Bancor v3 - What Can We Expect from OG DeFi?

It is a dark time for DeFi, or even for the entire crypto market. It is probably a good time to look back at some battle-tested DeFi that has withstood cycles already. Today I want to have a review of Bancor, which has just released its v3 update on May 11th. Being the first AMM DEX, what is its current state, and what are the new features for v3.

It is a dark time for DeFi, or even for the entire crypto market. It is probably a good time to look back at some battle-tested DeFi that has withstood cycles already. Today I want to have a review of Bancor, which has just released its v3 update on May 11th. Being the first AMM DEX, what is its current state, and what are the new features for v3.

Bancor - the First AMM DEX

The history of Bancor can be traced back to 2016, so there is a saying before there was DeFi, there was Bancor.

Bancor just released its v3 on 11 May (good timing…), I will explain version 2 first, and then introduce new features for version 3. Lastly, I will compare several major DEXes by some common valuation metrics.

Two Main Features of Bancor v2

Single-sided liquidity providing

For most AMMs, liquidity providers need to provide both a base asset and a quote asset. For example, a typical liquidity pair $ETH (base asset) and $USDC (quote asset). This is not optimal for a holder who just wants to hold $ETH, as he needs to convert part of his $ETH holding into $USDC, resulting in a lesser exposure to the $ETH.

Bancor v2 introduced the single-sided staking enabling LPs to provide single-sided liquidity. This is achieved through the protocol token $BNT. When someone deposits $100 token A, the protocol will mint an equal amount of $100 $BNT to fill the other half of the pool. When someone withdraws the $100 token A liquidity, the corresponding amount of $BNT will be pulled out of the pool and burned.

All of the liquidity for Token A is concentrated in one pool. When swap Token A to Token B, the transaction is routed through $BNT, the swap takes two-step, Token A to $BNT, and $BNT to Token B.

Impermanent Loss Protection

One of the biggest risks LP faces is impermanent loss. Bancor is the first protocol that provides full impermanent loss insurance.

A liquidity pool can consistently accrue fees for LPs through trading activity. As mentioned previously, half of the liquidity pool is provided by Bancor protocol through its token $BNT. Once a user withdraws their liquidity position, the fees earned by the protocol are then used to pay back LPs for impermanent loss. If the impermanent loss of a pool is greater than the fees that it is generated, the protocol then mints $BNT to pay back the insufficient amount.

Tokenomic

$BNT has an elastic supply. When LPs deposit token A liquidity, the protocol mint $BNT to match the dollar amount of Token A. The newly minted $BNT is removed when the liquidity is withdrawn. You may worry this will incur consistent inflationary pressure for $BNT, but in essence, this part of $BNT never goes to the open market circulation.

The protocol generates revenue by providing half of the liquidity, and the revenue is used for impermanent loss protection. If there is remaining value after paying the impermanent loss, the excessive amount of $BNT is burned.

$BNT token could have consistently inflationary pressure if the impermanent loss exceeds the fee generated. To limit the risk exposure, Bancor v2 set a deposit limit for every token listed, so LPs can only deposit amounts within a specific amount. In addition, LPs do not have 100% impermanent loss protection from the time they provide liquidity. The percentage of protection is linearly increased with time. To enjoy 100% protection, LPs need to remain in the pool for 100 days.

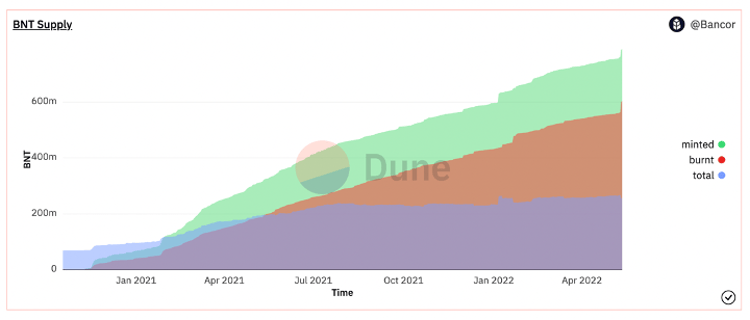

Source: https://dune.com/Bancor/bancor_1

The mechanism of Bancor has run pretty effectively. The amount burned of $BNT has been roughly kept the pace of the amount minted, resulting in a roughly constant $BNT total supply.

Bancor v3

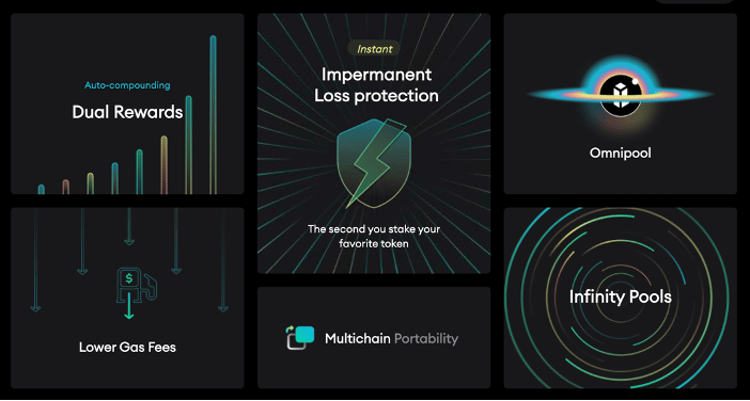

Source: https://try.bancor.network/

Bancor v2 provided a successful solution for single-sided staking and impermanent loss protection. However, its limitation is also substantial.

Notably, the protocol places a cap on each pool which limit the growth of the protocol. And users could only get full impermanent loss protection after 100 days. In addition, all transactions are routed by $BNT, this adds to the complexity of swap and incurs a larger transaction gas cost for swapping between tokens. All these limitations lead to a slow adaptation of the protocol.

Instant Impermanent Loss Protection

After one year of operation of v2, Bancor found the 100 days criteria is far too conservative. It modified the model, rather than delay the full impermanent loss protection, the

measure is changed to a 7-day cooling period when withdrawing liquidity from the pool and a 0.25% LP exit fee. When LPs want to remove their liquidity, they have to wait 7 days, and the fees earned in this period will be distributed to the rest of the LPs.

Infinity Pools

The cap on deposits is removed. LPs can now deposit any amount of single token into Bancor's pool.

Omnipool

The current liquidity pool on Bancor is a standalone pool, which is the standard across all AMM. However, the difference in Bancor is it use $BNT as a router for transaction between two different tokens. This leads to higher gas costs. In v3, the omnipool holds all tokens, each token paired with a single $BNT virtual pool. The swap can be executed in a single transaction, thus greatly reducing the gas cost.

Closing Thoughts

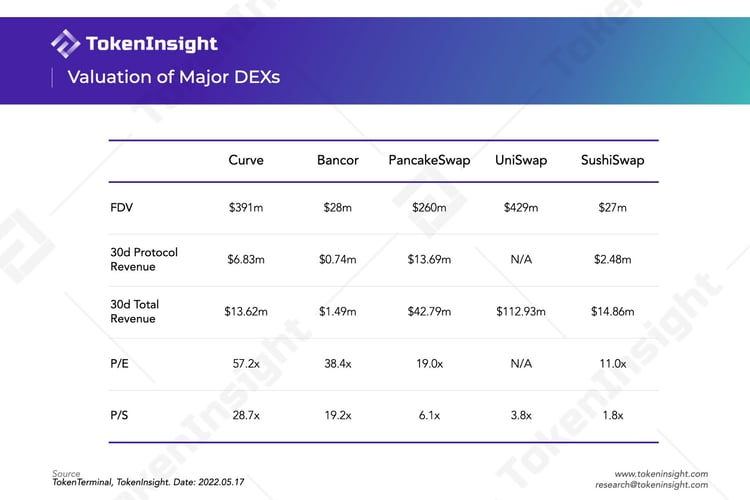

DEXs and lending protocol are the only two DeFi products that have established a profitable business model. This means we can use some traditional valuation metrics to look at the valuation.

Here I use the P/S, and P/E ratios. P/S ratio is calculated by FDV / annualized revenue, and P/E is calculated by FDV / annualized protocol revenue. The data here is as of May 17, 2022, so this reveals some insights after the massive sell-off that happened recently.

Curve is still the DEX with the highest valuation, this probably dues to $CRV's important governance value in the Curve war. Considering Curve's focus on the stabelcoin transaction market and the possible cooling down of the Curve war, I am not sure whether this high valuation could sustain due to a general fall in the appetite of algo-stablecoin.

I was surprised to see Bancor's valuation is still on the high side if compared to other DEXs in this bearish sentiment environment. And I cannot come up with any good explanations for that.

For Bancor, the main problems that deter its development in v2 have all been tackled in v3. This includes the deposit cap, high gas cost due to the transaction routing, as well as the 100 days requirement for impermanent loss protection. These improvement of version 3 could lead to an increase in TVL and transaction volume if the general market sentiment recovers.

AMM

DEX

DeFi

In This Article

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open