Could GMX Collapse in a Bull Market? A Deep Dive.

"Although GMX is killing it in the current bear market, it could implode in a bull." A friend casually fudded my bag during a coffee chat. "The GMX design will cause an imbalance between long/short positions in a bull market, reduce GLP returns, and trigger a death spiral."

"Although GMX is killing it in the current bear market, it could implode in a bull." A friend casually fudded my bag during a coffee chat. "The GMX design will cause an imbalance between long/short positions in a bull market, reduce GLP returns, and trigger a death spiral."

I was amused. GMX was one of the best-performing DeFi protocols in 2022. A bull market could only boost its usage and pump $GMX higher.

But after pondering the idea repeatedly, I realized it was not complete bullshit. So I checked whether what my friend described was indeed probable.

Here's what I found:

- Very few traders will open short positions on GMX in a bull market.

- A long-only GMX will reduce GLP returns, but it is unclear whether this will cause liquidity providers to withdraw.

- GMX's design shortcoming is less apparent in a bear market, but the so-called GMX bull market death spiral is not valid.

I share my analysis in detail below, and I appreciate any feedback, or criticism. I don't care if I am right or wrong. I only care whether I should hold my $GMX when the next bull market arrives.

What Is GMX

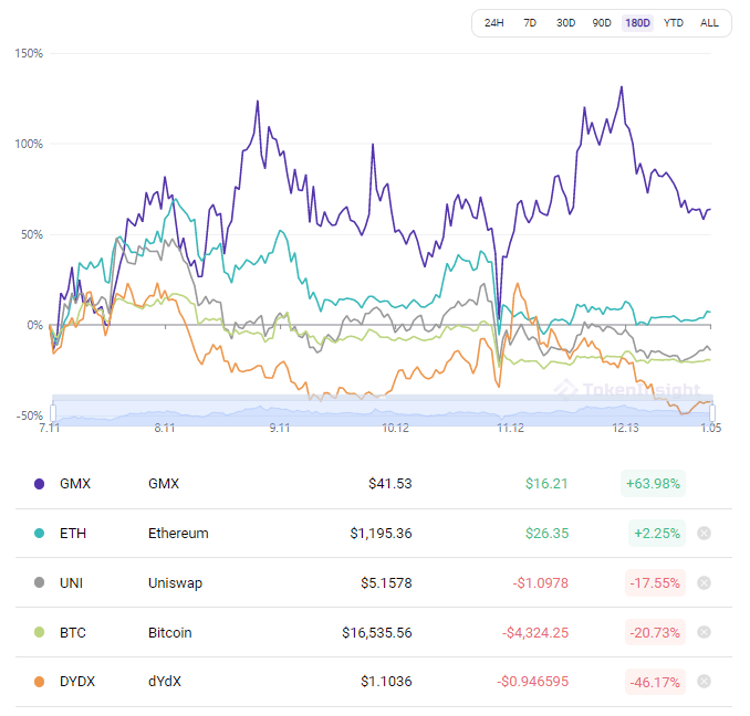

It's a bear market for crypto but not for GMX. In the past half year, $GMX significantly outperformed the market, while DeFi blue-chips like $DYDX took a freefall.

GMX offers spot swap and margin trading with zero slippage. GMX achieves this feat by letting users trade against the GLP pool, unlike traditional perps exchanges where users trade against one another. GMX doesn’t technically offer perps, but the margin trading experience resembles that of a perps exchange.

GLP is a basket of assets, about 50% of which are stablecoins, and the other half are cryptocurrencies like $BTC (15%) and $ETH (35%). GLP is the counterparty of every trade placed on GMX. LPs provide liquidity to GMX by depositing assets into the GLP pool. In return, GLP holders earn 70% of fees generated by GMX. GLP holders also win extra if traders lose their bets and vice versa.

The Real Yield Narrative

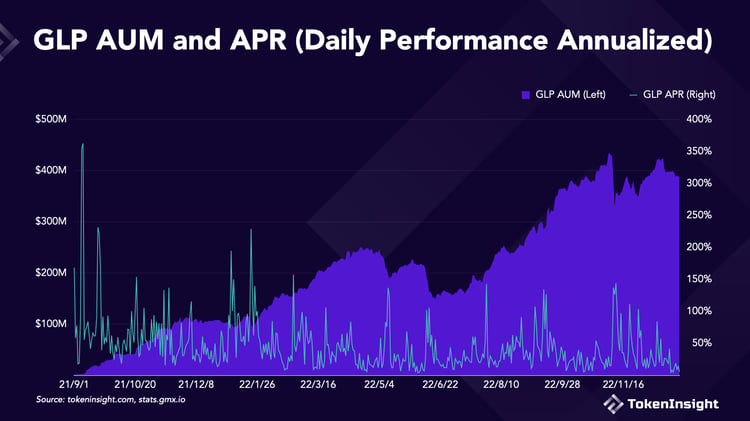

GMX quickly rose to prominence because the real yield narrative stormed crypto Twitter. Degens rotated from highly-inflationary tokens to real yield farms like GLP. GMX's $GLP consistently returned 20%+ APR in $ETH throughout most parts of 2022, even dwarfing Anchor during Terra's most glorious days. GLP AUM continued to increase despite macro and crypto headwinds while maintaining a competitive APR.

Note that here APR = Daily Fees / GLP AUM * 365 Days.

GLP's Challenge

GLP's biggest challenge is to stay competitive in a bull market, because its design shortcoming is less apparent in a bear market.

Every design is a balance of trade-offs. While GMX allows traders to execute zero-slippage trades in a fully decentralized manner, GMX requires traders to pay borrowing fees to GLP regardless of whether they are long or short. This is different from trading on a traditional perps exchange.

On a traditional perps exchange, traders pay a funding fee to those holding the opposite position, depending on the difference between perp price and spot price. For example, when the market is bullish, and the funding rate is positive (perp price > spot price), traders with long positions pay traders with short positions. There is always one side that receives funding fee payments to keep their positions open.

Again, GMX is not perps. It is perps-like trading. Delphi Digital briefly touched upon this point in their analysis but didn't dive deeper.

Traders are split between long and short in a bear market, and the difference between a traditional perps exchange and GMX is small.

But traders are mega-long in a bull market. Traditional perps exchanges balance this skew by rewarding short positions with funding fees. However, GMX traders not only do not receive funding fee payments but also have to pay borrowing fees. As a result, holding short positions on GMX during a bull run does not make sense.

So GMX will be full of longs in a bull market.

First, this makes the GLP pool less capital-efficient because the stablecoin half of the pool will be useless. Traders will only borrow $BTC and $ETH from the pool to make long bets. This is like flying a plane with just one side of the engine. You will not fall from the sky immediately, but you will be less safe.

Second, GLP will consistently lose money to traders because they rent out the upside of their $BTC and $ETH. GLP has to rely on fees to compensate for the losses. The decrease in returns could cause liquidity providers to seek better farms elsewhere. A bull market means they can easily find Ponzi coins that will deliver 1,000,000% APR before the party ends. Do you still remember $TIME?

Decreasing GLP leads to fewer assets that traders can borrow. If there is not enough liquidity, traders will seek liquidity elsewhere. Fewer traders generate fewer fees, which cuts GLP returns further and triggers the death spiral.

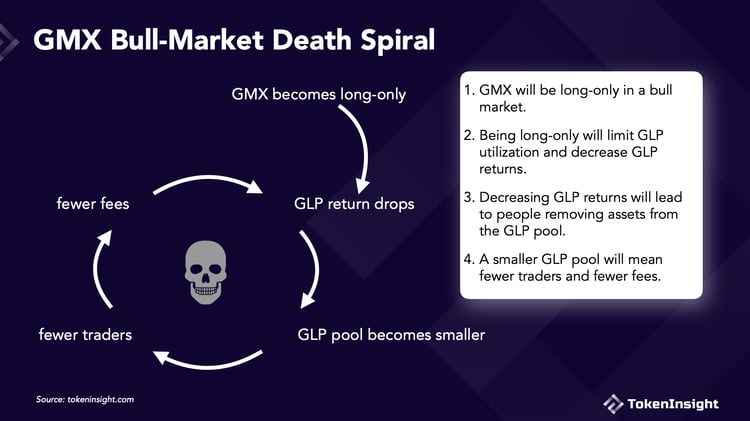

What Does GMX's Death Spiral Look Like?

The GMX bull-market death spiral consists of four steps:

- GMX will be long-only in a bull market.

- Being long-only will limit GLP utilization and decrease GLP returns.

- Decreasing GLP returns will lead to people removing assets from the GLP pool.

- A smaller GLP pool will mean fewer traders and fewer fees.

I use data to verify each step in the following sections.

GMX Will Be Long-Only in a Bull Market

This is 95% true.

Because short positions can receive funding fees elsewhere but have to pay borrowing fees on GMX, a rational trader will not open short positions on GMX during a bull run.

Data supports this claim.

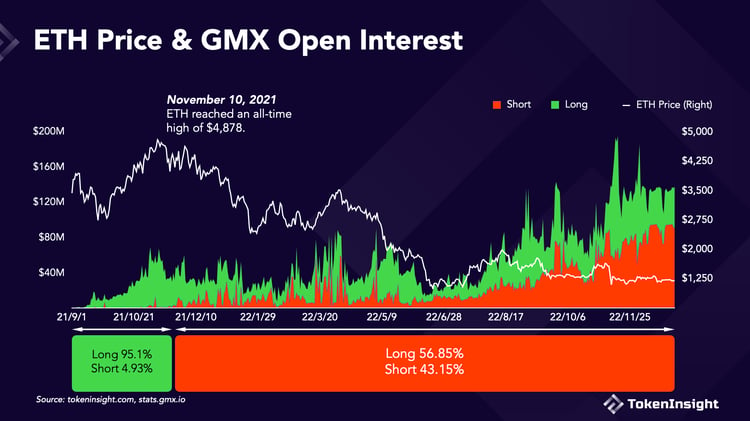

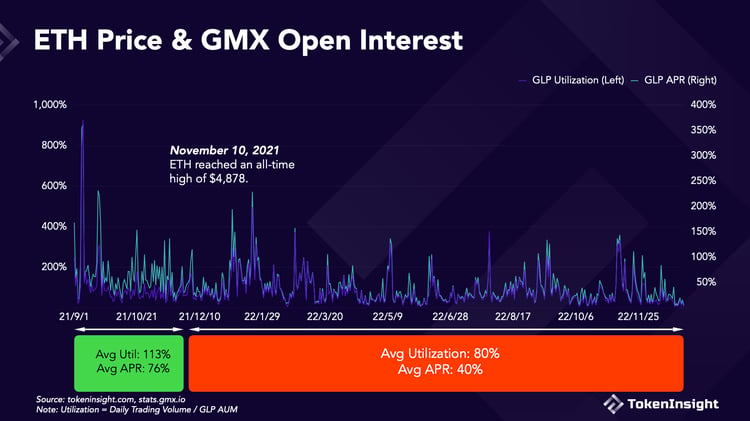

GMX's 15-month history can be divided into two parts. From September 1, 2021 to November 10, 2021 is a short bull market, where $ETH rallied to its all-time high. From November 10, 2021 onwards is an extended period of pain, where $ETH dropped by over 70%.

While traders were split almost 50-50 during the second part, 95% of the open interest on GMX was long during the first part. History will repeat itself when the next bull market arrives.

Being Long-Only Will Limit GLP Utilization and Decrease GLP Returns

This is unclear, but probably false.

Just looking at utilization and GLP APR does not help at all. Data shows that GLP performed better during the long-only phase. But it is an unfair comparison. GLP was small during the early days, so the returns were naturally higher.

However, whether traders make or lose money is closely related to the price movements of $ETH.

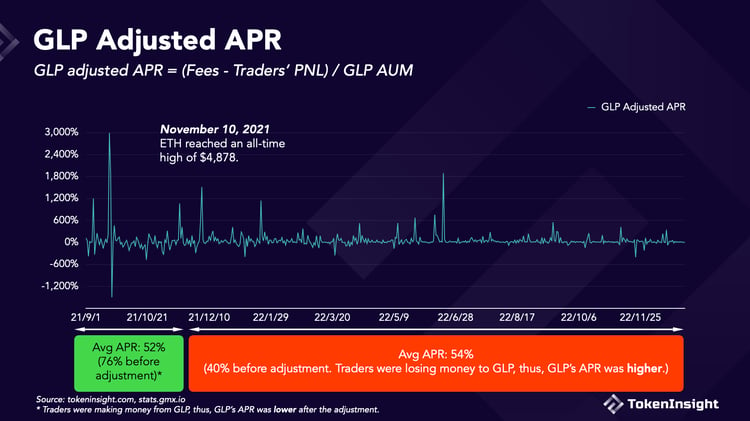

Gamblers always lose to the house. This holds for most of GMX's 15-month history, but not all. When $ETH rallied to an all-time high last fall, traders turned a ~$2 million deficit (Sep 21, 2021) into a $3 million surplus (Nov 10, 2021), netting a profit of ~$5 million. However, as $ETH plunged from $4,878 to ~$1,200, GMX traders managed to squander all the winnings and accumulate a net loss of over $40 million.

Although the sample is small, we have to admit that GLP will consistently lose money to traders during bull markets. In that event, do fees more than compensate for the losses?

I calculated GLP adjusted returns by subtracting (or adding) trader PnL to fees.

GLP's adjusted APR was lower during the bull market phase and higher during the bear market phase, because GLP returns were reduced by traders' winnings during the bull and boosted by traders' losses during the bear. Traders submit fees as well as their margins in a bear market.

GLP adjusted APR averaged ~50%, which was not bad at all. But this is where things get messy, because the first bullish phase coincided with the early days of GMX, when everything was experimental, data points were limited, and thus the result could be biased.

Decreasing GLP Returns Will Lead to People Removing Assets From the GLP Pool

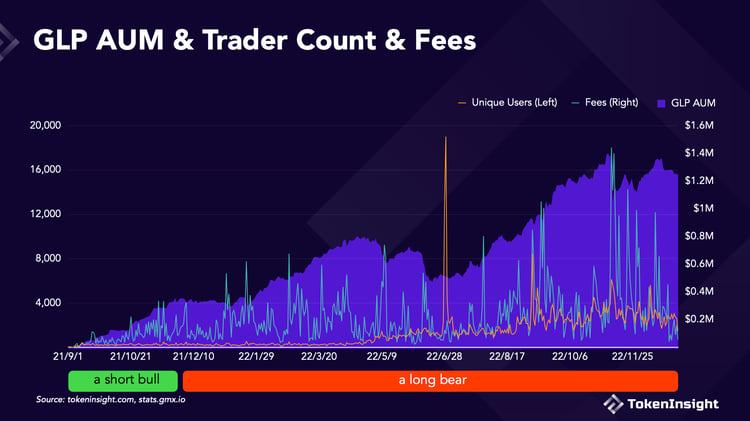

So do LPs flee when GLP returns decrease? Not really.

During Part I, when Adjusted APR was often negative, AUM grew nonetheless.

If anything, a decrease in GLP leads to an increase in APR. When there are fewer GLP holders at the table, everybody that remains gets a bigger slice of the cake. This dynamic prevents a bank run and helps stabilize GLP supply.

A Smaller GLP Pool Will Mean Fewer Traders and Fewer Fees

It is also unclear whether a smaller GLP pool means fewer traders and fewer fees. Too many factors are in play, and the causal effect is not evident.

The sharp decreases in GLP supply were all triggered by historical crypto events rather than fluctuations in APR, such as Terra in May, 3AC in June, and FTX in November, when the markets were volatile, and traders were the most active. As a result, a decrease in GLP AUM was usually accompanied by an increase in fees. The dynamic mentioned in the previous section was amplified: remaining GLP holders were already set to receive a larger slice, and the cake got bigger. Market-wide crypto FUD → more GLP redeem & more traders & high fees → high GLP APR → more GLP mint.

The risk of liquidity drying up always exists. As I was writing this article, the available liquidity to long ETH on GMX dropped to less than $40k, because there was a mini-bull run, and every trader rushed to profit from it. There will be more moments like this, especially during an extended bull run. It's hard to predict what will happen then, but GMX is unlikely to implode based on past performance.

Closing Thoughts

The so-called GMX bull market death spiral is not valid. GMX/GLP is an attractive money printer even if all traders are long in a bull market. GMX generates more than enough fees for GLP holders to cover their losses to traders.

However, the long/short imbalance is real. GMX may implement measures to mitigate the effect. For example, GMX can increase the borrowing fee of long positions and include a dynamic fee payment to shorts, to incentivize traders to open short positions. GMX can also decrease the swap fees to incentivize users to swap $BTC/$ETH for stablecoins in the GLP pool.

The decrease in GLP returns during a bull market also has broad implications for projects that rely on its yield, such as Umami, Jones DAO, Rage Trade, GMD, etc.

Narratives on CT affect sentiment and price. GMX benefitted from the real yield narrative and could be hurt by other narratives.

The following scenario is not impossible: liquidity tightens in a bull run, traders cannot open new positions, GLP holders cannot withdraw, and FUD intensifies on Twitter so that people start to trust threads instead of facts.

Black swans did not exist until adventurers discovered them in Western Australia.

DeFi

Derivatives

DEX

In This Article

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open