Crypto Decentralized Derivatives Exchange 2022 Q3 Report

In this report we hope to sort out and clarify the situation of decentralized exchanges derivatives market, especially the perpetual contracts products that are most popular among Defi users. The report will try to clarify the current state of decentralized perpetual contract trading from several protocols, including dYdX, GMX, Perpetual Protocol, Kwenta, etc paired with our research and findings to the broader Defi users and institutions.

In this report we hope to sort out and clarify the situation of decentralized exchanges derivatives market, especially the perpetual contracts products that are most popular among Defi users. The report will try to clarify the current state of decentralized perpetual contract trading from several protocols, including dYdX, GMX, Perpetual Protocol, Kwenta, etc paired with our research and findings to the broader Defi users and institutions.

TL,DR

- Crypto derivatives trading first started in 2011, but a new chapter was officially started after BitMEX invented the perpetual contract. The market was booming in 2019 and reached the peak of trading volume in 2021 as the bull market came.

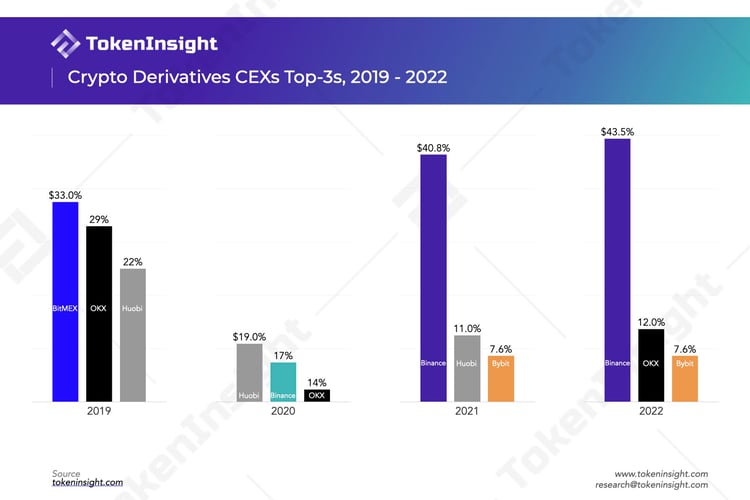

- The top three derivatives exchanges in 2019 are BitMEX, OKX, and Huobi; in 2020 they are Huobi, Binance and OKX; in 2021 they are Binance, Huobi and Bybit; in 2022 they are Binance, OKX, and Bybit (there was originally a place for FTX).

- Decentralized derivatives exchanges have obvious advantages over traditional centralized derivatives exchanges in terms of asset transparency, user asset control, censorship resistance and privacy, and on-chain composability.

- Insufficient liquidity, high transaction costs, low product usability, and poor function richness are the main problems faced by decentralized exchanges.

- Over the past 10-month period, the total trading volume of decentralized derivatives exchanges reached $478B. While this figure is roughly equivalent to two weeks of Binance derivatives trading volume in the current market environment, this figure was almost zero at the beginning of last year.

- dYdX is the leading decentralized exchange before Q3 in 2022, but there are signs of being surpassed by GMX in terms of trading volume after Q3; dYdX has sometimes been surpassed by GMX in terms of platform revenue, and GMX has already ranked first in terms of TVL.

- According to the current market development trend, the market size of decentralized exchanges is expected to increase by more than 10 times within a year.

- From the perspective of decentralization, dYdX is the lowest compared to GMX, Perpetual and Drift. At the same time, the vAMM mechanisms of Perpetual and Drift are less adaptable to the current market than the other two protocols.

- From the perspective of fee structure, compared with the others, GMX and Perpetual's sources of fees are more abundant, which helps the protocol to develop better; and the fee structures are also better, which is conducive to user incentives. In contrast, dYdX keeps all platform revenue for itself.

- dYdX, GMX, and Perpetual all have sound tokenomics, encouraging users to participate in protocol governance and token staking. However, in terms of effect, dYdX and Perpetual will be slightly inferior to GMX, mainly because the actual income received by users after participation is lower.

- The next development direction of the decentralized derivatives exchanges mainly includes providing more trading mechanisms and products, striving for market share, launching new chains, and realizing fully decentralization (especially dYdX), etc.

- The core mechanism of most new entrants still applies the mechanism established by the current leading project, namely the order book, multi-asset liquidity pool and vAMM mechanism.

Introduction

FTX applied for bankruptcy due to the misappropriation of user funds, causing about 8 billion user funds to be irreparable. The incident affecting millions of users has drastically impacted the whole crypto industry. Because of this event, the entire Crypto market has gradually escalated concerns about the safety of user funds. Subsequently, more and more users of centralized exchanges have withdrawn their funds. At the same time, in order to enhance user confidence and transparency, some exchanges have published their Proof of Reserve or audit reports, and disclosed the wallet addresses.

Although such measures can alleviate the anxiety of the market to a certain extent, the market is still sending a bad signal. Affected by FTX, other centralized exchanges have also experienced a so-called liquidity crisis, and have suspended withdrawals and even insolvency rumors. Such as The vice president of the AAX exchange has announced his resignation, and AAX exchange withdrawals have been suspended from November 13th. Since then, as of the 29th, there has been no resumption of withdrawals. The Japanese exchange Bitfront announced that it will cease operations. Genesis hired restructuring consultants, rumored to be insolvency reorganization. BlockFi also filed for Insolvency reorganization on the 28th.

There is a saying that "a gentleman will never stay under a dangerous wall.". As long as there are other choices. Many users will choose to transfer their assets to a safer place.

As for the demand for the trading itself, when DeFi was not yet developed, users had no choice but to use a centralized exchange. After DeFi Summer, decentralized exchanges developed rapidly and were quickly welcomed by users because they solved the long-tail tokens' liquidity problem. At the same time, the liquidity of some mainstream tokens has been no less than that of centralized exchanges. Therefore, decentralized spot exchanges have become the choice of many users, and users no longer need to deposit funds in centralized institutions but hold them in their wallets to complete transactions.

The liquidity of spot trading is slightly easier to solve than that of derivatives, and AMM (Automated Market Maker) is not performing very well in derivatives trading. The vAMM that had been tried before also failed because the assets in the pool were heavily tilted when the market price trended unilaterally, and the market price could not anchor the index price.

Since the outbreak of Crypto derivatives trading in 2019, the overall market size has continued to expand, and more companies have emerged and focused on this field. The decentralized world has also seen a large number of protocols focusing on derivatives trading since last year. As a product with a strong user need, there is still a big gap between decentralized derivatives trading and centralized products. But perhaps this is where the opportunity lies. Decentralized derivatives trading has not yet appeared as a product similar to Uniswap, and more and more protocols are constantly joining.

In this report, we hope to sort out and clarify the situation of the decentralized exchanges derivatives market, especially the products of the perpetual contract that are most popular among Defi users. The report will try to clarify the current state of decentralized perpetual contract trading from several protocols, including dYdX, GMX, Perpetual Protocol, Kwenta, etc paired with our research and findings to the broader Defi users and institutions.

A Brief Development History of Crypto Derivatives Exchanges

The first Bitcoin derivatives trading platform ICBIT was born in 2011, providing Bitcoin-based Settlement Futures trading. Subsequent exchanges such as Huobi and OKEx also imitated similar products. At that time, the derivatives trading market was still in its infancy and the market size was small.

BitMEX was and still is a key exchange that has truly grown Bitcoin (Crypto) derivatives trading. Founded in 2014, BitMEX initially only offered Bitcoin Futures trading. In 2016, BitMEX invented Perpetual Swaps, which is a type of Futures contract with no expiration date. Both parties pay a funding fee to converge the gap between the Futures price and the spot index price as much as possible.

At the end of 2017, the infamous traditional finance institution CBOE and CME also began to offer derivatives trading of digital currencies, and they were also the first compliant digital currency derivatives exchanges.

After 2019, Crypto derivatives trading began to explode. In that year, the Crypto derivatives trading market was mainly occupied by BitMEX, Huobi DM, and OKEX.

The DeFi Summer, which started in 2020, ignited Ethereum, making $ETH a popular asset besides Bitcoin, and the huge volatility allowed it to amplify the trading volume in the derivatives trading market.

In August 2020, Binance released two contract products, "USDT-Margined" and "Coin-Margined". The "Coin-Margined" refers to the inverse contracts, which means that the collateral and settlement are all in digital currency; while the "USDT-Margined" contract is a product that uses fiat/stablecoin as collateral assets and settlement, more similar to the traditional financial industry.

In April 2021, the dYdX Layer2 was officially released, allowing perpetual contracts to be traded on a decentralized platform. In August of the same year, the dYdX Foundation issued $DYDX as a platform incentive, and the transaction volume subsequently increased.

In September 2021, GMX officially released its product on Arbitrum, which supports customer engagement in spot and perpetual contract transactions of some currencies, and can also participate in market-making by minting $GLP. The Avalanche version of the product was officially released in January 2022.

Founded in May 2019, FTX reached its peak two years later, with more than 1 million users. But in November 2022, due to the misappropriation of user funds and large losses, FTX filed for Chapter 11 bankruptcy proceedings.

Why Does the Crypto Market Need Derivatives?

Risk management

The demand for derivatives in the Crypto market is similar to the demand for derivatives in traditional Financial markets, and the most important reason is risk Hedging. For example, for miners, the amount of Bitcoin they will obtain in the future is basically certain, and the cost of mining is predictable, but the price of Bitcoin is unpredictable. In order to eliminate this uncertainty, miners can use Bitcoin derivatives transactions to lock in the future price while guaranteeing their own returns.

There are also several other similar trading strategies, such as for tokens in high demand in a short period of time, such as participating in the IEO of exchanges, or participating in the voting of public chain nodes, a large number of currencies are required. These coins may experience huge price fluctuations before and after the event. By using derivatives trading, you can eliminate the risks brought by these fluctuations to a certain extent and manage your own risk exposure.

Speculation

Crypto trading is different from the traditional financial industry. Crypto supports 24 * 7 non-stop trading and has greater volatility, which also makes this market a speculator's paradise. The flexibility of derivatives trading itself attracts a large number of speculators to enter and make or lose money.

Add Leverage to amplify income

The leverage ratio of Crypto derivatives trading is generally high. There has been maximum leverage of 500x in the market, and there are many users who use 100x leverage to trade. When the market is volatile, a higher leverage ratio can bring more potential benefits (of course, it will also bring higher risk). And when the market is deserted, it can also artificially create volatility by increasing leverage.

The use of high leverage in the Crypto market is a common situation, which is why the average lifespan of a contract user is not long.

Historical Data Review

We summarize the trading data of Crypto derivatives history. As we said before, the derivatives exchange market officially started after 2019 and peaked during the bull run in 2021.

In terms of quarterly trading volume, the trading volume of Q1 in 2019 was only $264B, Q1 increased by nearly 8 times in 2020, and by 2021, the trading volume reached a staggering $16,590B, which is 62.8 times more than Q1 in 2019.

If you are interested in previous derivatives reports, you can click on the link below to view:

In 2021, the trading volume of Q2 derivatives peaked and began to decline. Q4 of the same year, the trading volume was only about half of Q2. With the end of the Bull Market Q4 last year, the subsequent trading volume continued to shrink. However, due to the collapse of Terra this year, 3AC, FTX insolvency, and other events, although the price continued to fall, the violent fluctuations also made the trading volume decline, but it did not shrink very much.

The historical trend of the total market open interest volume is also roughly the same as the volume trend. Despite the recent market deleveraging, the current level of position squaring volume is still about 7 times that of the same period in 2019.

In terms of market share, we have selected the top three derivatives CEXs markets in the past four years, and their market shares are shown in the chart below.

Before 2020, BitMEX had always occupied the largest market share because the birthplace of the perpetual swap was BitMEX. After 2020, centralized derivatives exchanges flourished, and the degree of market concentration declined compared to before. At that time, Huobi occupied the first position, followed by Binance, OKX (it was called OKEx at that time), these three were also known as the "Big Three" at that time. After 2021, Binance began to surpass other exchanges and firmly occupied the first position in the market. In addition, with the announcement of Huobi's withdrawal from the Chinese mainland market, although it was still second, the gap between Huobi and Binance has already gotten very large.

OKX performed well this year. Although it was also affected by the policies of the Chinese mainland, OKX began to expand overseas markets in 2022. At the same time, after the incident of FTX misappropriating user funds, it responded quickly and soon announced the wallet address of the exchange and the Merkel Tree proof of assets that users can verify. It has become second place in terms of market share of derivatives.

Decentralized Perpetual Contract Trading Protocol

What truly marks the beginning of decentralized derivatives trading should be after Layer2 officially starts to run. The two main representative projects are dYdX and GMX. Of course, we mainly discuss perpetual contract-type trading products. Options, synthetic assets, and other categories, for the time being, are not discussed.

After dYdX issued $DYDX in August 2021, the transaction volume on its platform also increased significantly. On August 1st, the cumulative trading volume of dYdX was $3.4B, and 4 months later, at the end of the year, the cumulative trading volume reached $322.6B, an increase of nearly x95.

The average daily trading volume of GMX in the last two months was about $250M. Compared with the centralized exchange, this figure is almost half of the trading volume of the BitMEX exchange.

The above data on decentralized perpetual contracts transactions was almost zero at the beginning of last year. According to the data collected by TokenInsight, we have found more and more decentralized protocols focusing on this area, and we will see more in the future. Of course, we also have reasons to believe that in the future, the market share of decentralized derivatives will increase, just like what happened to decentralized spot exchanges.

Why Do We Need Decentralized Derivatives Exchanges?

Advantages of Decentralization

Decentralized protocols tend to provide greater transparency

All transaction data on DEXs is transparent, and anyone can check every transaction record on the blockchain explorer. Users can get valuable insights through on-chain data analysis, such as tracking whales' activities, identifying rat trading and wash trading, etc. In CEXs, every transaction record and the assets in reserve are not disclosed, like a black box. Users need to trust CEXs completely, which also gives CEXs a lot of possibilities to do evil.

Decentralized protocols allow users to have control of their assets at all times

CEXs often require traders' assets to be held in custody on the platform, and they will be responsible for managing user funds. Users need to trust the platform will not misuse their assets and that there will be no centralized problems, such as a bank-run crisis, that could compromise the integrity of their assets. DEXs, on the other hand, require users to connect to their cryptocurrency wallets and have control over their funds (Self-Custody) before they can use them.

Decentralized protocols improve censorship resistance and privacy

As cryptocurrencies' economic and political influence grows, government regulations are becoming increasingly stringent. Since CEXs exist as a distinct legal entity in nature, it is more likely to be subject to the laws and regulations of the countries in which it operates, such as KYC (Know Your Customer) and AML (Anti-Money Laundering), and users are often required to upload personal information, documents, etc. when registering. US users trading on CEXs with a valid license are even required to report US taxes annually, just as they do for stock trading. DEXs, on the other hand, can be thought of as a protocol consisting of codes rather than legal entities. Therefore, DEXs are naturally censorship-resistant and require no KYC verification for users.

On-Chain Composability

Due to the Permissionless nature of DEXs, many DEXs products can be considered not only as standalone products but can also be integrated by other DeFi products and provide underlying liquidity. This puts DEXs in the liquidity layer between the L1/L2 and the application layer and can play a Lego-like role in the DeFi ecosystem in the future, with a high degree of on-chain composability and interoperability.

Yield Aggregator

In July 2022, in partnership with GMX and TracerDAO, Umami Finance launched USDC Vault. The mechanism is that 50% of the $USDC deposited by users will be minted for $GLP, and the other 50% will be used to hedge the $GLP exposure in TracerDAO. In Q4 of the same year, Umami Finance will launch GLP Vault.

Meanwhile, as of November 23, 2022, Umami has referred $160,000,000 in trading volume on GMX through GMX's referrals program (i.e., new users receive a 10% fee reduction for using "umami" referral codes), earning $18,000 in rebates to add to its treasury.

DeCommas

DeCommas is a cross-chain DeFi automation layer. It has developed a GLP delta-neutral strategy, where 50% of the USDC deposited by users will be minted as $GLP; the other 50% will be hedged on Aave. From Aave, the vault will borrow $BTC and $ETH and then sell both assets for USDC, creating a short position on the crypto assets. This can hedge the impact of market volatility on risky assets in the portfolio. The strategy is expected to be released in Q1 2023.

Users can deposit $GLP in the $GLP farm, and the platform allows automatic reinvestment, while the official GMX platform requires users to reinvest and pay gas fees manually. Yield Yak's solution will enable users to get a higher APY than staking on the GMX platform, provided that $GLP will be converted to $fsGLP on Yield Yak.

Lending

Vesta Finance is a DeFi lending protocol built on Arbitrum. Through the GMX Vault and GLP Vault, users can deposit $GMX or $GLP to borrow the platform's stablecoin, $VST.

Insurance/Cover

$GMX holders can purchase cover on Nexus Mutual, which means that in the event of contract failure, economic attacks (including Oracle failure, etc.), and governance attacks, users can receive the equivalent of their lost funds in ETH up to the covered amount.

What Challenges Are Decentralized Derivatives Exchanges Facing?

Lower liquidity compared to centralized exchanges

CEXs typically offer market-making services as a counterparty to provide users with more liquidity for buying and selling cryptocurrency, rather than relying solely on the user's own trading needs, thus providing higher liquidity. Many DEX products are limited by LP and trading volume and therefore have much smaller liquidity pools, which can result in higher slippage and impermanent losses for participants.

Higher transaction costs

Users only need to pay relatively low trading fees to CEXs. For example, BitMEX has a taker fee of 0.075% and a negative maker fee of -0.010%, which means that users can even get a rebate from the platform. DEXs, on the other hand, tend to charge higher trading fees and, due to their decentralized nature, have to bear additional on-chain processing costs, but these costs can be meager in Layer 2, e.g., Arbitrum.

Steeper learning curve and higher barrier to entry

CEXs provide a better user experience, similar to a traditional investor buying and selling stocks. DEXs, on the other hand, require users to learn new trading rules due to product innovation, which undoubtedly causes a steeper learning curve and a higher user entry barrier.

Fewer product features

Currently, the decentralized derivatives exchange is still in the early stage of development, and the product functions are mainly perpetual contracts and spot trading. In contrast, CEX, after years of development, now has more diversified derivatives product features to meet rich user needs, such as coin-margined futures contracts, grid trading strategies, etc. Moreover, the trading pairs available on DEXs are much smaller than on CEXs, e.g., Binance supports hundreds of pairs, while dYdX and GMX support only 38 and 8 pairs, respectively.

Major Players Nowadays

In this section, we will focus on four major players among the decentralized derivatives exchanges, GMX, dYdX, Perpetual Protocol, and Drift. First, we will briefly introduce each project from a general perspective, hoping to give readers a brief overview of the project. Next, we will provide an in-depth analysis of these protocols, including the project mechanism, fee structure & distribution, token economics, and security. We will compare the above aspects of the projects so that readers can comprehensively better understand the current decentralized derivatives market.

Intro

GMX

GMX is a decentralized perpetual exchange created by an anonymous team. GMX launched on Arbitrum on September 1, 2021, and went live on Avalanche on January 5, 2022. GMX currently supports spot swap and perpetual contract trading up to 50x leverage. Supporting orders include market orders, limit orders, and trigger orders (take profit/stop loss orders).

The core mechanism of GMX is its GLP liquidity pool, which consists of a basket of assets. GLP exists as the counterparty to traders in trades and provides liquidity for all trades on the platform. Moreover, GMX uses a dynamic pricing mechanism to execute trades with zero slippage, by feeding prices through the dynamic aggregation oracle provided by Chainlink.

GMX has two native tokens. One of them is $GMX. $GMX is the utility and governance token of GMX. Holders of $GMX can participate in governance voting and stake tokens for rewards. Another token is $GLP. $GLP is GMX's liquidity provider token. Holders of $GLP, known as LP, can receive a certain percentage of the platform's trading fees as a reward for their provision of liquidity.

dYdX

dYdX is a decentralized derivatives trading protocol deployed on the Ethereum network as a layer2 rollup and powered by ZK StarkEx, founded by Antoni Juliano in August 2017. dYdX's core team consists of software engineers from well-known cryptocurrency companies such as Coinbase.

dYdX adopts the order book mechanism familiar to traditional market makers to execute trades, providing traders with a wide variety of orders and ample liquidity during trades. As for now, dYdX's trading products are primarily perpetual contracts. dYdX supports perpetual contract trading with up to 20x leverage and slippage tolerance setting.

In addition to its well-known order book trading mechanism, dYdX chooses the scalability engine from the Layer2 solution company, Starkware to increase its trading throughput and reduce gas fees and transaction fees. However, the order book mechanism of dYdX and the reliance on the external trading engine somewhat increase the centralization of dYdX. According to dYdX's disclosed v4 development plan, dYdX plans to transition from Starkware to its native Cosmos-based appchain, dYdX Chain, to create a fully decentralized derivatives exchange.

$DYDX is dYdX's native governance token. In addition to governance voting, holders of $DYDX can receive discounts on trading fees based on the size of their holding positions. Moreover, $DYDX holders can stake their tokens to the security pool to receive rewards.

Perpetual Protocol

Perpetual Protocol (Previously known as Strike) is a decentralized derivatives trading protocol co-founded by Yenwen Feng and Shao-Kang Lee. Perpetual Protocol was originally launched on Gnosis Chain (formerly xDai) in December 2020. Its v2 version, Curie, was launched on Arbitrum in November 2021.

Perpetual Protocol's primary products are perpetual contracts. Currently, Perpetual Protocol supports market orders, limit orders, and stop orders. It supports perpetual contract trading with up to 10x leverage and slippage tolerance setting.

Perpetual Protocol uses the virtual AMM (vAMM) trading model as its core trading mechanism. While vAMM also uses the same constant function used by the AMM model, unlike the traditional AMM model, vAMM acts as a price discovery tool only, with no real liquidity and no counterparties during the trade. However, vAMM v1 might suffer from the long-short skew problem caused by open positions and the high slippage problem. To address the high slippage issue, Perpetual Protocol introduced its v2 version, which uses Uniswap v3 as the execution layer to provide centralized liquidity to reduce trading slippage. In addition, v2 adds a cross-margin mechanism and multiple collaterals, while allowing permissionless market creation.

$PERP is the native utility token of Perpetual Protocol. The primary function of $PERP is governance. Holders of $PERP can participate in governance voting or stake tokens for rewards.

Drift

Drift Protocol is a decentralized derivatives trading protocol co-founded by David Lu and Cindy Leow. The core contributing team behind Drift is Drift Labs.

Drift v1 was launched on Solana in November 2021. Currently, Drift v2 is live on its gated mainnet and possibly will go live to the public soon. Right now, Drift supports spot trading, perpetual contract trading with up to 10x leverage, lending, and passive liquidity provisioning. Order types supported by Drift include market orders, limit orders, and advanced conditional orders (e.g. stop-limit orders).

Drift is similar to Perpetual Protocol mentioned above. It also uses the vAMM model as its core mechanism. The major difference is that the liquidity of Drift's vAMM model is dynamically variable, so it can provide deeper liquidity around price to address the slippage problem. Meanwhile, Drift v1 is combined with the order book mechanism that allows users to submit limit orders against vAMM. Drift v2 is an upgraded version of v1. Compared to the v1 version, v2 adds a Just-In-Time (JIT) liquidity auction mechanism and passive liquidity pools to incentivize market makers to provide more liquidity for trading.

Currently, Drift Protocol has not issued its own native token yet.

Mechanism

One of the core problems to be solved in decentralized derivatives trading is liquidity. In terms of this core mechanism, dYdX, GMX, Perpetual Protocol and Drift have implemented it in several completely different ways.

The traditional model of dYdX attracts market makers to provide liquidity, but the degree of decentralization is lower than that of GMX.

dYdX is more inclined to traditional centralized exchanges, using the orderbook method as the core mechanism. Traders are counterparties to each other, and the protocol itself only provides functions as a platform. However, it is definitely not enough to rely on ordinary users to provide liquidity. Therefore, dYdX has designated several institutional market makers to provide liquidity since its launch. dYdX also reserves a certain percentage of $DYDX as an incentive for these designated market makers.

The implementation of dYdX’s on-chain orderbook relies on its construction on Layer2. The orderbook is different from AMM in that it reduces the barriers for users and market makers to participate in transactions, and can provide continuous liquidity over time. It is also an established model familiar to traditional market makers. dYdX hosts its trading and matching engine through Amazon Web Services (AWS). Notably, dYdX is not strictly a fully decentralized derivatives exchange, as its orderbook and the trading matching engine is still centralized. But dYdX is actively developing v4, expected to be launched in Q2 2023, which will feature a fully decentralized orderbook and matching engine, and achieve extremely high throughput.

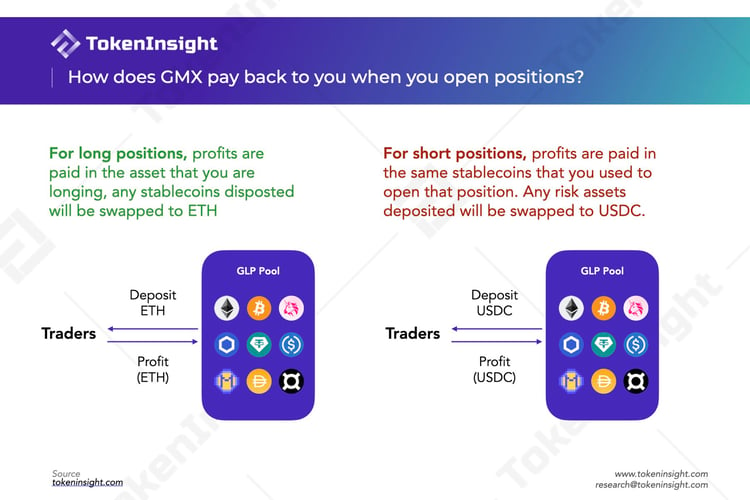

Instead of using dYdX's orderbook model, GMX has innovated a GLP mechanism. The GLP liquidity pool provides liquidity for trading and it consists of a variety of assets, including wBTC, wETH, stablecoins, etc. Under this mechanism, the platform divides its users into two categories: traders and liquidity providers.

With regard to traders, to make a leveraged trade, they need to first deposit collateral into the GLP pool. According to the rules of the exchange, the collateral for shorts and longs is different.

For instance, when a trader is long ETH, it can be described as the trader "renting out" ETH from the GLP pool, while when a trader is shorting ETH, he is "renting out" the stablecoins versus ETH from the GLP pool, thus corresponding to two different collateral. The assets in the pool are not actually lent. When a long position is closed, if the trader makes a profit, the long asset (in this case ETH) is withdrawn from the GLP pool and given to the trader as profits, while in case of a loss, the asset initially deposited is deducted and put into the GLP pool, i.e. the token of the profit and loss corresponds to the token of the collateral. The GLP pool is therefore equivalent to the trader's counterparty.

As for liquidity providers, $GLPs can be minted/burned by depositing/withdrawing a specific asset into the GLP pool, with a fee charged for both minting and burning. Each type of asset in the pool has a corresponding target weight, which is adjusted based on market conditions. If the current weight of an asset is higher than the target weight, a higher fee will be charged for depositing that asset, and as an incentive, the fee for withdrawing the asset will be reduced, and vice versa.

GLP pools are priced by an oracle provided by Chainlink, which is based on some centralized exchanges such as Binance and Bitfinex. This makes GLP extremely capital efficient. Trades can be executed with zero slippage, as GMX pulls prices in real time from CEXs to give traders the best execution, and LP’s are protected from suffering impermanent loss, as GLP LPs need not incur the cost of price discovery.

Perpetual and Drift seek to correct the weaknesses of AMM, but the effect has not yet met expectations.

The AMM mechanism proposed by Uniswap uses a constant function of x*y=k to implement token swaps, but this mechanism is not suitable for derivatives trading and suffers from high slippage and impermanent loss. To address the limitations of AMM, Perpetual Protocol proposed virtual AMM (vAMM). Although implemented using the same formula, there is no actual storage pool of assets (k). Tokens are eventually stored in a vault via a clearing house, and vAMM is only used for price discovery. Since liquidity does not need to be provided by the liquidity providers but by the traders themselves, there is no impermanent loss. Combined with the fact that the k value is set manually by the operator according to market conditions, vAMM achieves slippage management to a certain extent.

However, vAMM v1 is not suitable for highly volatile markets, relying on insurance fund when open interest is heavily skewed, and traders still face high slippage. In order to solve these issues, vAMM v2 is combined with Uniswap v3 as the execution layer, which introduces liquidity providers that allow each transaction to occur directly between the trader and market maker via a liquidity pool, reducing the involvement of the insurance fund in skewed markets and making the protocol more secure. In response to slippage, Uniswap v3 allows liquidity providers to provide liquidity within a custom range, and each position is then aggregated into the pool, so that large transactions will be spread across multiple positions, thereby reducing slippage. However, the new problem is that the liquidity provider has no losses only in the initial state (when the price has not deviated), which is very unfriendly to them and makes vAMM v2 unattractive to LPs. The Perpetual Protocol team is currently providing liquidity to the market itself to support tradings.

Drift initially focused on the vAMM model as well - just like Perpetual. Based on the Perpetual Protocol v1 model, Drift introduces dynamic k-values to implement Dymatic AMM (DAMM). By introducing a dynamic k, liquidity rebalances, allow for deeper liquidity around current prices. The depth of liquidity will not get out of control as the price gets farther and farther away from the initial price level of the perpetual contract, ensuring that liquidity is sufficient under any market conditions. Also, Drift is integrated with the orderbook, allowing users to submit limit orders.

But has the problem of static k been completely solved?

Not really. Although the position on Drift can be closed directly without reaching the final price, its funding rate has seriously deviated from the funding rate of the perpetual contract on CEX, because the problem of market skew has not been really resolved. For example, when LUNA prices plummet, Drift needs a large number of short positions to keep prices accurate, meaning that longs pay extremely high funding rates to do so. Overall, the vAMM model makes it difficult for such DEXs to reflect real market prices. This failure led Drift to decide to discontinue the v1 and focus on the second generation.

Drift v2 adds two liquidity mechanisms to the original decentralized orderbook - just-in-time liquidity auctions and AMM liquidity. When a trader submits a market order, an auction is generated for that order allowing market makers to compete with each other to achieve a better price to satisfy the order. If the market maker does not step in within the first 5 seconds, the order will be satisfied through DAMM. This improves pricing and liquidity depth, enabling orders to be filled with minimal slippage, and at the same time reducing the risk of AMM long/short imbalances, but the exact effect remains to be tested in the real market.

Overall, from a mechanistic point of view, although the orderbook model has brought high trading volume to dYdX, the degree of decentralization is much lower than that of GMX, Perpetual and Drift. Through analysis, it’s not difficult to find that the vAMM model has certain drawbacks and is not applicable to the current market for the time being. Perpetual and Drift need to further explore this model.

Fee Structure and Allocation

Due to the orderbook mechanism, dYdX uses the Maker-Taker price model to determine transaction fees. Depending on the volume traded in the previous 30 days, Maker is charged 0-2bps, while Taker is charged 2-5bps. It is worth noting that no transaction fee will be charged when the transaction volume in the past 30 days is less than $100,000. This is to encourage individual investors to participate in the transaction, and the fee will only be charged for orders that have been filled. Additionally, depending on the amount of DYDX and $stkDYDX tokens held by users, there will also be discounts of up to 50% on transaction fees. Unlike other protocols, all fees collected belong to the dYdX Foundation and will not be distributed to token holders.

Compared with dYdX, GMX has more sources of transaction fees. There are two main parts: one is the fees incurred when minting/burning $GLP. As mentioned above, 0-80bps fees are charged according to the current weight; the other part comes from margin trading, where the transaction fee is 0.1% of the total position. At the same time, in margin trading, a "renting fee" is charged to the GLP pool. The calculation formula is Assets Borrowed / Total Assets in GLP* 0.01%, and it will be charged every hour. 70% of the fees charged by the platform will be distributed to $GLP holders, and the remaining 30% will be distributed to stakers of $GMX.

The fee mechanism for Perpetual and Drift has also changed as a result of the upgrade to the model. A transaction fee of 0.1% is charged on every transaction on Perpetual Protocol v2. Compared with v1, v2 has broadened the fee sources: while v1 fee income comes only from the public market, v2 includes private markets on top of that, as well as rehypothecation (Funds in the insurance fund may be utilized in low-risk interest protocols to increase staker earnings). There are two scenarios for fee allocation: when the insurance balance is less than the insurance threshold, 20% of the fees are deposited into the insurance fund and 80% are allocated to liquidity providers (Market Makers); if the insurance balance is greater than the insurance threshold, the fees flowing into the insurance will be evenly distributed to DAO Treasury and $vePREP holders.

Since part of Drift's liquidity comes from the orderbook, its fee structure is more similar to that of dYdX, which is also based on the trading volume in the past 30 days. Takers are charged 5-10bps, and, notably, Makers are charged a fixed 2bps, a significant difference from dYdX. In addition, 90% of the transaction fees charged by DAMM are distributed to the liquidity providers based on the proportion of liquidity provided by them.

In summary, dYdX and Drift are very similar in terms of fee structure, but overall Drift costs slightly more than dYdX. Compared with these two DEXs, GMX and Perpetual have richer fee sources. In addition, dYdX does not allocate income to token holders or liquidity providers. Even though token holders can enjoy transaction discounts, from this perspective, it will be slightly inferior to the other three protocols in terms of user incentives.

Tokenomics

GMX, dYdX and Perpetual all have their own governance tokens except for Drift, and token holders can also be rewarded by staking tokens. There are differences in the specific reward allocations.

100% of GMX revenue is distributed to $GMX and $GLP holders. The total reward for $GMX holders is 30% of the transaction fee (in the form of ETH or AVAX) plus $esGMX tokens and multiplier points obtained from staking. $esGMX can also be re-staked like $GMX to get the same benefits, or exchanged for ordinary $GMX tokens after a one-year lock-up period. $GMX/$esGMX stakers can also receive multiplier points with 100% APR per second, which can also be staked again, aiming to incentivize the holder to keep staking $GMX. And once the user withdraws the staked $GMX, the corresponding proportion of multiplier points will be burned. Similarly, $GLP holders earn 70% of transaction fees (in the form of ETH or AVAX) plus $GMX obtained by staking. It is worth noting that the $GLP price is positively correlated to the asset price in the GLP pool, and liquidity providers indirectly benefit from the potential appreciation of the assets.

Similar to GMX, holders of $DYDX on dYdX can stake tokens to the Safety Module to mint $stkDYDX. $stkDYDX has the same proposal and voting rights as $DYDX in terms of governance. The safety module is primarily used to incentivize holders to properly govern the protocol, and act as a risk manager in the system at the same time. As an incentive reward, 2.5% of the initial supply of $DYDX is allocated to users who stake $DYDX according to the fees generated by user transactions and the percentage of open interests. In addition, 7.5% and 25% of the initial token supply are also used for liquidity provider rewards and trading rewards to incentivize their participation in trading activities on dYdX.

$PREP tokens are also available for governance and staking on the Perpetual Protocol. Holders of $PREP can stake it in the staking pool for a fixed period of time to mint $vePREP. The risk is that if the insurance fund is exhausted in extreme market conditions, the staked tokens will be sold through the protocol; and as compensation, the stakers can receive weekly rewards (fee allocation).

It is not difficult to find that all three protocols encourage token holders to participate in protocol governance and staking, but the effect varies greatly: GMX introduces $esGMX and multiplier points to encourage holders to continue staking, which has a positive effect on the development of tokens and protocols; dYdX allocates initial token supply to incentivize users, but the accompanying problem is that some traders will trade heavily on the day before pass allocation (every 28 days) to increase transaction volume and thus obtaining more token rewards, leading to token price fluctuations; although holders of $vePREP can also be rewarded, the reward is only 10% of the transaction fee and has a prerequisite, so it is not conductive to incentivizing stakers.

Security

As mentioned above, traders are required to deposit corresponding collateral before trading on GMX. GMX uses partial liquidation, where the liquidation price is calculated as the price at which the (collateral - losses - borrow fee) is less than 1% of the position's size. If the token's price crosses this point, liquidation is triggered and then the position will be automatically closed. Since traders can choose up to 50x leverage, the higher the leverage, the higher the liquidation price. With the increase of borrowing costs, the liquidation price will gradually increase, requiring users to monitor the liquidation price to avoid liquidation.

In addition to the liquidation mechanism, GMX also has security measures against platform attackers. The attack originated in September 2022: the attacker first opened a position at GMX, then manipulated the AVAX price at FTX, and finally benefited by closing the position on GMX. The attack caused the liquidity provider to lose about $570,000. In response to this incident, GMX protected the exchange from further manipulation by limiting short and long positions on AVAX/USD, making the cost of manipulation higher than the potential gain. Besides, GMX also launched a bug bounty program in October. Rewards are distributed according to the severity and impact of vulnerability to protect smart contracts and applications from issues such as fund theft, price manipulation, and theft of governance funds.

Unlike GMX, dYdX decides whether to liquidate based on account value and margin requirements: when the account value is less than the maintenance margin requirement, the account will be liquidated using different formulas depending on the position. Profits and losses resulting from liquidation will enter the insurance fund, and if the insurance fund is exhausted, a deleveraging mechanism is used as a last resort to protect the system: the underwater accounts are offset by reducing the positions of the high-profit and high-leverage accounts, thereby maintaining the stability of the system.

The liquidation mechanism of Perpetual is similar to that of dYdX in that the margin ratio is obtained by dividing the collateral value by the nominal value. Only if the ratio is greater than 6.25% can it avoid being liquidated. If liquidation is triggered, the maximum liquidation percentage varies depending on the margin ratio: when the margin ratio is between 6.25% and 3.125%, 50% of the trader's position is liquidated, while when the margin ratio is less than 3.125%, 100% of the position is liquidated.

In addition, Perpetual's insurance funds are also used to protect the perpetual market. When the perpetual market is heavily skewed, the insurance funds will be used to pay high funding rates. If the insurance fund is depleted, a smart contract is triggered that mints new PERP and subsequently sell them for collateral in the vault to protect the system’s solvency.

Drift also calculates the margin ratio, and the position will be eligible for liquidation by liquidators when the account maintenance margin ratio drops below the minimum maintenance margin. In addition, "Health" is also calculated on Drift by the formula log(max(0, margin ratio - maintenance ratio) + 1). The Health measure on the user page can help visualise how close a user is to liquidation territory. At 0 Health, a user can get liquidated, and the positions will be liquidated using margin engine prices.

Overall, dYdX, Perpetual, and Drift all use margin to determine whether to liquidate. In addition to liquidation, GMX and Perpetual also have related security measures against attacks or market conditions. Although dYdX also has a similar safety module to deal with protocol bankruptcy or other issues, it is no longer effective after November 28.

Data Performance

In this section, we compare the market performance of several decentralized exchanges over the past period, including market volume, open interest, revenue, active users, and other indicators, in order to understand the current state of decentralized derivatives exchanges.

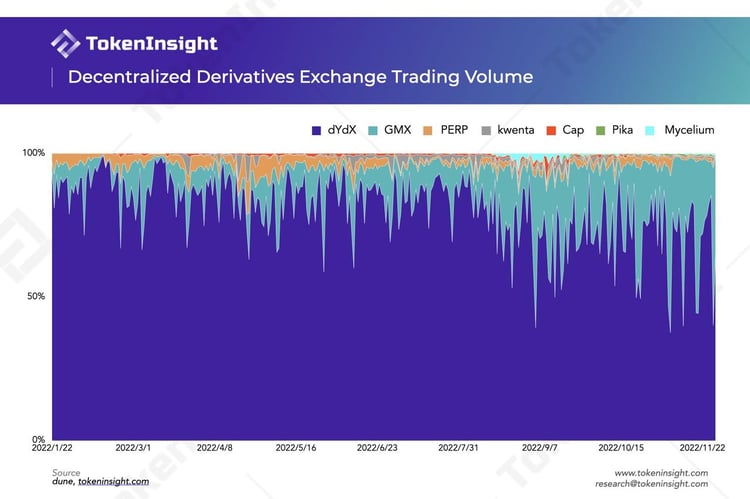

Decentralized Derivatives Exchange Volume

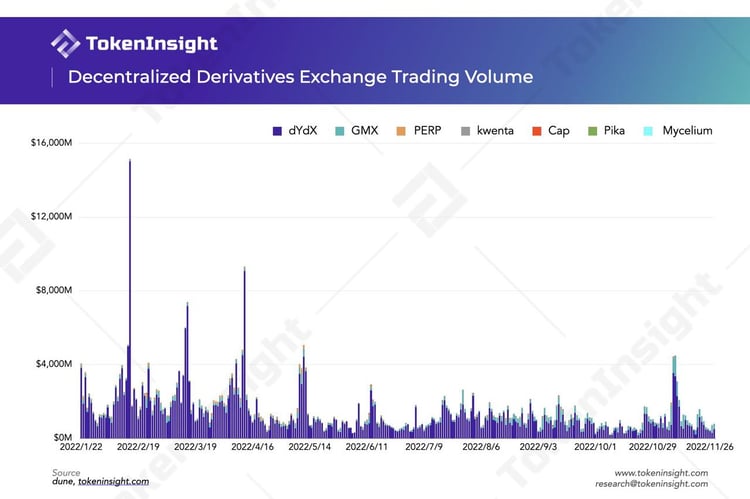

In terms of the trading volume market shares, dYdX has an absolute advantage over others, especially at the beginning of this year, before GMX was widely known. Overall, it holds more than 70% of the market share. The high trading volume of dYdX is inseparable from its order book and having designated market makers to provide liquidity. Users can use trading strategies similar to centralized exchanges, and low transaction costs, support for API transactions can also support more frequent transactions.

GMX as a "rising star", innovative mechanisms, considerable real returns (ETH rewards), and the expansion of Layer2's own user base have all promoted the development of GMX. Since the third quarter of this year, GMX's market share has increased significantly, and in some periods it can even gain more than half of the market share.

The remaining protocols account for only a small part of the total volume and are less competitive at this stage.

The trend of trading volume of various exchanges in 2022 is basically the same, dYdX has been in a dominant position in the early stage, and its ATH 24H trading volume even exceeded $15B. Since Q2, the overall trading volume has declined due to the impact of events such as the bear market and Terra. The FTX thunderstorm incident in early November caused a large number of traders to withdraw from centralized exchanges and switch to decentralized derivatives exchanges. As a result, the trading volume peaked during this period, and then fell back to a lower level.

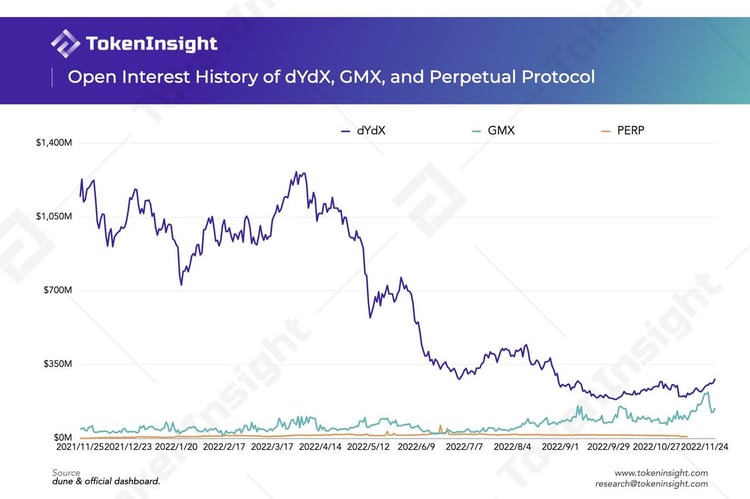

Historical open interest volume

Before 2022 Q3, dYdX held the highest open interest, far exceeded the other two, and then all the way down to the lowest 190 million US dollars, only about 15% of the peak. Of course, this is not dYdX's own reason, but the impact of the market environment. Since the beginning of this year, due to the overall market turning to bear and mixed with various storms, the high leverage and market credit expansion in the Bull Market last year were gradually forced to break down this year.

While for GMX, its OI has been growing steadily and even had a trend of surpassing dYdX at one point. One of the core catalysts is of course that many users have begun to switch to decentralized protocols. The increase in the size of GLP assets in GMX has also enabled its platform to support greater liquidity and provide users with more trading opportunities. And more user influx and trading behavior will attract more users to GMX to provide liquidity to earn rewards. In contrast, PREP has performed mediocre and is relatively weak in competitiveness.

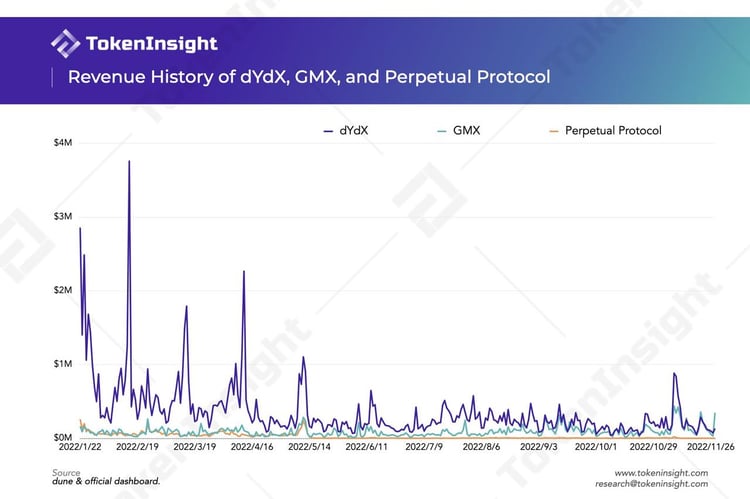

Historical revenue from dYdX, GMX, and Perpetual Protocol

Similar to the trading volume, dYdX's revenue in the first half of this year also far exceeded that of the other two decentralized exchanges. The reason might be that the trading volume of dYdX is much higher than that of these two. Even though transaction fees are lower and there are certain discounts, the overwhelming advantage in trading volume still brings considerable revenue to dYdX.

On the other hand, as mentioned above, dYdX does not distribute revenue to token holders, and all revenue goes to its Foundation. Other exchanges distribute all or part of the fees to token holders or liquidity providers. dYdX was even surpassed by GMX for a few days in November this year, and GMX's revenue is expected to continue to grow.

Comparison of cumulative users and total value locked

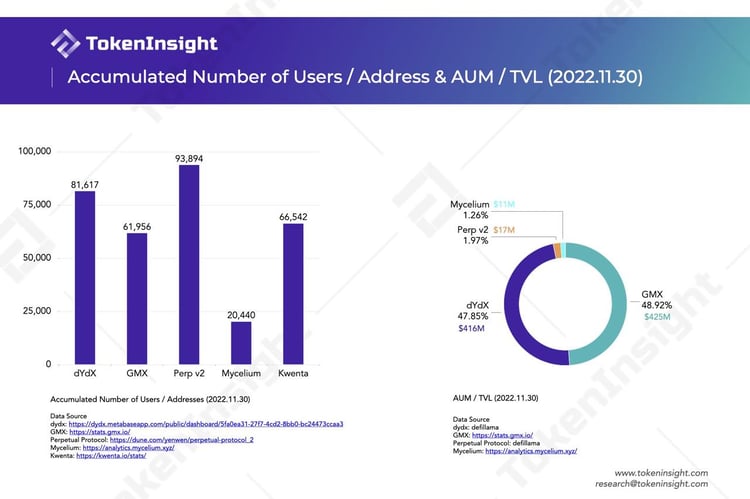

Comparing the cumulative number of users of various exchanges on November 30, 2022, we can see that Perp v 2 has the highest number of users at 93,894. This data comes from Dune Dashboard created by Yenwen (The founder of Perpetual protocol). The highest number of users with low trading volume and TVL is somewhat abnormal.

Aside from Perp v2, dYdX has the largest cumulative user base of any other protocol. Mycelium is currently in a low position in terms of user volume after changing its name from Tracer DAO. In terms of TVL, GMX has the largest GLP asset size and has slightly surpassed dYdX. But the two protocols basically each occupy half of the market.

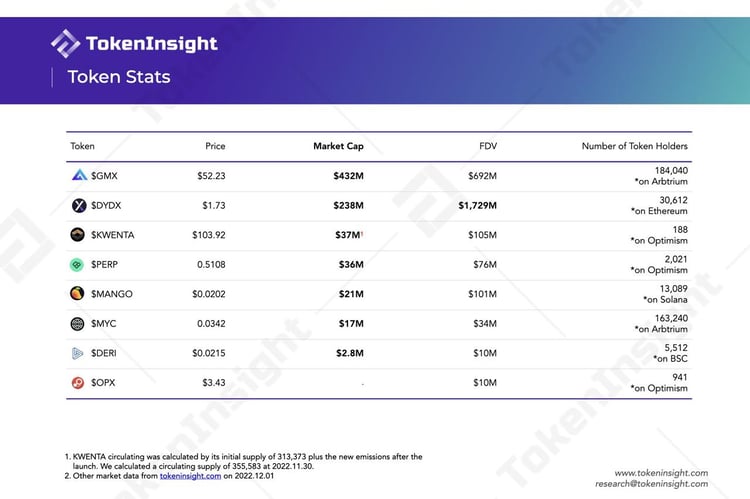

Token Stats

The table above summarizes the Token performance of some decentralized derivatives protocols.

In terms of market capitalization, $GMX is the highest, followed by $DYDX. It is worth noting that the market capitalization of $GMX is almost twice that of $DYDX. The market cap of $KWENTA is also as high as $37M, but $KWENTA has just been issued. The current circulation is only the initial emission and a small number of releases in the first few weeks. As a new token, $KWENTA has the smallest number of holders, only less than 200 addresses.

In terms of fully diluted valuation (price * total amount of tokens), $DYDX is the highest, mainly because a large amount of $DYDX has not been unlocked. The $DYDX initially allocated to teams, investors, employees, etc. will be unlocked in February next year, resulting in a significant increase of $DYDX circulation. TokenInsight has updated the $DYDX unlock plan. Click the link to view.

The Next Step

This section aims to provide a brief comparison of the development path of each exchange based on their roadmaps and related disclosures. Through this comparison, we hope to provide readers with further insight into the future trends of the decentralized derivatives exchange track.

Provide more diverse trading mechanisms and products to gain market share

According to the discussion of GMX DAO's development plan for 2022 in the forum, GMX will continue to develop the platform mainly in three dimensions: enhancing platform reliability and interface improvements, supporting synthetic tokens, and deploying X4 and new chains.

From the development priority level, although the deployment of the new chain itself will only take a month or so, according to the GMX team, specific matters such as liquidity and on-chain monitoring are the real challenges that the new chain's facing. Meanwhile, the team is also concerned that the new chain development might cause GMX to be left behind by other players, who are constantly improving their products. Therefore, the synthetic trading market, which is relatively less difficult to develop, will take precedence over X4 and the new chain, and this decision means that gaining more market share is still GMX's primary goal for now.

X4 is intended to attract more derivatives traders by offering a more flexible and diverse trading mechanism. This new version will propose a customizable AMM that gives pool creators and projects full control over the functions of its pool. This means that when a pool is created, the creator can specify any custom behavior that they would like on adding liquidity, removing liquidity, buying, and selling. In addition, X4 proposes to build a PvP AMM that matches traders against each other while optionally allowing liquidity providers to participate. This means that the whitelist no longer exists and all kinds of assets can be traded. Theoretically, this trading model supports uncapped trading liquidity.

Besides, according to the GMX team's statement in the forum in May this year, in terms of time taken, both PvP AMM and X4 would likely take around 3 months each to launch, and the project is now significantly behind schedule.

Deploying new chains for the vision of fully decentralized

The dYdX team is currently working on the v4 release and recently completed the second phase of v4, the deployment of the internal testnet. According to the news earlier this year, dYdX's v4 was scheduled to land by the end of 2022, while in the latest disclosed development progress, the complete dYdX v4 will be deployed by 2023 Q2 after the completion of the third phase of advanced feature development, the fourth phase of public test network launch and the fifth phase of mainnet launch.

With an emphasis on DAO construction and platform performance enhancement, dYdX aims to realize the vision of building a fully decentralized trading platform with v4. While the current v3 version still relies on a centralized system for the orderbook and matching engine, v4 will introduce a fully decentralized off-chain orderbook and matching engine that will hopefully expand throughput by several orders of magnitude. In addition, trading products such as spot trading, which were once deprecated with the ETH Layer 1 version, are expected to return to the trading platform with the v4 version.

With the v4 release, the platform's development team, dYdX Trading Inc., will also be handing over operations to the community and will no longer take revenue from transaction fees. The community currently plans to create an Operations subDAO to support the smooth transition of the platform's operational structure.

Besides, dYdX will develop its own standalone blockchain in the Cosmos ecosystem, and expand dYdX v4 to it. The new chain will be built based on the Cosmos SDK and the Tendermint Proof-of-Stake consensus protocol.

When asked about the competition among decentralized derivatives exchanges in the future by TokenInsight, Nathan Cha, Senior Marketing Associate of dYdX replied.

“We think in the long run, there will be concentration in the hands of few players in the derivatives like we see currently in the DeFi Spot, swap or lending markets with Uniswap, MarkerDAO and AAVE which we admire. Hence, building a powerful DeFi tool with easy UX is key and as long as its owned by the community and its users makes concentration a relatively a small problem.”

"The alliance of derivatives exchanges"

In terms of development plans, Perpetual Protocol and Drift Protocol do not show particularly clear development ambitions. Perpetual Protocol is currently focused on increasing the types of collateral supported by the platform and completing USDC fee distribution, but the project is also experiencing slow development considering the expected completion time on its roadmap. Drift Protocol recently launched v2, which aims to achieve greater liquidity and improve the platform's collateral profile.

Notably, Perpetual Protocol, Drift Protocol and GMX recently announced a partnership with blockchain data analytics platform Nansen to build a Dashborad that will allow traders to monitor trading platform data in real-time. Through this partnership, the alliance of derivatives exchanges hopes to revive traders' confidence during the winter brought on by the FTX incident, while re-emphasizing the core concepts of the DeFi industry, namely transparency, immutability, and decentralization, and calling on other decentralized exchanges to join the partnership.

When asked about the problems that need to be solved to accelerate the development of decentralized derivatives trading, Burt Rock, Head of Marketing at Kwenta replied.

"First, let’s recognize how new of a concept we’re dealing with when we talk about decentralized derivatives trading. Back in 2016-2017 we had some basic proof of concept synthetic assets, but the layer 2 scaling solution we’re using to build a fully decentralized perps AMM on Ethereum is less than 2 years old. I think it’s great we’re already talking about performance, fees, and really trying to offer a competitive product, but we’re still talking about something that’s quite nascent and needs a ton of development from all sides.

That being said, I think we actually have a great handle on what problems need to be solved. First, we need low latency decentralized oracles, and faster execution on L2s. Some exchanges have made sacrifices on decentralization or security for the sake of performance, but for a true DEX to shine, we need to be able to fetch prices and submit orders in seconds, or even milliseconds without cutting corners.

From a UX perspective, we also need to start streamlining the trading experience without compromising security too much. If you’ve ever tried trading perps with a hardware wallet, it’s a nightmare to sign every transaction. Ideally users should only have to sign transactions once per session, the same way you only sign in to a CEX once and then trade at your leisure from the window.

Lastly, onboarding from a user’s checking account or other traditional institution is still a huge challenge, and unfortunately this isn’t a challenge I’m sure we can solve simply by building smart contracts or web applications. We still some entity that plays nice with regulators to help onramp users, and we need education and outreach to teach people how to use the available tools."

Brief Sum-up

It is obvious that the biggest shackle facing decentralized derivatives exchanges is still the problem of insufficient liquidity. The major players have coincidentally chosen some similar solutions, such as improving the product experience and expanding the product matrix to increase user-friendliness, in order to reach more traders and thus capture more market share. Both GMX and dYdX chose to build their own chain, to further develop the platform ecology.

Having a standalone blockchain seems to be the general trend in the development of decentralized derivatives exchanges. However, the full deployment of a new chain is difficult and time-consuming. With the market changing rapidly, as in the GMX team statement, it is more important to gain more traders in the shortest possible time. Traders' trust is based on the transparency, immutability, and decentralization of the platform, and the aforementioned alliance also supports the importance of implementing the core concept for market confidence. From this perspective, it seems that dYdX, which is committed to full decentralization, will deliver more impressive results.

New Entrants

In addition to the four previously mentioned platforms, the decentralized derivatives trading track is not without some up-and-comers. This section will briefly introduce a few derivatives trading protocols that include perpetual contract trading and try to explore the growth potential of these new entrants, providing readers with a new perspective on this track.

Mycelium

Mycelium is a decentralized derivatives protocol, formerly known as Tracer DAO. It is deployed on the Arbitrum and Rinkeby networks. Mycelium primarily supports perpetual contract trading, which offers up to 50x leverage trading.

The initial product launched by Mycelium was the Perpetual Pool. Its core mechanism is the use of two pools (Long Pool and Short Pool) and the rebalancing rate to realize the "never-burst" perpetual contract trading.

In the Perpetual Pool, opening position means minting assets, where the user can mint 1L-ETH/USD (Long) or 1S-ETH/USD (Short) in either the long or short pool by collateral $USDC. On the contrary, closing position means burning assets. The difference between the asset price at the time of minting and burning is equal to the user's loss or gain. The ratio of assets in the long pool to the short pool reflects the user's choice of future price direction movements. For example, if there are more assets in the long pool, it means that more people are long and more assets are minted in the long pool, and vice versa. The rebalancing rate, on the other hand, is similar to the funding rate in Perpetual Protocol's vAMM mechanism. It is used to balance the ratio between the two pools (bringing the long-short ratio back to 1:1). In general, the Perpetual Pool is similar to Perpetual Protocol's vAMM mechanism, with a certain price discovery function and a rebalancing rate similar to the funding rate to balance the long-short ratio. The biggest difference is that the Perpetual Pool has real liquidity.

After changing its name to Mycelium, Mycelium launched a new product in August 2022, Perpetual Swaps, which has a similar mechanism to GMX. It introduces an MLP liquidity pool (like GMX's GLP pool) as a counterparty to traders and provides liquidity to trades.

In terms of trading fees, Mycelium charges 9 bps to open and close a position, and, similar to GMX, traders pay a Borrow fee of 0.5 bps per hour to the MLP pool. 70% of the trading fee is distributed to the MLP liquidity provider and 25% to Mycelium Treasury.

$MYC is the utility and governance token of the Mycelium protocol. In addition to governance voting, holders of $MYC can stake their tokens to receive stake rewards.

Deri Protocol

Deri Protocol is a cross-chain decentralized derivatives trading protocol that is deployed on Ethereum (currently inactive), BNB Chain, Arbitrum, Polygon, and HECO Chain (currently inactive). It's now updated to v3. The platform now offers perpetual futures, perpetual options, and Power Perpetual, which allows users to trade an index of asset prices and hedge against impermanent losses. The most important feature of the agreement is the introduction of DPMM (Deri Proactive Market Making) mechanism, where user positions are tokenized into NFT and can be highly integrated with other DeFi projects, which the platform calls "DeFi Lego".

With the DPMM mechanism, when the net position is 0 (the equilibrium state; long positions equal short position), the mark price equals the index price fed by the oracle. Whenever there is a trade, it pushes the mark price toward the specific trading direction (i.e. a buying trade pushes the price up while a selling pushes it down). Thus, a spread between the mark price and the spot price is created (i.e., mark - spot), and the funding rate mechanism switches to per-second billing, the same as most centralized derivatives exchanges such as BitMEX. Deri's DPMM mechanism unifies the trading logic for both perpetual futures and perpetual options, and allows for any funding-fee-based derivatives to be handled by a single liquidity pool.

v3 also introduces an external liquidity pool through Vault. The protocol deploys a vault for each user to manage deposited capital (LP liquidity or trader margin). The vault will keep a portion of the liquidity reserve for settlement and fees, and the remaining user asset will be sent to an external liquidity pool to earn additional LP rewards. Deri is currently hosting the vault externally on Venus on the BNB chain.

$DERI is a native pass to the Deri Protocol and can be used for platform governance, staking, and transaction settlement. In addition, Deri has defined a "Privilege" feature for $DERI that allows for more favorable trading conditions by staking above-average passes. Further details of this feature have not yet been disclosed.

OPX Finance

OPX Finance (OPX) is a decentralized spot and perpetual exchange deployed on Optimism. It is a fork of GMX. It now supports swap and limited orders for spot trading, 30x leverage long & short for perpetual futures trading. The platform also plans to introduce cross-chain trading and synthetic asset trading in Q1 2023. Besides, OPX offers O-Prediction, an entertainment product that offers rewards through price prediction. The platform was founded by DarkCrypto Foundation, which has extensive experience in project development along with a lot of public controversies.

In terms of fee distribution, 60% to 70% will go to liquidity provider rewards and the rest will be allocated to governance rewards, token buyback and burn, platform development, and the DarkCrypto Foundation.

$OPX is the native governance token of the OPX platform, as well as a deflated token. The max supply depends on the total Fund raised in the Presales.

SynFutures

SynFutures is currently the largest decentralized synthetic asset derivatives trading protocol on Polygon. SynFutures' founding team members, most of whom come from traditional financial institutions and other blockchain companies, such as Bitmain, Matrixport, Credit Suisse, and Nomura Securities, have extensive experience in derivatives management.

SynFutures v1 is deployed on the Polygon, BSC, and Arbitrum networks. It mainly supports crypto futures trading. Users can freely trade all types of assets on the platform, including native, cross-chain, and any other assets with price feed by oracle (eg. Gold).

SynFutures v1 uses Synthetic AMM (sAMM: Synthetic Automated Market Maker) as its core trading mechanism. In a traditional AMM, the liquidity provider needs to offer both assets of a trading pair to balance the asset ratio. Synthetic AMM, on the other hand, allows the liquidity provider to offer only a single asset, with the other asset can automatically be synthesized by the smart contract.

For example, by default 1 $USDC = $1. If the current value of each ounce of gold is 1800 $USDC, the user can directly provide 3600 $USDC, half of which is kept as $USDC, and the other half of 1800 $USDC will be used to synthesize 1 ounce of gold (automatically created by the smart contract).

To further enhance the v1 version and optimize the user experience, SynFutures plans to launch v2. Compared to v1, v2 adds perpetual futures, DAO futures, and NFT futures to enrich the product range. Meanwhile, v2 improves the sAMM model and introduces new liquidity-providing methods such as order book market making to optimize the liquidity provider experience. Currently, SynFutures v2 is in the closed alpha testing stage and only supports the Polygon network. The official launch will go publicly live after the testing ends.

SynFutures is not issuing its token yet. Information related to its token is not disclosed yet.

Firefly

Firefly is a decentralized derivatives trading protocol based on the order book mechanism. Firefly is based on the Polkadot ecosystem. It is the first derivatives exchange of the Polkadot ecosystem. Firefly will be deployed on the Moonbeam network, adopting the Layer2 solution Rollup to increase the throughput of trading.

Firefly is in the guarded launch stage right now, opening to a subset of the community. According to the team's disclosure, the Firefly exchange is scheduled to go live to the public on Moonbeam in December 2022.

The Firefly team has not yet disclosed details about Firefly's product and trading mechanics. What is known is that Firefly will use the Chainlink oracle to feed prices during liquidation, collateralization, and calculation of funding rates. For the product, Firefly will offer both Isolated Margin Leverage and Cross Margin Leverage for trades. In addition, after the official launch of its core product, Firefly plans to establish its DAO to drive the development of the project's decentralized governance.

$FFLY will be issued as Firefly's native governance token. $FFLY will be used for governance voting, staking, and trading rewards.

Kwenta

Kwenta is a decentralized synthetic derivatives exchange developed by the Synthetix team and deployed on the Optimism Layer2 network. It currently supports spot swaps and perpetual futures trading.

Kwenta's primary product is perpetual futures, which supports perpetual contract trading with up to 25x leverage. The order types supported by Kwenta include market orders, limit orders and stop market orders.

Unlike traditional exchanges that use mechanisms such as order books and AMMs, Kwenta is based on the Synthetix protocol. Liquidity on Kwenta is provided by Synthetix's debt pool. This allows traders on Kwenta can access the liquidity they need on trades at any price point. Moreover, the prices of Synthetix's synthetic assets are fed by the Chainlink oracle. Tradings on Kwenta are executed with 0 slippages.

Due to the complexity of the Synthetix protocol, we will not dig deeper into its core mechanics here. If you are interested, you can click here to learn more about Synthetix.

Regarding the fee structure of Kwenta, since Kwenta's liquidity is derived from Synthetix's debt pool, an exchange fee will be collected and sent to the fee pool and allocated to Synthetix ($SNX) stakers. In addition, under volatile market conditions, Kwenta will charge a dynamic exchange fee to neutralize front-running opportunities and protect stakers.

$KWENTA is Kwenta's utility and governance token. It is used to incentivize coordination and growth within the Kwenta DAO. The main functions of $KWENTA include staking and governance.

Summary

- Crypto derivatives trading first started in 2011, but a new chapter was officially started after BitMEX invented the perpetual contract. The market was booming in 2019 and reached the peak of trading volume in 2021 as the bull market came.

- The top three derivatives exchanges in 2019 are BitMEX, OKX and Huobi; in 2020 they are Huobi, Binance and OKX; in 2021 they are Binance, Huobi and Bybit; in 2022 they are Binance, OKX and Bybit (there was originally a place for FTX).

- Decentralized derivatives exchanges have obvious advantages over traditional centralized derivatives exchanges in terms of asset transparency, user asset control, censorship resistance and privacy, and on-chain composability.

- Insufficient liquidity, high transaction costs, low product usability, and poor function richness are the main problems faced by decentralized exchanges.

- Over the past 10-month period, the total trading volume of decentralized derivatives exchanges reached $478B. While this figure is roughly equivalent to two weeks of Binance derivatives trading volume in the current market environment, this figure was almost zero at the beginning of last year.

- dYdX is the leading decentralized exchange before Q3 in 2022, but there are signs of being surpassed by GMX in terms of trading volume after Q3; dYdX has sometimes been surpassed by GMX in terms of platform revenue, and GMX has already ranked first in terms of TVL.

- According to the current market development trend, the market size of decentralized exchanges is expected to increase by more than 10 times within a year.

- From the perspective of decentralization, dYdX is the lowest compared to GMX, Perpetual, and Drift. At the same time, the vAMM mechanisms of Perpetual and Drift are less adaptable to the current market than the other two protocols.

- From the perspective of fee structure, compared with the others, GMX and Perpetual's sources of fees are more abundant, which helps the protocol to develop better; and the fee structures are also better, which is conducive to user incentives. In contrast, dYdX keeps all platform revenue for itself.

- dYdX, GMX, and Perpetual all have sound tokenomics, encouraging users to participate in protocol governance and token staking. However, in terms of effect, dYdX and Perpetual will be slightly inferior to GMX, mainly because the actual income received by users after participation is lower.

- The next development direction of the decentralized derivatives exchanges mainly includes providing more trading mechanisms and products, striving for market share, launching new chains, and realizing fully decentralization (especially dYdX), etc.

- The core mechanism of most new entrants still applies the mechanism established by the current leading project, namely the order book, multi-asset liquidity pool and vAMM mechanism.

DeFi

Derivatives

Exchanges

In This Article

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open