Warning: Gamma Squeeze

Recently, the market has moved frequently, and the prices of mainstream cryptos have risen sharply. The "Gamma Squeeze" caused by options trading may be an important reason for that. Gamma squeeze often brings large fluctuations in prices, but it may also herald the recovery of the market in the future.

Recently, the market has moved frequently, and the prices of mainstream cryptos have risen sharply. The "Gamma Squeeze" caused by options trading may be an important reason for that. Gamma squeeze often brings large fluctuations in prices, but it may also herald the recovery of the market in the future.

For the crypto market, there were a lot of changes in the third and fourth weeks of July that are hard to ignore. After Bitcoin briefly fell below $30,000, stimulated by the good news from bulls, mainstream crypto prices began to slowly rebound, causing market bears to be caught off guard, and the decline in PMI data provided the basis for further increases in asset prices, and market optimism began to rise.

However, the opposite is a sharp decline in market liquidity. The market activity in mid-to-late July dropped to the lowest level in nearly three months. Take Bitcoin as an example, its daily trading volume in mid-July remained below $30 billion for a long time. The market macro background of "low liquidity + high expectations" has nurtured a hotbed for this "short squeeze" of the crypto market.

Gamma Squeeze: What Is "Short Squeeze"?

"Short squeeze" comes from the stock market. Usually, when short positions need to close their positions to cover the underlying assets for some reason under the condition of insufficient liquidity, the demand for the underlying assets in the market is much higher than the circulation, thus causing the price to rise sharply due to insufficient supply.

Gamma Squeeze is an enhanced version of "short squeeze." Unlike traditional short squeeze, which requires a holding spot, gamma squeeze is realized through options. When a large number of call options are bought in the market, short sellers and market makers will choose to sell the call options and profit from the option fee. However, due to the unlimited risks and limited returns of options sellers, in order to prevent positions, market makers and short-sellers need to buy spots to hedge against the risk of rising prices.

Considering the low price of crypto options, the buyer can add considerable leverage to the option seller through lower costs. Moreover, under the condition of low market liquidity, the amount of spot assets that the options seller needs to buy is enough to form a considerable price. With the price rising, the options that originally did not reach the strike price successfully rose to the strike price, and the long-term profits further stimulated the purchase of the option, which led to a price spiral. This spiral is difficult to stop until the option expires and the position is closed.

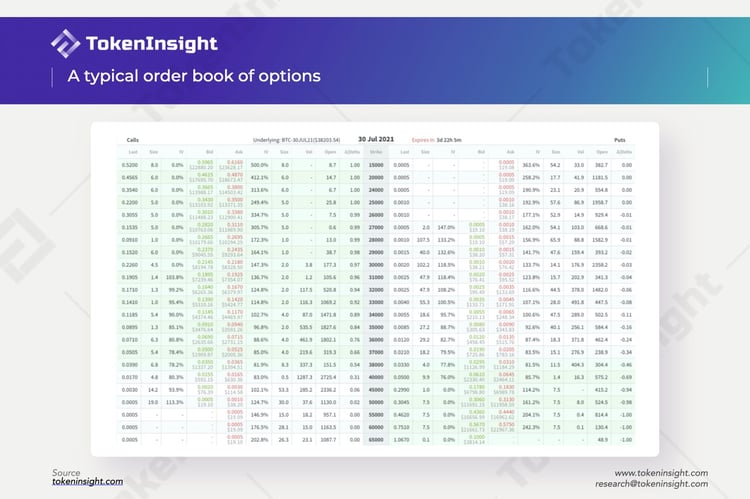

According to Deribit real-time data, as of 17:00 p.m. UTC+8, the number of bitcoin call options trading within 24 hours has exceeded 11,700, setting a new non-closing day trading volume record in the past month (under low volatility, daily non-closing day trading volume rarely exceeds 8,000). From the perspective of positions, the current distribution of bitcoin options at the $32,000-$40,000 strike price has reached 20,435, and these options are in just two days from "difficult to execute" imaginary value into "executable" real value, bringing considerable pressure to option sellers.

Who triggered this pressure, why and how big is it? Another option-related indicator Delta revealed some more critical information.

Delta That Can't Stop: How Is Bitcoin "Bought Up"?

Delta value, also known as hedging value, measures the degree to which changes in the price of the subject matter affect the price of the options. Generally speaking, the margin required by the options seller is calculated according to Delta. Delta value can also be used as a judgment indicator of whether the options can be realized: the closer Delta is to 0, the lower the probability of realizing the options. Delta exceeds 0.5, usually, the options have been realized.

For options sellers, the last thing they want to see is a spike in Delta, because it means that they need to pay a lot of costs to maintain their positions. But in the case of "gamma squeeze", Delta rose rapidly, which means that margin demand rose rapidly. Due to the current currency-based settlement of options, sellers can only choose to buy a large amount of Bitcoin spot in order to cope with the huge margin. At the same time, as the price rises, call options become real profits, more call options are bought, and more options with strike prices are raised. In a word, "It can't stop at all."

It is worth noting that out-of-money options typically have a Delta of less than 0.1. So, because of the rapid price rise, when the option becomes in-the-money, the Delta of the options will usually be higher than 0.5, and even when the price rises too fast, the option with a lower strike price will have a Delta value of 1. At this time, because the option has not yet expired, the option seller still needs to supplement the margin. In this "gamma squeeze", the seller of the options with a strike price of only $33000-$40000 will conservatively estimate that the margin required within 24 hours will not be less than 8962.86 bitcoins-considering the number of bitcoins currently traded on major exchanges, this is enough to cause the price to rise significantly.

Tracking "Gamma Bursts"

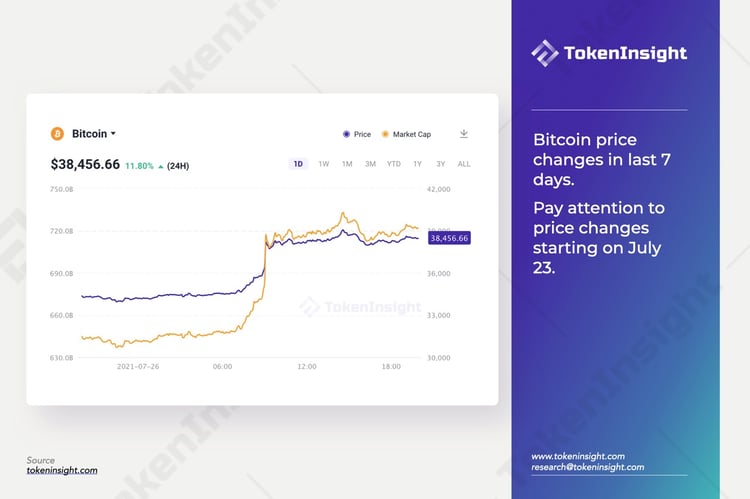

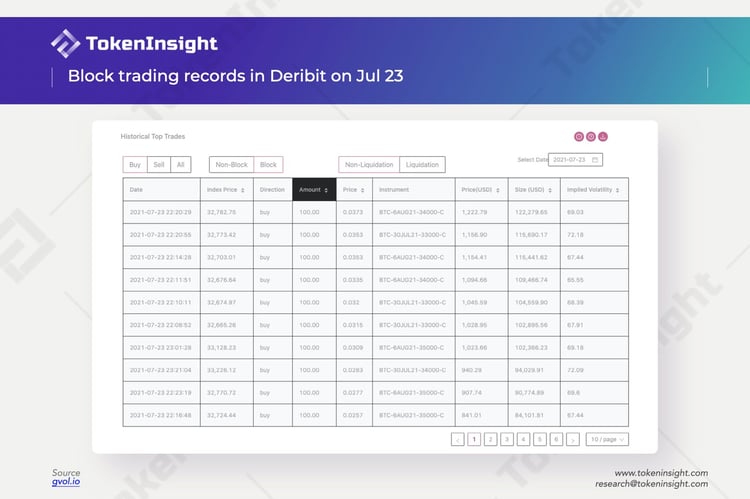

The driver of this "gamma squeeze" began to act on July 23. Before and after the options were delivered on July 23, nearly 3,000 bitcoin call options with execution dates on July 30 and August 6 were purchased. The next day, the price of bitcoin was pushed up to about $34,000. Until then, most people in the market still believed that this was only a positive result of macroeconomic data, and began to buy spot and contracts, until July 26.

As a result of the price hike, options with $34,000 strike price were successfully converted into real value on Sunday. The "gamma squeeze" began: on July 26, a large number of investors realized that the options market was "profitable" and began to buy call options. Option sellers (including market makers and bears) began to buy spots to hedge against put risks, which further pushed up asset prices. The crazy rise in delta caused a surge in the margin, and the bears were miserable: after the spare spot in their hands was exhausted, they could only replenish the margin after closing the contracts used for fund rate arbitrage with the spot, causing the open interests on some exchanges to drop by 15% at one time; a large number of transaction requests poured in, and even caused the Binance exchange to once again experience illiquidity. Judging from the current price trend, the "gamma squeeze" is still in progress.

After "Gamma Burst": Up or Down?

Judging from the records of each gamma squeeze in the traditional market, gamma squeezes often represent a sharp rise and fall in asset prices. The reason is that the short side's emergency purchase of spot stocks is mostly to meet margin requirements. After the option is delivered, its excess inventory will be released, thereby depressing the asset spot price again. For holders, large fluctuations in asset prices do not seem to be a good thing.

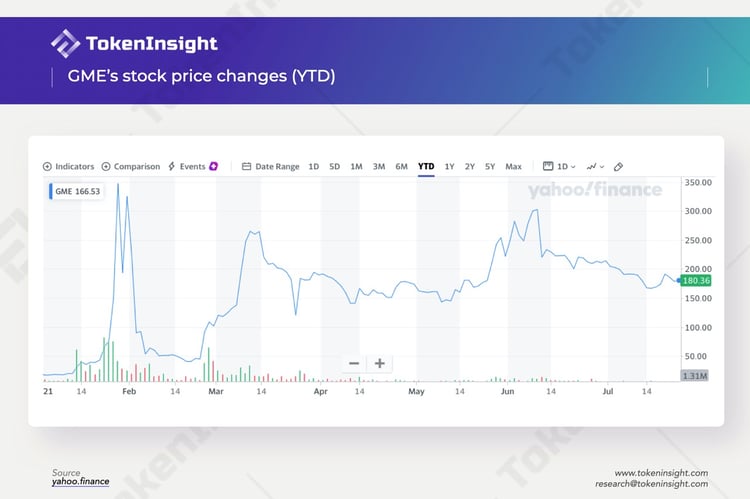

However, the "gamma squeeze" also reflects another trend: market activity and optimism are rising again, and higher than expected. Only when the number of market participants rebounds to a sufficient number, and there are enough bulls, can the conditions required for gamma short be met. After the short squeeze, GME did not collapse, but rose all the way to a high level. For cryptos, as the short squeeze occurs, market confidence is also rebuilding at the same time, and the rise in volatility increases trading activity, providing more possibilities and foundations for future market recovery.

Bitcoin

Ethereum

Options

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open