$FRAX and $UST – Same destination from different starts?

Whilst $UST is under the spotlight, it is probably a good time to review how $FRAX works, the first fractional-algorithmic stablecoin.

Whilst $UST is under the spotlight, it is probably a good time to review how $FRAX works, the first fractional-algorithmic stablecoin.

$UST/$LUNA has attracted everyone's attention in the field of algorithmic stablecoins. The establishment of LUNA Foundation Guard and the $BTC reserve for UST have pushed $LUNA to ATH. The $BTC reserve for $UST is kind of making the pure algorithmic stablecoin with the element of collateral.

Whilst $UST is under the spotlight, it is probably a good time to review how $FRAX works, the first fractional-algorithmic stablecoin, which is partially backed by collateral and partially stabilized algorithmically. In a sense, $UST & $FRAX is actually going toward the same destination from different starts.

The algorithmic mechanism

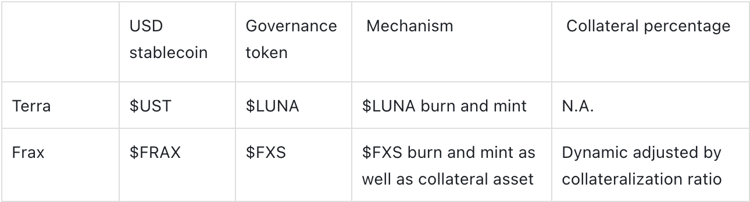

Both Frax protocol and Terra implement a duel-token system. For Frax, there is a USD stablecoin, $FRAX, and a governance token, $FXS. In comparison, Terra has stablecoin $UST, and a governance token, $LUNA.

For Terra's $UST, users burned $LUNA to mint $UST, and redeem $LUNA back by burning $UST, a pure algorithmic mechanism to maintain the dollar peg. While for Frax, $FRAX is backed by both collateral and an algorithm (burning and redeeming of $FXS). $FRAX is minted when collateral and $FXS are deposited into the Frax protocol contract. The collateralization ratio determines the amount of collateral needed to be deposited to mint 1 $FRAX.

Source: Frax, Terra

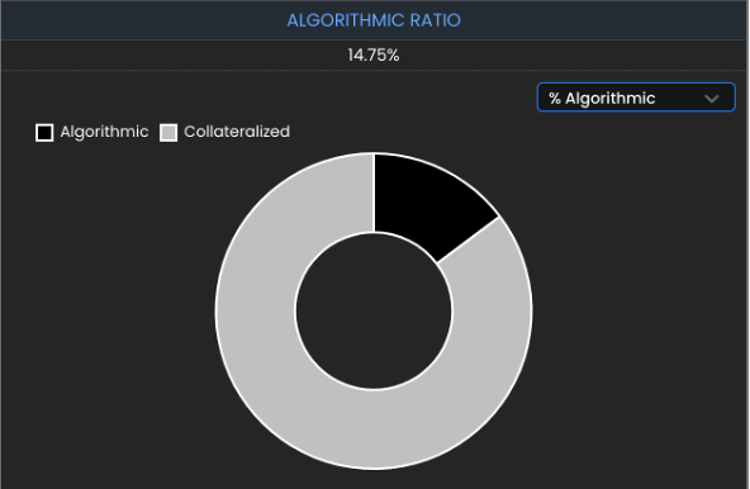

At launch, $FRAX was 100% collateralized, and the only collateral that was accepted is $USDC, meaning $FRAX requires placing an equal amount of $USDC into the minting contract. The collateralization ratio is 100%. This means $FRAX is actually a centralized stablecoin.

Source: https://app.frax.finance/

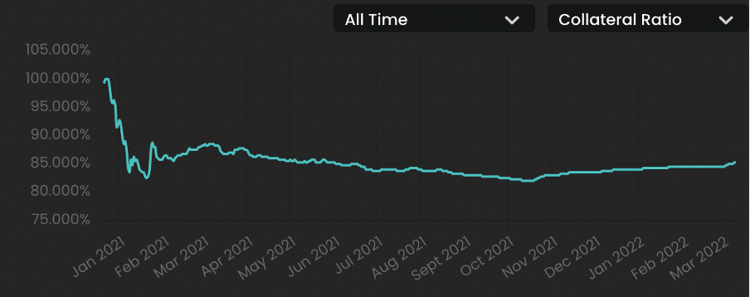

The collateral ratio is dynamically adjusted based on the price of $FRAX. If the demand of $FRAX increases, pushing the price above $1, then the collateral ratio will decrease making $FRAX less backed by centralized stablecoin collateral. If the price of $FRAX is below $1, then the collateral ratio will increase, more $UDSC will be required to back the $FRAX. For example, at an 85% collateral ratio, every $FRAX is backed by $0.85 $USDC and $0.15 of $FXS.

Source: https://app.frax.finance

As the market demand expands for $FRAX stablecoin, the collateral ratio will decrease, making the stablecoin more decentralized and algorithmic. The stablecoin will be less backed by $USDC, and rely more on the burn and mint mechanism of $FXS. The current collateral ratio is around 85%. If the market demand continues to increase, this will essentially make $FRAX, in theory, become a pure algorithmic, the same as $UST.

$UST backed by $BTC

In February, LUNA Foundation Guard (LFG) announce a 1 billion dollar Bitcoin reserve for Terra by private tokens sales of $LUNA. Although the reserve is not explicitly labeled as collateral, LFG stated that the reserve is used to maintain the stability of the $UST peg. When there is a contraction of $UST demand, instead of being required to mint $LUNA to arbitrage UST's price, now there is the option to swap $UST to $BTC instead. This has greatly reduced the death spiral risk that is inherently in algorithmic stablecoin.

With a market cap of around $14.5 billion as of Mar 11, the $1 billion bitcoin reserve, as well as an additional $450 million potential bitcoin reserve announced on Mar 5, could be viewed as a 10% collateral ratio. In a sense, this makes $UST partially backed by collateral and partially algorithmic stablecoin.

Capital inefficiency problem and the death spiral risk

Collateralized stablecoins face the capital inefficiency problem, over collateralized stablecoin like $DAI, need 150% of collateral to mint $1 $DAI, this greatly limits the overall possible amount of $DAI can be minted, this kind of stablecoin cannot scale. Algorithmic stablecoin does not need collateral but faces the death spiral risk.

Source: Twitter, @ZeMariaMacedo

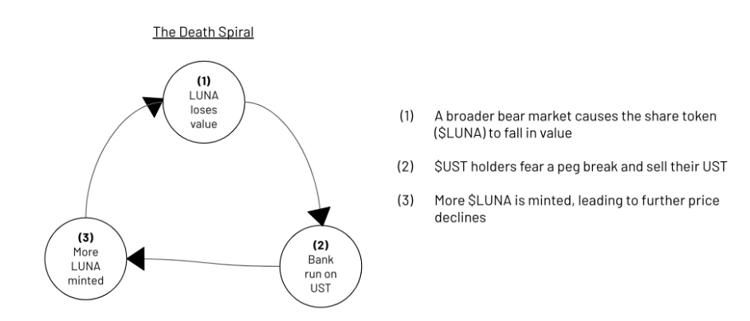

Take the example of $UST, at the time of demand contraction, people sell $UST back to the protocol and in return get $LUNA, the $LUNA is used to absorb the volatility of the stablecoin, thus higher the value of $LUNA, the robust of this system. However, if there is a broader bear market and $LUNA falls in value significantly, and people continue to burn $UST, more $LUNA is minted as a result. This will form a vicious cycle, leading to a collapse of faith in the entire system. There is no perfect solution to this risk. The only way to mitigate it is through increasing use cases of the algorithmic stablecoin, resulting in increasing demand, hence pushing up the $LUNA price, making it stronger to absorb the volatility in the bad times. Terra developed a series of in-house protocols for this purpose, the most well-known example is Anchor protocol.

A partially algorithmic and partially collateralized stablecoin is both more robust and capital-efficient compared to a pure algorithmic or pure collateralized stablecoin.

The recent positive market reaction for the Bitcoin reserve shall prove that the market thinks this is the right direction. And it is very interesting to note the founder of Frax tweeted below last April.

Source: Twitter, @samkazemian

$FRAX has long been in this mechanism, why doesn't it experience the same growth as $UST. The issue probably lies in the range of use cases. For $UST, Terra ecosystem has one and only one purpose, to boost use cases for $UST. Every protocol on the Terra chain has been on this mission to increase the $UST demand.

Frax market strategy

Terra is a layer one blockchain, it can self-build a whole ecosystem to boost $UST demand. Frax cannot follow the same strategy since it is a DeFi protocol built on Ehtereum.

Rather than put all the effort on expand $FRAX demand, Frax protocol seems to follow a different path – Treasury management.

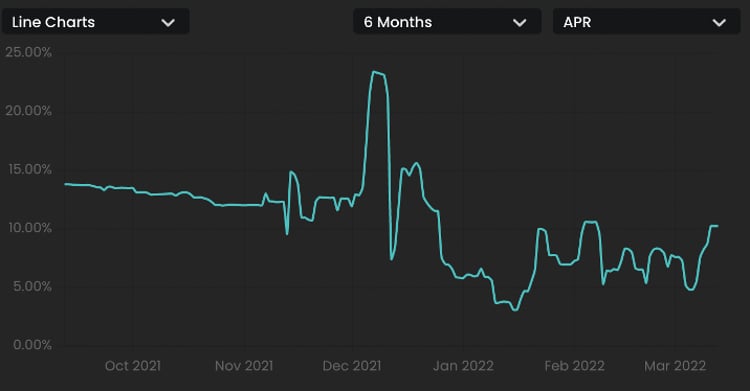

Frax launched algorithmic market operations modules or AMO. The mechanism of AMO is rather complex, and out of the topic of this article. One of the purposes of AMO is to put idle treasury assets ($USDC & $FRAX) into different DeFi protocols to earn yield. This includes AAVE, Compound, Yearn, as well as liquidity pool in Curve and Uniswap. The AMO has been extremely profitable, the average daily income was around $500K in January, with the general lower yield across DeFi recently, the average daily income is now around $240K. The governance token $FXS captures all income, which makes it a current yield of 10%.

FXS APR. Source: https://app.frax.finance/

As $FRAX is still primarily collateralized by centralized stablecoins, it didn't urgent to drive broader application scenarios as $UST, and the current high collateralization rates ensure a very secure stablecoin pegging mechanism. Frax is focused on creating greater value for $FXS, and a more robust $FXS can support lower collateral rates in the future, making the $FRAX algorithm more robust.

Stablecoins

DeFi

Terra

In This Article

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open