Angle - A Bold Attempt for EURO Stablecoin

Angle is an EURO stablecoin issuance platform on Ethereum. This article will briefly introduce the mechanism and token information of Angle.

Angle is an EURO stablecoin issuance platform on Ethereum. This article will briefly introduce the mechanism and token information of Angle.

Key Takeaways

- Angle is a EURO stablecoin issuance platform, where users do not deposit collaterals to exchange stablecoins, but directly mint them (or buy them) based on the oracle price. Angle smart contract is working as the counterparty to users;

- Angle supports perpetual swap for minted stables. Angle also has an “insurance fund”, which users can earn yield by providing liquidity. It also works as a buffer for the moments when traders do not fully cover the collateral that was brought.

- Angle's investors are a16z, Wintermute, Divergence, and others.

- You can earn $ANGLE token from minting stablecoins, opening positions, staking, providing liquidity.

What is the Angle Protocol?

Angle is a stablecoin issuance and derivative trading protocol that allows users to use collateral to mint different types of stablecoins. It also supports traders to trade stablecoins minted in a way of perpetual swap.

The Angle protocol provides three application scenarios and corresponding types of users:

- Minting and burning: Users who just need stablecoins somewhere else;

- Perpetual swap trading: risk hedging or traders can trade stablecoins directly; Angle provides the perpetual swap feature on its platform;

- Arbitrage or liquidity provision: Balance the difference between oracle price and AMM price; provide liquidity for the insurance fund and earn the transaction fees and yield farming profit of the insurance fund.

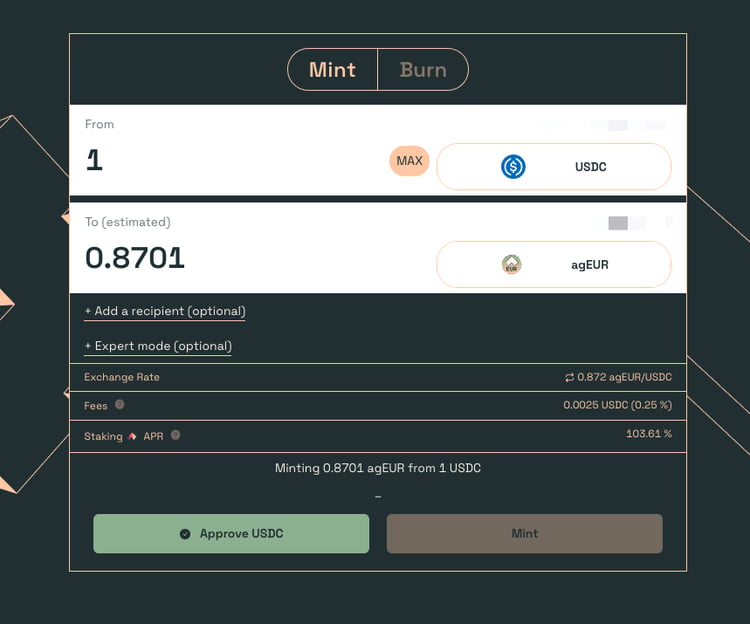

Minting and Burning

Minting and burning are always based on the oracle prices from Uniswap or Chainlink. There will be no slippage no matter how many stablecoins are minted or burned. Users are actually trading against Angle's smart contracts.

In contrast to Maker, the user deposit ETH in Maker's contract in exchange for DAI. Although the ETH collateral provided by the user is kept in the Maker contract, it still belongs to the user and is only a position opened by the user. Users can take the exchanged DAI and redeem the original amount of ETH.

But in Angle, after the user has minted the stablecoin with collaterals, the collateral then belongs to the contract. You can get collaterals back by burning stablecoins, but the quantity will probably change. These two processes are buying and selling. However, when the oracle price of the stablecoin changes, the amount of collateral exchanged by users will also change.

For example, you sold 1000 USDC to the contract for stablecoin with the oracle price at 1 USDC = 1 STABLE, and minted 1000 units of STABLE (transaction fees are not counted here).

- After some time, the price of STABLE fell. Now it is 1 USDC = 2 STABLE. If you try to burn the stablecoin, you will sell 1000 STABLE to the contract and get only 500 USDC back.

- If the STABLE oracle price increases, and becomes 2 USDC = 1 STABLE. Then selling 1000 STABLE to burn to get you 2000 USDC collateral back.

- However, if there is not enough USDC in the contract, for example, there is only 500 USDC left in the contract, then the transaction of burning will fail. The contract does not care about price changes, but only executes the transaction according to the price of the oracle.

In less extreme cases, market arbitrage can keep the price balance between oracle and AMM markets by minting or burning. When the price of the oracle is higher, buy stables and burn them to exchange back more collateral; when the market price is higher, mint stable coins and sell them in the AMM market.

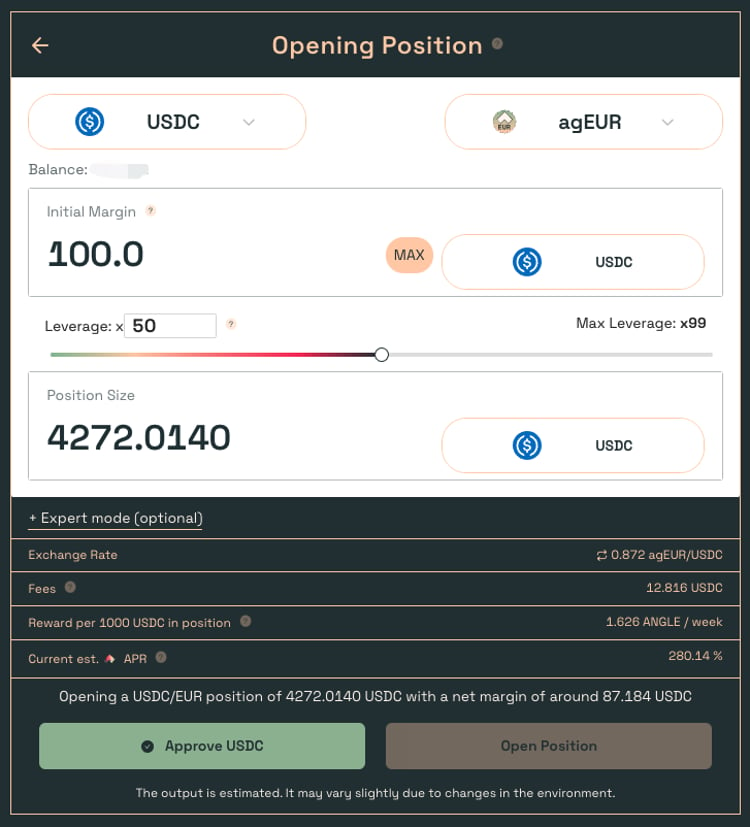

Perpetual swap

The perpetual swap provided by Angle is relatively simple. You only need to select the supported collateral and the stablecoins that you want to open, and the leverage. In the above picture, 100 USDC is selected as collateral to open the agEUR (EURO stable currency minted in Angle) position, and 50x leverage is selected. The nominal value of the position is 4272 USDC, and the difference of 72.8 U from 500 USDC is the transaction fee.

In Angle, the higher the leverage ratio, the higher the fee ratio.

Liquidity Provision

Due to the existence of perpetual swap in Angle, the provision of liquidity actually constitutes an insurance fund. The insurance fund in Angle is similar to the insurance fund in the centralized exchange working as a buffer.

When the insurance fund is idle, it will be allocated to other protocols to earn interest (Yearn, Compound, etc.). Users who provide liquidity can receive the yield earned from reusing idle funds. In addition, part of the transaction fee paid by users in minting and burning will also be distributed to liquidity providers.

EURO Stablecoin

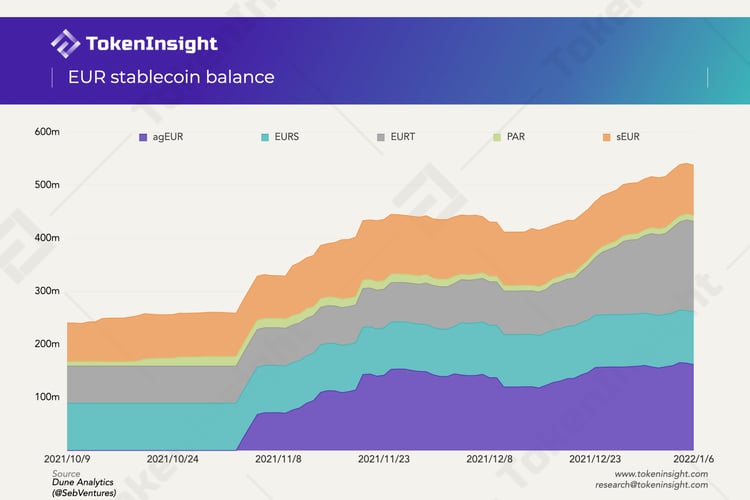

Although the demand for euro stablecoins is still low in Crypto market, the balance of on-chain euro stablecoins has grown from 250 million to over 500 million in the past 3 months, an increase of over 100%. Angle, which went live in November, already has a foothold in the euro stablecoin market, with agEUR's currently accounting for about 30% of the market share.

Token Economy

- Token: ANGLE

- Total Supply: 10,000,000,000

- Access: Minting stablecoins, staking, opening positions, providing liquidity, etc.

- Usage: Token economy of ANGLE was updated in early January, following the incentive mechanism of Curve Finance's veCRV. Users need to pledge ANGLE to get veANGLE. veANGLE cannot be traded, and the more ANGLE pledged and the longer the time, the more veANGLE can be obtained. veANGLE holders can get up to 2.5x liquidity mining rewards, and decentralized governance will use veANGLE to calculate weights.

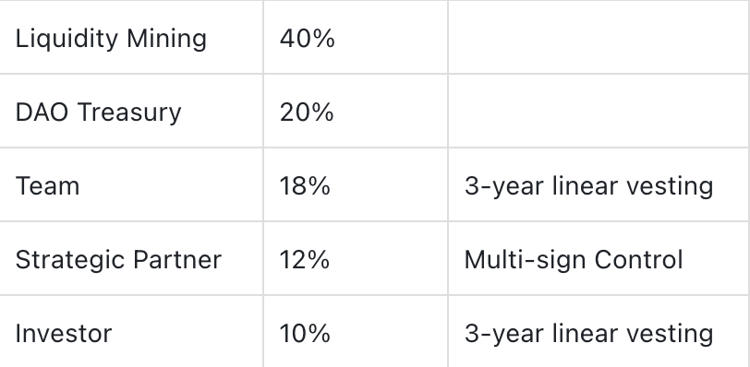

- Token Distribution & Vesting Plan

![]()

- Investors: a16z, FABRIC Ventures, Wintermute, Divergence, GFC, Alven, Julien Bouteloup, Frederic Montagon

Token Information: Angle Protocol(ANGLE)

Stablecoins

DeFi

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open