin, ABDK, PeckShield, etc. In addition, the protocol has adopted more sophisticated risk parameters and features to againts potential insolvency:

- Supply and Borrow Caps: how much an asset can be supplied or borrowed.

- Risk admins: Setting a special entity to adjust the risk parameters of assets without community voting.

- Variable liquidation close factor: In the past, the agreement could only liquidate 50% of a position, but now it is possible to liquidate more, or even all of the collateral.

- Granular borrowing power control: At present, most protocols in the market must liquidate some users' positions if they want to reduce the borrowing power of an asset (for the protocol perspective). However, in Aave V3, the protocol can achieve it without affecting existing users.

Example3:

Suppose the current LTV of $TOKEN2 is 80%, and the protocol wants to reduce the LTV of this token to 75%. Then all users who use $TOKEN2 to borrow more than 75% can no longer leverage $TOKEN2 to borrower more assets (that is, the current LTV of $TOKEN2 is 0). Only when the user returns part of $TOKEN2 to make the LTV greater than 0, can users continue to make a loan backed by $TOKEN2.

Price Oracle Sentinel(for L2)

Supporting more L2 network is also a goal of V3. To solve the problem of untimely update of Layer 2 prices caused by Layer 1 congestion in extreme cases, Aave proposed Price Oracle Sentinel. It means that when the L2 price update/transaction record is delayed, the user's liquidated position will have a grace period before the next block is produced. That is to say, the user's position will not be liquidated before the oracle price is updated, but the user will not be able to borrow any more during this period.

Market Overview

As of March 18, 2022 (06:56 UTC), the operating data of Aave V3 in each market is illustrated in the table bellow. At present, Aave V3 has not yet been deployed on Ethereum. And the using experience is relatively smooth and fast. However, according to the statistics, Ethereum is still the largest in-demand lending market, and part of V3's functions have not been fully deployed yet. Therefore Aave may not see an extreme growth in the short term, but V3 is a must step for Aave's long-term development.

Token Information: Aave (AAVE)

Aave

Lending

DeFi

In This Article

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open