How Stable are USDT, USDC, and BUSD?

First of all, I have to admit that I was a little panicked on May 12th, swapping my $USDT for $USDC, which of course cost me dearly in gas fees. But it also peaked my interest in taking a closer look at the top three fiat-backed, centralized USD stablecoins. Whichever way you look at it, they still provide a safe harbor in a turbulent market.

Today I will look at three aspects of these centralized stablecoins: reserve assets, adoption, and compliance risk.

First of all, I have to admit that I was a little panicked on May 12th, swapping my $USDT for $USDC, which of course cost me dearly in gas fees. But it also peaked my interest in taking a closer look at the top three fiat-backed, centralized USD stablecoins. Whichever way you look at it, they still provide a safe harbor in a turbulent market.

Today I will look at three aspects of these centralized stablecoins: reserve assets, adoption, and compliance risk.

Reserve Assets

What lies behind a centralized stablecoin determines whether there will be a risk of a bank run. If a stablecoin is 100% backed by USD deposits, we can say confidently that there will be no such risk.

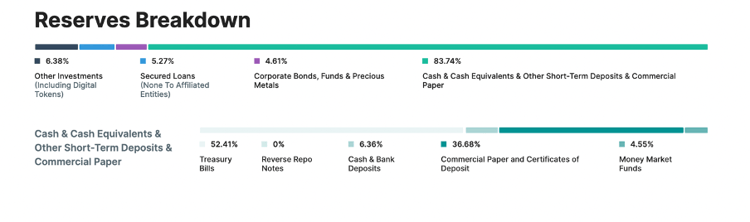

USDT

As we all know, $USDT is not fully backed by dollar deposits. The latest attestation report dated Dec 31, 2021 shows around 53% of $USDT is currently backed by cash and cash equivalents, meaning these assets can immediately be converted into dollars. The remaining portion is backed by a combination of commercial paper & Certificate of Deposit, corporate bonds, secured loans, and other investments.

Source: https://tether.to/en/transparency/#reports

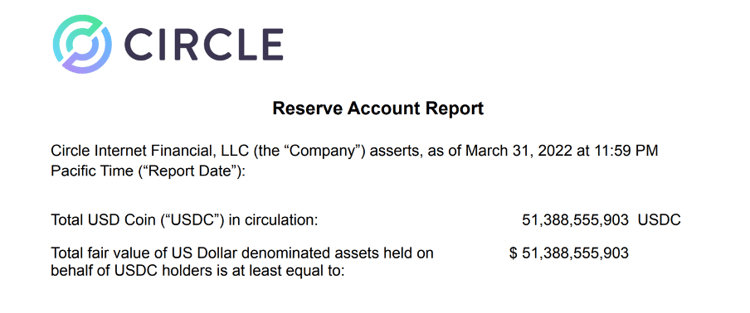

USDC

Source: https://www.centre.io/hubfs/PDF/2022%20Circle%20Examination%20Report%20March%202022.pdf?hsLang=en

$USDC is therefore solid as a rock, because it is 100% backed by US dollar assets. These assets are limited to cash and short-dated US government obligations only, and are held at US-regulated financial institutions.

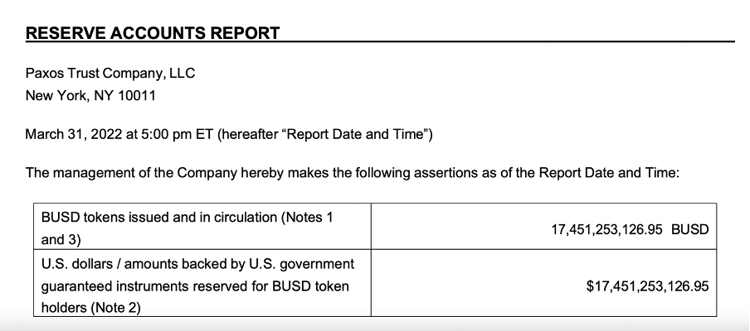

BUSD

Source: https://paxos.com/wp-content/uploads/2022/04/Executed-_-BUSD-Examination-Report-March-2022.pdf

Binance partnered with the Paxos Trust Company to issue $BUSD. Paxos Trust is the USD custodian and issuer of $BUSD. $BUSD is fully backed by the US dollar and the US government treasury.

Summary

In conclusion, if you want to be 100% safe, go with $USDC or $BUSD. Even if there are price fluctuations around a dollar, you will always be able to redeem that dollar. And while $USDT is not fully secured by cash assets, it is extremely difficult to de-peg $USDT. Plus, $USDT's more than 53% cash reserve is more than sufficient.

Surely, if more than 53% of $USDT needs to be redeemed all at once, and Tether can't sell other investments at a fair market price, it will incur a bank run. But this is extremely unlikely due to the fact that users need to have an account with Tether for the redemption process and the process usually takes 1 to 2 days.

Whales also know there are sufficient reserves for Tether; if the $USDT falls below a $1, they are more than happy to buy $USDT from the market at a price less than $1, and redeem it from Tether. The buying pressure then pushes the price back up to $1.

Tether is also well aware of the market's concerns about its reserves, and is actively de-risking its reserves toward more cash-based backing.

Source: https://www.reuters.com/markets/currencies/tether-has-reduced-its-exposure-commercial-paper-cto-says-2022-05-12/

Adoption

I will focus on $USDT when examining the adoption of stablecoin, since this is another aspect that contributes to its stability.

Medium of exchange, and unit of account - these are the real use cases for a currency. With an outstanding market cap of over $80 billion, $USDT is the single largest stablecoin in the market. It is widely used in the exchange of on-chain assets, as well as off-chain adoption. Although there are no stats to prove it, it's well known that $USDT is used for daily transactions outside of the crypto market too, especially in East Asia, Southeast Asia, and the Middle East.

Liquidity Distribution

Of the $80 billion $USDT, around $39 billion is on Ethereum, and another $39 billion is on Tron.

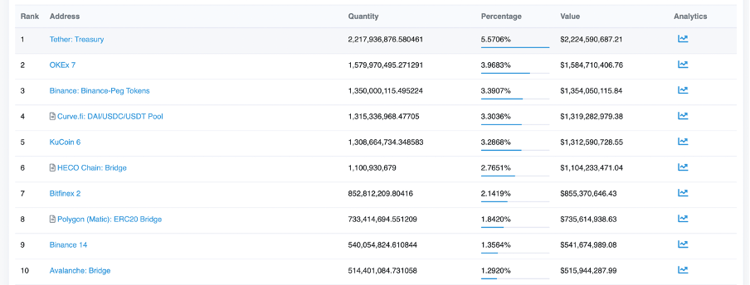

Wallet holding in Ethereum:

Source: https://etherscan.io/token/0xdac17f958d2ee523a2206206994597c13d831ec7#balances

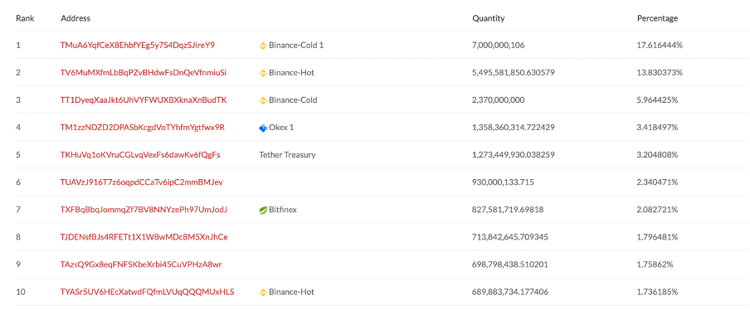

Wallet holding in Tron:

Source: https://tronscan.org/#/token20/TR7NHqjeKQxGTCi8q8ZY4pL8otSzgjLj6t/holders

If we look at the top holders of $USDT on Ethereum and Tron, it shows most of the $USDT is actually held by centralized exchanges. The largest on-chain liquidity pool in Curve holds $1.4 billion, which is merely 1.75% of the total supply.

If there is market-wide FUD, the centralized exchange could suspend trading first. I know this is not good practice, but this kind of circuit breaker allows the market to resume normal tradings.

Regulatory Compliance

Early May's Terra drama has inevitably attracted the attention of US regulators, and US Treasury Secretary Janet Yellen has pushed for stablecoin regulation by the end of this year, meaning we can expect to see much faster stablecoin regulation from this point on. It's worth adding that regardless, all three issuers have already made clear efforts to be more compliant.

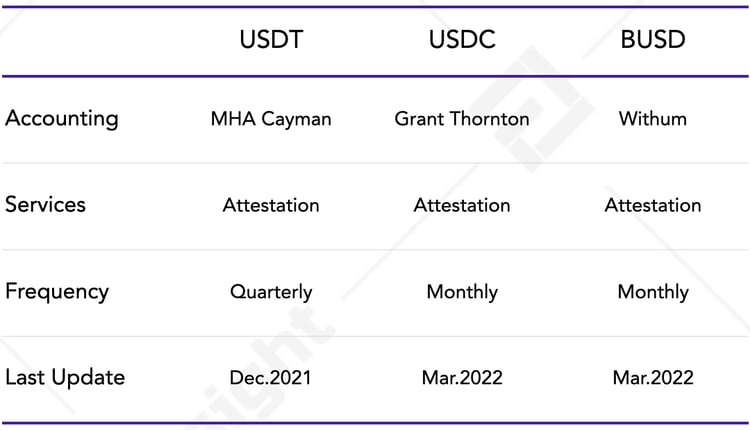

Independent Accountant Report

All three stablecoin issuers hire independent accounting firms to issue an attestation report on their reserves. While $USDC & $BUSD provide monthly attestation reports, $USDT only provides a quarterly one. Note that the latest attestation report for $USDT is dated Dec 31st, 2021, while the other two have already provided attestation reports to Mar 31st, 2022.

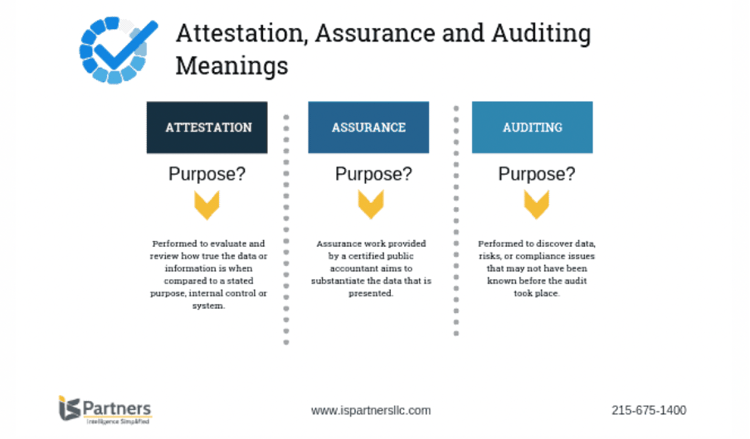

It's also important to understand the concept of attestation, as it is not the same as auditing.

Source: https://www.ispartnersllc.com/blog/defining-attestation-assurance-auditing/

An audit is the evaluation and investigation of an organization, during which information and data are gathered that can help spot a weakness in its operations. Instead, an attestation is carried out to check the validity of data and internal controls. The key difference between them is that audits are performed to discover data, risk, or compliance issues that may not have been known before the audit took place, while an attestation is carried out to evaluate and review how true the data or information provided is.

An attestation is therefore sufficient to show that all three issuers have the reserve assets they have declared. But an attestation does not ensure they have appropriate internal control procedures in place to maintain those reserves.

Excerpt from $USDC attestation report

Licensing

$USDC - The issuer Circle is a licensed money transmitter in 46 US states, plus Washington, D.C., and Puerto Rico.

$BUSD - The issuer Paxos is regulated by NYDFS – the New York State Department of Finance – and has in-principle approval for a Major Payments Institution License from the Monetary Authority of Singapore.

$USDT - The issuer Tether is registered with the Financial Crimes Enforcement Network.

The different licensing methods imply a different level of supervision. While I don't have a regulatory background, I tried to assemble information regarding the level of regulatory recognition. The only one of the three stablecoins that is regulated rather than licensed is $BUSD, which means a higher level of regulatory oversight. More specifically, it has to meet specific NYDFS capital reserve, consumer protection, compliance, and anti-money laundering requirements, as well as undergo regular examination.

Closing Thoughts

If we consider the metrics discussed above, it looks like $BUSD is the safest choice for stablecoin. It not only has full reserve assets but also obtains the highest level of regulatory supervision. While I don't think $USDT has any real risk of de-pegging, it is the weakest among the three in terms of reserve assets and regulatory supervision. I also don't feel good about the fact that it only provides a quarterly attestation report, while the other two provide a monthly one.

Being the largest stablecoin in crypto, $USDT serves as a trading pair for almost all other crypto-assets and as the quote currency for almost all futures contracts. It could therefore also be the single point of failure for the whole crypto industry.

After the incident on May 12th, the supply of $USDT is rapidly decreasing, and both $USDC and $BUSD have seen demand increase. The popularity of $USDT is more due to its history in the space rather than because it is a better product. It is therefore nice to see a more balanced market supply distribution between several major fiat-backed stablecoins – not least because it could bring about a more robust system.

Stablecoins

USDT

DeFi

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open