Innovations of On-Chain Perpetual Protocols

As the impending contagion effects from FTX unfold, there has been an increased emphasis on decentralization and transparency.

As the impending contagion effects from FTX unfold, there has been an increased emphasis on decentralization and transparency.

As the impending contagion effects from FTX unfold, there has been an increased emphasis on decentralization and transparency. The migration of trading activity from CeFi to DeFi is not a matter of “if” but a matter of “when”.

Perpetual protocols like GMX have gained significant traction in the past couple of months. The unique design of GMX has flourished into an ecosystem on its own. This research piece has been split into 2 articles.

Part 1 can be found here: Bytetrade Lab Medium

In Part 2, greater focus will be placed on GMX’s Ecosystem and some interesting protocols that are built on top of GMX.

As mentioned in Part 1, GMX LPs are exposed to 1) the open interest (OI) on GMX and 2) the price volatility of underlying assets.

Some protocols have set out to solve the challenge of underlying asset volatility.

TL;DR

- Given the "real & sustainable" yield of GMX, more protocols are building on top of GMX to take advantage of $GLP yield.

- Several protocols are building delta-neutral strategies on top of GMX:

- Rage Trade uses other protocols like Balancer, Uniswap & Aave to provide pre-packaged delta-neutral strategies for $GLP holders and provide yield on stablecoins.

- Umami Finance attempted to use TracerDAO's perpetual pools to provide hedging strategies for $GLP holders. Meanwhile, the product has since been terminated indefinitely.

Rage Trade

After having a short discussion with Rage Trade’s founder @crypto_noodles, the protocol aims to do 2 things: 1) provide pre-packaged delta neutral strategies for GMX LPs and 2) provide enhanced yield for stablecoin depositors.

Rage Trade’s vision is to be Arbitrum’s largest stablecoin farm by utilizing real & sustainble $GLP yield.

To accomplish this, Rage Trade plans to provide 2 products. These products are namely the Junior Tranche (Risk-On Vault) and Senior Tranche (Risk-Off Vault).

The simple workflow below depicts how Rage Trade’s vaults work.

Referencing the mindmap above, orange colour-coded figures/text present information regarding the Junior Tranches, and blue colour-coded figures/text present information regarding the Senior Tranche.

Starting with the Junior Tranche:

- Users that participate in the Junior Tranche deposit $GLP into the

Risk-On Vault on Rage Trade. The subsequent actions are completely automated and routed by Rage’s vault contracts. - Based on the weightages of $ETH and $BTC in the $GLP pool, Rage Trade takes a corresponding amount of $ETH and $BTC flash loan on Balancer.

- The borrowed $ETH and $BTC is then sold on Uniswap for $USDC. Creating a synthetic short position.

- In addition to proceeds from selling $ETH and $BTC on Uniswap, a $USDC top-up from Senior Tranche will be deposited on Aave as collateral to borrow $ETH and $BTC.

- The borrowed $ETH and $BTC from Aave is then used to repay the flash loan from Balancer.

- This entire process allows LPs on GMX to enjoy $GLP yield with a delta-neutral position. Effectively reducing underlying asset volatility by a great extent.

Moving on to the Senior Tranche:

- Users that participate in the Senior Tranche deposit $USDC into the Risk-Off Vault on Rage Trade.

- $USDC is then lent to the Junior Tranche to maintain a health factor of 1.5x on Aave.

- Senior Tranche participants then earn yield via 2 means. Firstly, the $USDC deposited on Aave generated additional yield.

- Additionally, a portion of $GLP’s yield is allocated to the Senior Tranche based on the utilization of $USDC in the Senior Tranche. The calculation of the utilization rate is shown in the mindmap.

The performance of Rage Trade’s backtest results using 1 year of GMX’s data is shown below.

Assuming an $ETH yield of ~20% the “Risk-On” Vault/Junior Tranche yielded a net return of ~24.8% after accounting for $GLP yield sharing with the Senior Tranche. Do take note that the “Risk-On” Vault automatically compounds the $ETH rewards on a regular basis.

Conversely, if $GLP holders were to purely HODL, they would have netted a -3% return given the fall in asset prices within the $GLP pool.

Assuming an $ETH yield of ~20% the “Risk-Off’ Vault/Senior Tranche yielded a net return of ~8.27%. The yield can be split into 2: 1) Lending Interest on Aave yielded ~1.05% and 2) $ETH yield from $GLP yielded ~7.22%.

The “yield funnel” for both Tranches are shown in the diagram below.

Key Challenges

Rage Trade has built an amazing product. Meanwhile, the protocol faces 2 main challenges: 1) Balancing Risk and 2) Heavy reliance on $GLP yield.

Balancing the positions within the vaults happen for two reasons:

1) Weight Changes in the $GLP pool or 2) Price changes $ETH and $BTC.

The short positions on Aave are updated every 12 hours. This means that every 12 hours if the prices of the $ETH and $BTC increase, profits from $GLP will be taken to repay the short positions. To improve capital efficiency, Rage Trade maintains a 1.5x health factor on short positions on Aave.

In the scenario where the prices of $ETH and $BTC were to spike within the allocated 12-hour window, there could be a possibility of liquidation on Aave.

In that scenario, the participants in the Senior Tranche would lose whatever they lent to the Junior Tranche. While participants of the Junior Tranche would likely have to reduce their position in $GLP to achieve delta-neutrality again OR completely lose their delta-neutral position.

Naturally, the protocol is heavily reliant on $GLP yield. This is not a systemic risk but users should take note of the potential volatility in yield.

The team was conservative in assuming a 20% constant borrowing rate for $ETH. Regardless, participants should take note that the yield for $ETH fluctuates significantly.

Observing the past 2 months' data, the average borrowing rate for $ETH was 26.5%. Nonetheless, there were 44 instances of $ETH’s yield dipping below 20.0%, with the lowest borrowing rate being ~9.1%.

Umami Finance

At inception, Umami Finance aimed to bring institutional capital into Web 3.0 with the promise of a “sustainable” 20% APR.

Umami’s USDC vault provided liquidity to GMX and passed on $GLP’s yield to depositors while hedging out unwanted market delta.

USDC Vault (Defunct)

In operation, Umami’s USDC Vault generated yield by providing liquidity to GMX and in exchange, the vault receives $GLP yield.

- Users deposit $USDC into the USDC vault and receive a receipt token, an ERC-4626 token, $glpUSDC. Users can leave the vault by swapping $glpUSDC for stables on Uniswap at any point.

- The vault uses an undisclosed proportion of the deposited liquidity to mint $GLP and collect GMX trading fees.

- The rest of the deposited liquidity is used to mint $BTC and $ETH hedging derivatives on TracerDAO (now called Mycelium).

- By purchasing leveraged tokens (3S-BTC/3S-ETH) as a hedge, the vault creates a $ETH and $BTC short position.

- This enables the vault to earn $GLP yield (from trading fees) while hedging out $BTC and $ETH price volatility.

Tracer Hedging Derivates

Umami utilizes Tracer’s Perpetual Pools for hedging out unwanted $GLP price volatility. Tracer’s Perpetual Pools are synthetic derivates that enable users to take leveraged long or short positions on assets. Each pool has a predetermined exposure amount (e.g. 3S BTC or 3L ETH)

These positions are non-liquidatable and fully collateralized.

The Perpetual Pools are governed by a contract that dictates the transfer of value between long and short sides of a collateral pool, based on an underlying price feed:

- There are 2 sides to the pool: long & short. Users deposit $USDC on the long side of the collateral pool to mint a long token and vice versa.

- Users can convert long/short tokens to $USDC by burning either tokens.

- The value of the tokens is determined by the proportion of the collateral held on each side of the pool.

- The amount of collateral held in the short and long pools varies dynamically.

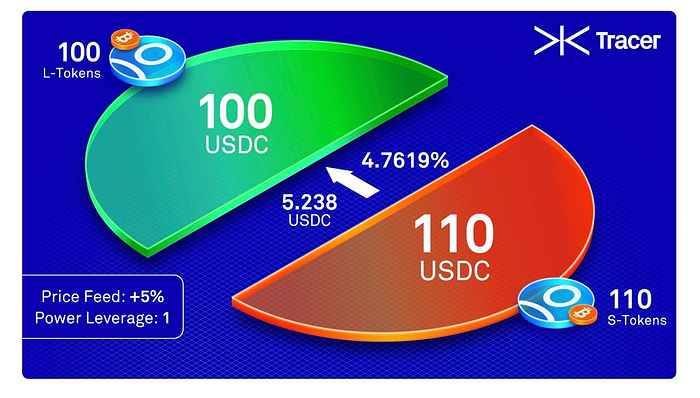

- Every hour, a rebalancing occurs and value is transferred from one side of the pool to another. The amount transferred is determined based on the pool’s collateral ratio and its calculation is illustrated below.

Using a 1x pool as an example, when the underlying asset’s price increases, collateral from the short pool will be transferred to the long pool.

The calculation for the value transfer is a 2-step process:

- Assuming a 5% rise in the underlying price, the value transfer is calculated as:

2. The amount that is transferred from the short pool is then calculated as:

Returns from the TracerDAO Perpetual Pools are non-linear

This function effectively prevents any side from losing 100% of its value. Even though liquidation risk is effectively eliminated, gains are dampened quite substantially. Observing the 2p Long Spot (green dotted line), if the underlying asset appreciates by 100%, a 2x exposure would net 200% gain. Yet, due to the power leverage function, gains are reduced to about 75%.

The “yield funnel” for Umami’s USDC Vault is shown in the diagram below.

Key Challenges

The Underperformance of TracerDAO’s Perpetual Pools

It is important to note that the USDC vault’s hedging model does not result in complete delta neutrality.

Despite the flawed design of TracerDAO’s perpetual pools, Umami likely used it as a hedging tool as they launched an earlier campaign to support liquidity in TracerDAO pools ahead of the USDC vault launch. The actual cost of hedging using the Pools proved to be much higher than anticipated.

Skew on TracerDAO Pools were a significant constraint to vault scalability and performance.

Similar to Rage Trade, the balancing risk is prevalent in Umami’s USDC Vault.

The vault rebalances its Tracer hedges every 9 hours. If $BTC or $ETH is very volatile in a short period of time, this might adversely affect the delta-neutrality.

Vault is now defunct

In late Aug 2022, Umami paused its highly anticipated USDC vault as the claimed 20% APR was unsustainable.

Naturally, when the public received the news of the vault’s underperformance and subsequent pause, majority of vault depositors swapped out of $glpUSDC.

Moving Forward

Both protocols mentioned above have attempted to ease the challenge of underlying asset price volatility for $GLP pool LPs. Umami Finance is stated to give it another attempt while the results of Rage Trade are not yet visible.

The developments within the GMX ecosystem are something to be excited about.

Key Takeaways:

- Two protocols have set out to provide delta-neutrality to $GLP holders. We look forward to Rage Trade's product and applaud Umami's attempt toward delta-neutrality.

- More protocols will eventually leverage on the real & sustainable yield of $GLP.

DeFi

Derivatives

DEX

In This Article

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open