Curve Finance - DEX Designed for Stablecoins

Curve Finance is a decentralized exchange designed for stablecoins. This article will briefly introduce the mechanism and token information of Curve Finance.

Curve Finance is a decentralized exchange designed for stablecoins. This article will briefly introduce the mechanism and token information of Curve Finance.

- The Curve's AMM model is more suitable for stablecoins with low slippage and low fees (0.04%).

- Higher APY, users can earn extra yield except for transaction fees.

- Nearly half of the supplied CRVs are locked.

Curve Finance is a decentralized exchange (DEX) for stablecoins that has been deployed on multi-chains, such as Ethereum, Arbitrum, Avalanche, Fantom, Harmony, Polygon, and xDAI. As of December 29th, 2021, the TVL of Curve reaches $22.97b, the 24h trading volume on it is $254.34m, and its market cap is $2.10b.

AMM for stablecoins

Just like Uniswap, users can be an LP (liquidity provider) or a trader on the protocol. However, Curve is specially designed to provide exchanges services for stablecoins (USDT, USDC, DAI) or tokens with similar values, such as stETH & wETH, renBTC & wBTC, etc.

On Uniswap, the price of a token is determined by the ratio of the two underlying tokens in the pool, thus, the token's price will constantly change while users interact with the pool. In addition, when there is a lack of liquidity in the pool or an imbalance in the ratio of the two tokens, a small-sized transaction can impact the token's price massively, namely high slippage. To solve this, Curve has improved on the traditional AMM algorithm to make it more consistent with the characteristics of stablecoins. Because the price of stablecoins usually fluctuates in a certain price range, for example, the price of USD-anchored coins always fluctuates around $1.

In Uniswap, if there are 10 ETH and 10,000 USDT in the liquidity pool, at the moment 1 ETH worths 1,000 USDT. If the user exchanges 1 ETH with 1,000 USDT, there will be 11 ETH and 9,000 USDT left in the pool, which means that 1 ETH is worth 818.18 USDT.

When trading pair balance gets out of balance, for example, there is only 1 ETH and 10,000 USDT. If the user exchanges 0.5 ETH, the price of ETH will change from 10,000 to 30,000 USDT, which is extremely huge.

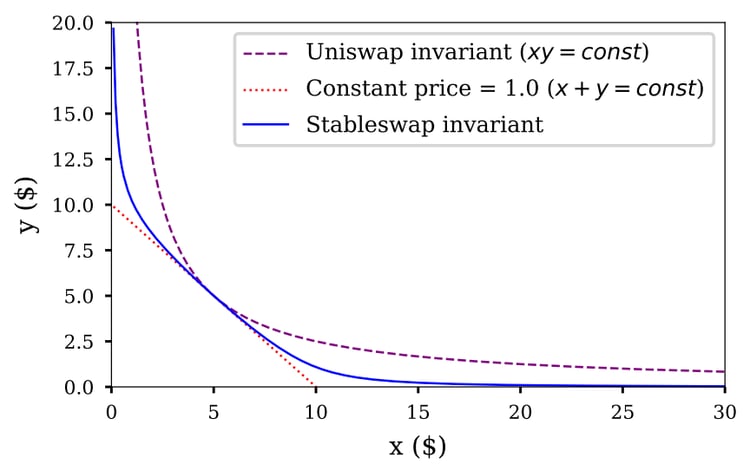

The figure below shows the Bonding Curve of Curve Finance and Uniswap. Compared with Uniswap, although the line of Curve Finance has larger slippage at both ends, the slippage in the middle part is quite low, and it even overlaps with the line with a slope of 1. This is exactly in line with the characteristics of stablecoins, because the prices of stablecoins usually fluctuate in a small range around $1.

Source: Curve Finance

Therefore, trading stablecoins on Curve is helpful for users to reduce their slippage losses. By the way, the transaction fee on Curve (0.04%) is also less than that of Uniswap (0.3%).

50% of Curve transaction fee will be awarded to LP, and the rest will be awarded to CRV stakers.

Bonus

Notably, there might be more than two assets in Curves's liquidity pools, for example, the Curve is made of DAI, USDC, and USDT.

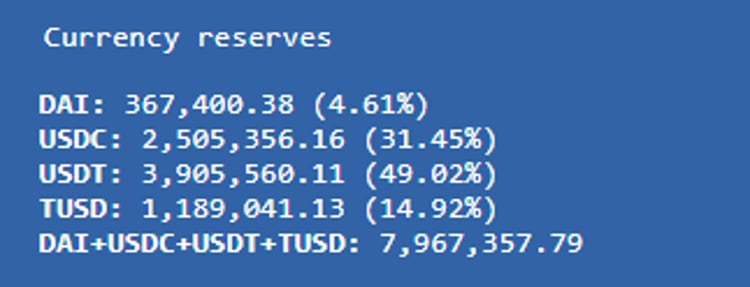

In theory, there should be a one-to-one exchange relationship between USD stablecoins, otherwise, there is room for arbitrage, so the proportion of tokens in the pool should be the same. For example, in the figure below, the percentage of all four stablecoins (DAI, USDC, USDT, TUSD) should be 25%, however, it is not at this point. So in order to motivate users to work together to maintain stablecoin's price, Curve adopts the deposit bonus and withdrawal bonus.

Source: Curve Finance

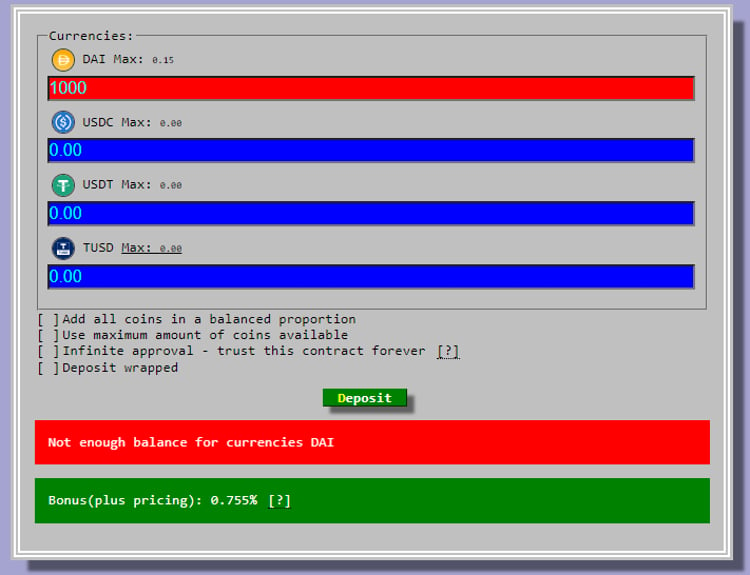

If users add liquidity with DAI, the least asset in the pool, they can receive a 0.755% bonus. Similarly, if users withdraw USDT, they will be rewarded some withdrawal bonus as well.

Users can add liquidity by one or more kinds of tokens, and there is no need to put them in proportion. The protocol will automatically swap it into an appropriate proportion, and then add them to the pool.

Source: Curve Finance

In addition to the basic stablecoin pool, there are also some special pools on Curve which enable users to earn extra profit from another protocol. For example, the tokens in the Compound pool will be deposited into Compound (a lending protocol) to earn interest.

CRV Token

There are three main functions of CRV, namely Staking, Voting, and Boosting.

- Staking

Users stake CRV will get veVRC as a representation, and receive 50% of transaction fees.

- Voting & Boosting

Users can further lock veCRV to participate in DAO governance, and the voting power is related to users' locking amount and locking period. If the user is a CRV staker and a liquidity provider at the same time, he/she can earn a boost of up to 2.5x on the liquidity.

The total issuance of CRV is 3.03 billion, of which 62% will be allocated to LP through liquidity mining. The specific token distribution and unlocking plan are as follows:

Source: Curve Finance

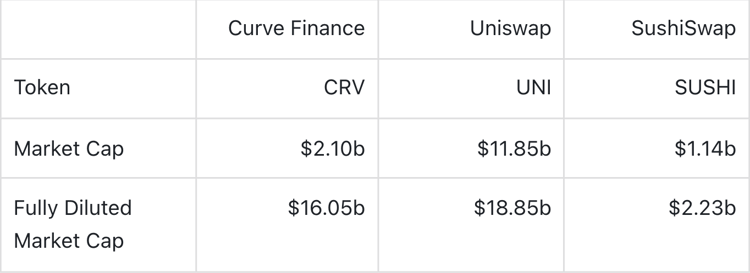

As of December 29th, 2021, Curve's TVL is $22.97b. The price of CRV is $4.86, the market value is about $2.10b, the fully diluted market value is $16.05b, and the max supply is 3.30b. (Data source: Curve Finance, TokenInsight)

Currently, the daily CRV distribution to LPs is approximately 753,262.53 CRVs. And where these tokens are allocated mainly depends on two factors, one is Liquidity gauge and the other is Weight gauge.

Liquidity gauge refers to the proportion of the token provided by each user in the liquidity pool. Weight gauge is the distribution of CRV rewards for each pool determined by Curve DAO voting. Such a mechanism determines that users can maximize their benefits only by locking CRV (more bonus bonuses and greater governance power).

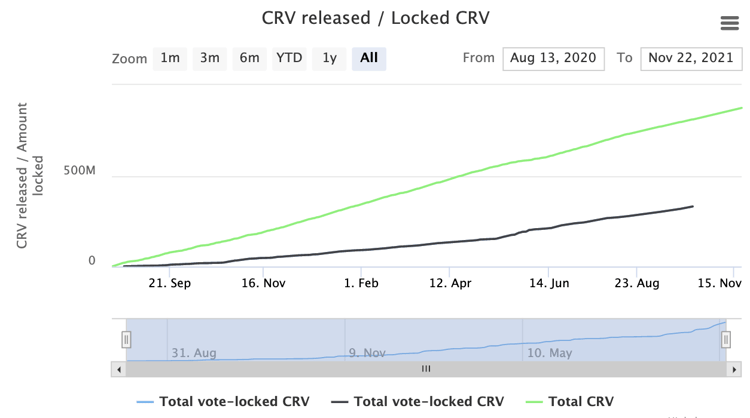

There are currently some DeFi protocols, such as Yearn and Convex, and their yield strategy is based on Curve's liquidity reward mechanism. In other words, they will put the tokens deposited by users on Curve for liquidity mining rewards. And through Curve governance, voting for their liquidity pool and getting more CRV rewards has also become the common goal of these protocols. This has also led to the continuous increase of CRV's stake rate. Up to now, the lock-up rate of CRV is about 50.18%, and the average lock-up time is 3.63 years.

Source: Curve Finance

TI Information: Curve Finance

Curve

DEX

Stablecoins

DeFi

In This Article

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open