How does the delivery of the US$2.4 billion option affect the market?

Although the impetus of the crypto options market on crypto prices may be less than expected, it is changing the market with a completely different mechanism from the traditional market.

Although the impetus of the crypto options market on crypto prices may be less than expected, it is changing the market with a completely different mechanism from the traditional market.

"Unusual Friday"

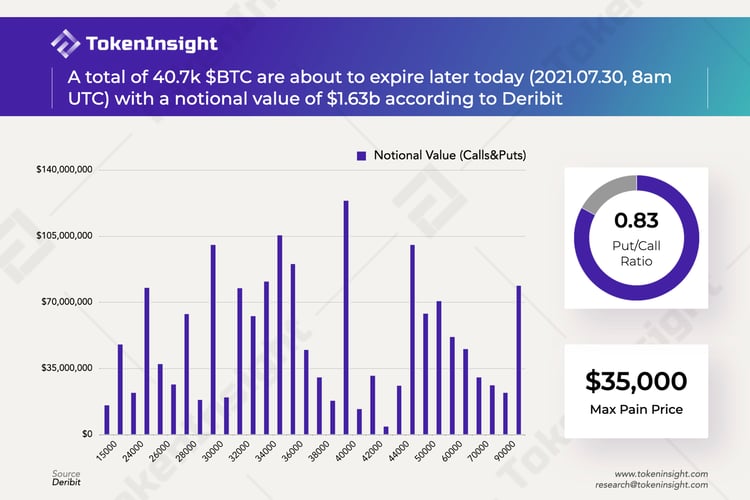

Friday is the weekly derivatives delivery day. Compared with the usual Friday, July 30th, this Friday is not ordinary.

Under normal circumstances, the delivery days with larger trading volumes tend to be concentrated at the end of the quarter and the end of the half-year. The reason is that options are often targeted for a longer period of time, usually monthly, quarterly, or even annual allocation. However, this time is different from the past, in terms of changes in the amount of open interest, there has been a rapid increase in the number of bitcoin options contracts this week: from last Friday to this Thursday, the open interest in Deribit has increased by 25,810 contracts, the largest weekly increase since mid-April. The notional value of options delivered on July 30 also exceeded US$2.4 billion.

The rapid rise of open interest usually occurs before the quarterly delivery, but in normal times, it may be a signal of the activities of "whales"(large digital asset market players) and investors who have obtained information in advance. Other signals are also available at this time. It may follow.

The rapid rise of open interest usually occurs before the quarterly delivery, but in normal times, it may be a signal of the activities of "whales"(large digital asset market players) and investors who have obtained information in advance. Other signals are also available at this time. It may follow.

Comparing annual data, it can be found a similar situation occurred in September last year. And afterwards, Bitcoin and even the digital asset market ushered in a bull market that lasted until May. The recovery of options and even other derivatives trading enthusiasm seems to herald the improvement of the market in the future.

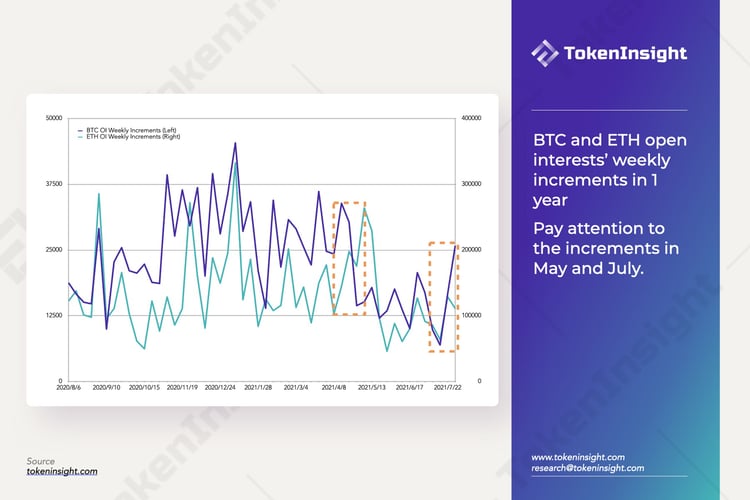

This seems to be a good sign, but not that kind of good. In the past, under the guidance of the macro market, the changes in the open interest of options contracts were often related to the market macro conditions. Therefore, it can be found that the increase in the open interest of options contracts of mainstream digital assets such as Bitcoin and Ethereum showed the same trend of "increase and decrease". However, this time the contract increment is concentrated on Bitcoin, and the Ethereum contract increment has even declined compared to last week.

Is it "hot money" or market confidence back?

One possible explanation is that large-scale "hot money" is focusing on short-term layout, and the "gamma squeeze" caused by short-term layout (for gamma squeeze, please refer to the previous blog "Warning: Gamma Squeeze" related explanation ) Large purchases in the spot market have caused the price to rise sharply in a short period of time. This kind of rise is often concentrated on a single asset, lacks support, and is easy to burst in a short period of time. What happened on Ethereum in May is a similar thing. While the increase in Bitcoin contracts fell, the increase in Ethereum contracts rose sharply. At the same time, the price of Ethereum rose to a high of more than $4,000 in a short period of time, and then it was cut in half.

The incremental rise of this option contract takes the same form and is similar to it. Judging from the data this week, due to the lack of long-term expectations, it is likely that short-term planners will sell after the option pushes the price up to make a profit. However, judging from the spot market, options are not the only reason for the price increase.

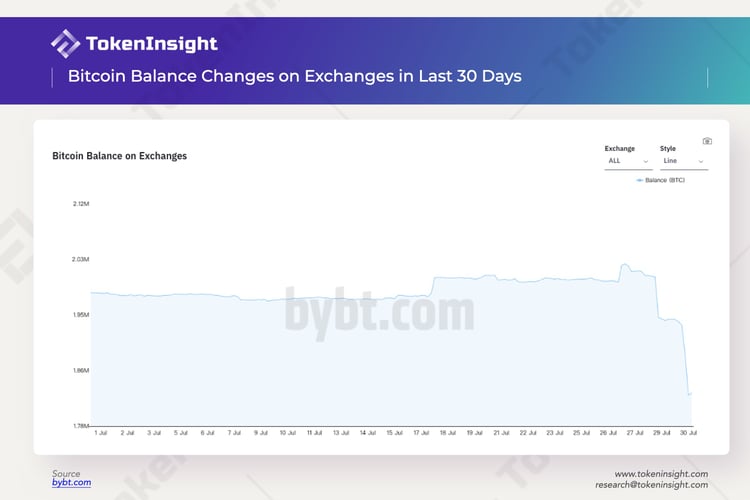

The rapid increase in Bitcoin was accompanied by a sharp drop in the exchange wallet balance. According to Bybt, the outflow of bitcoins from major exchanges reached a staggering 175,458.75 in the past week, and most of them were large-scale outflows. The reason is temporarily unknown. The weekly spot purchases caused by the gamma squeeze will not exceed 20,000 Bitcoins, and the outflow of more than 170,000 Bitcoin does not seem to be the effect of the options market.

This leads to an interesting inference: the market's turnaround is guided by the rise of volatility, and the rising volatility is driven by volatility derivatives such as options. After the volatility rises, the market activity increases, triggering spot buying, and finally, the market changes from "virtual bull" to "real bull". This is very different from the traditional market: the volatility in the traditional market is often dominated by the macro level, and the long-term push effect of derivatives on asset prices is not significant. But for the digital asset market, derivatives drive not only prices but also expectations and confidence. The influence of expectations and confidence in the digital asset market means much more than that of traditional markets.

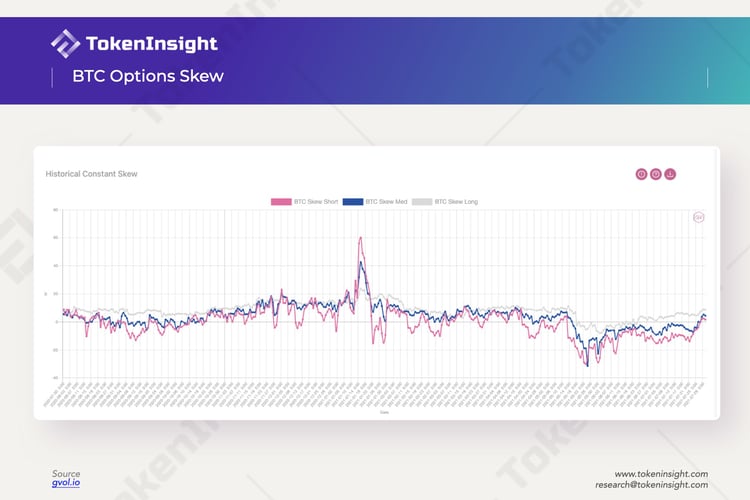

Skewness is one of the important indicators reflecting market confidence. From the perspective of skewness, both the short-term and medium-term skewness have turned positive, and market confidence has recovered significantly. A large number of Bitcoins transferred from exchanges seems to indicate strong spot buying, which means that price increases triggered by fluctuations in the derivatives market ultimately boost market confidence and are beneficial to short-term price trends. But no one knows how long market confidence can last.

Bitcoin

Ethereum

Options

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open