Crypto Fund 101: Direct Market Access Prime Brokerage

Welcome back to Crypto Fund 101! In this article, we will cover one of the most prominent services that will be used in crypto funds - the Direct Market Access Prime Brokerage service.

Welcome back to Crypto Fund 101! In this article, we will cover one of the most prominent services that will be used in crypto funds - the Direct Market Access Prime Brokerage service.

Prime Brokerage in Traditional Finance

A prime brokerage (PB) is a bundled group of services that investment banks and other financial institutions offer to hedge funds and other large investment clients that need to be able to borrow securities or cash in order to engage in netting to achieve absolute returns. The services provided under prime brokering include securities lending, leveraged trade execution, cash management, etc.

In traditional finance market, prime brokerage services are provided by most of the largest financial services firms, including Goldman Sachs, UBS, and Morgan Stanley… who provide a centralized securities clearing facility for hedge funds. When trading the most common long-short or general market neutral strategies, the hedge fund can have portfolio margin, which is netted collateral requirement across all deals handled by the prime broker who has the visibility to all positions, so their capital efficiency is high and the liquidation risk is lower.

Prime Brokerage in Crypto Market

Prime Brokerage in Crypto Market emerged in cryptocurrency market since late 2019 / early 2020. Initially, PB in crypto market tries to copy a full suite like PB in the traditional finance market to crypto market, where the only difference is the underlying, i.e., stocks to coins, futures to crypto futures…

Typically, a full suite of prime brokerage should cover below topics where various firms attempting to cover multiple above topics, like Coinbase Prime, FalconX, Galaxy Digital, B2C2, Fidelity Digital Assets…

- Custody: Institutional-grade custody of digital assets. In some cases, custody supports settlement requirements for trade executions, transaction processing, and same-day settlements

- Market Making / OTC: Providing two-sided liquidity for buyers and sellers

- Borrow / Lending: Offering access to borrow / lending digital asset credit markets where the provider acts as the trusted counterparty

- Derivatives: Providing liquidity across crypto derivative markets, whether that’s OTC or providing clearing services for derivatives markets (options and futures) and bilateral OTC derivatives. Can include pricing and structuring more exotic derivative contracts for clients

- Clearing / Settlement: Offering settlement assurances, or the act of transferring ownership (settling) in-line with the underlying agreement between parties. For digital assets, serving as a trusted escrow agent or sitting in between two trading parties is still an area that isn’t as robust as in traditional markets

- Execution: Trade messengers and execution platforms that can offer smart order routing and improve algorithmic systems for cryptocurrency trading. Execution can be either principal-based (where the other side is the dealer) or agency-based (where the intermediary is only a middleman)

Direct Market Access (DMA) Prime Brokerage in Crypto Market

Direct Market Access (DMA) means access to the order books and API of the exchanges for clients to trade directly, rather than relying on broker’s execution system (e.g., market-making, broker-dealers) to facilitate trades. When DMA client trade crypto, their order flow is trading clients -> crypto exchanges, rather than clients -> broker -> crypto exchanges.

In practice, Direct Market Access Prime Brokerage (DMA-PB) offers API key or login credential of sub-accounts under DMA-PB's main account of each venue / exchange (Binance, FTX, OKX...), plus loan (optional). Such service is also called sponsored access. Clients will fund the PB's sub-accounts (as own principal, or collateral to PB's loan), and run trading strategies with the PB's sub-accounts directly to crypto exchanges.

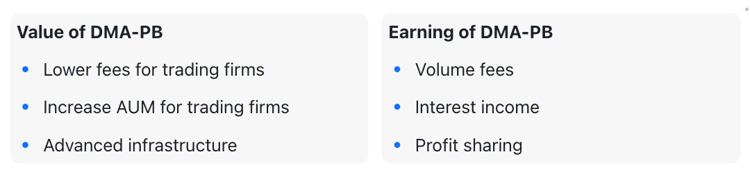

Typical clients are trading firms, especially quant trading firms who want to improve their trading fees, increase AUM with leverage, or have access to advanced infrastructure.

Why Clients Use DMA-PB Service and What Do DMA-PB Earn?

In traditional market, the prime broker finances the client's margined long and short cash and security positions, in return earns fees ("spreads") on interest and, in some cases, fees for clearing and other services. It also earns money by rehypothecating the margined portfolios of the hedge funds currently serviced and charging interest on those borrowing securities and other investments.

DMA-PB service in crypto market has similar business model. Specifically, they earn

1. Lower Fees for Trading Firms/Volume Fee for DMA-PB

In short, DMA-PB aggregates volume from multiple small-medium trading firms and negotiate with exchanges for a high VIP tier trading fee, so trading firms can improve trading fee, and trade as if it's their own accounts without any extra latency.

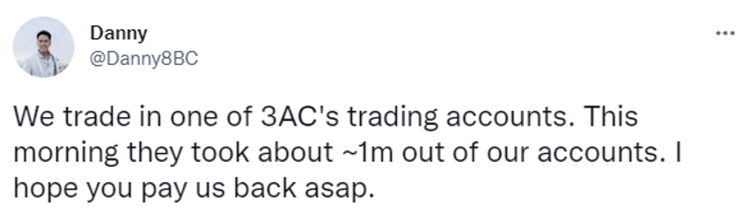

There's a public explanation of DMA-PB service by @Danny8BC (Danny, Head of Trading @8BlocksCapital), where 8Blocks Capital is trading with 3AC's DMA-PB service.

Why is this a sustainable business relationship? Let’s take a real example with Binance Trading Fees

Suppose trading firm A runs strategy with

- Total AUM of $100 million (already large in crypto)

- 50% of their AUM on Binance (quite concentrated)

- Trade daily 3.33 times of their AUM (high frequency)

So that firm A can reach $5 billion volume in 30 days, which qualifies VIP 7 on Binance

If the prime broker is on VIP9 fee tier and offer firm A to trade with VIP 8 fee tier, it’s mutually beneficial

- For Firm A, monthly $5 billion trading volume, this client’s fee will improve

- Maker: Firm A VIP7 0.4bp, PB charge by VIP8 0.2bp, improvement is 0.2bp

- Taker: Firm A VIP7 2.2bp, PB charge by VIP8 2.0bp, improvement is 0.2bp

simply save 0.2 bp * $5 bn = $100k, which adds 0.2% on their monthly return, without considering extra trading opportunities

- For DMA-PB, they will earn from firm A

- Maker: PB VIP9 0bp, PB charge client by VIP8 0.2bp, profit is 0.2bp

- Taker: PB VIP9 1.7bp, PB charge client by VIP82.0 bp, profit is 0.3bp

Suppose Firm A is trading 100% maker orders, DMA PB will 0.2 bp * $5 bn = $100k (they would earn extra if they qualify market maker program). If DMA-PB is able to aggregate 10 clients like firm A, the monthly fee collected by DMA-PB would be $1 million

In reality, most trading firms have much smaller AUM and less frequent trading strategies that spread across several different venues, who can barely keep VIP5 on Binance, but still need a competitive fee to capture trading opportunities.

The main risk is mainly to trading clients

- DMA-PB brings additional counterparty risk, as the fund custody is under DMA-PB's exchange accounts

- DMA-PB controls API keys for asset withdrawal, so client's withdrawals for rebalancing (usually needed for cross-venue arbitrage strategies) might be delayed due to DMA-PB's operational inefficiency

The risk for DMA-PB is that they have to maintain the aggregated trading volume and negotiate with exchanges to improve/ maintain fee tier, especially when the whole market is inactive. In 2022, some DMA-PB might not be able to maintain VIP9 fee tier on Binance, hence incumbent trading clients will switch to other competitors, which further reduces their trading volume.

2. Increase AUM for Trading Firms/Interest Income for DMA-PB

Besides trading fee, DMA-PB also offers financing to trading clients, so-called OTC leverage (off the exchange), where trading firm clients use PB's funding in DMA-PB’s accounts while maintaining certain scale of collateral.

Usually, DMA-PB only finances delta neutral strategies because of low volatility. The financing ratio (loan:collateral) starts from a conservative value like 1:1 (2x to collateral) or 1:2 (3x to collateral). After 1-2 month’s observations, if the strategy is verified to be delta neutral and robust, resulting in consistent profitability and acceptable drawdown, the trading firm can have their leverage gradually increased to 10x from DMA-PB.

Crypto exchanges also provide financing options, but why is DMA-PB more popular than exchanges for trading firms? The rationale behind as below

- DMA-PB offers cross-venue financing

- DMA-PB oversees all the positions across venues, so they can offer higher leverage than each single exchanges

- DMA-PB usually keeps the same interest rate in the contract period, while exchange lending rate can fluctuate greatly

The business model for DMA-PB financing is like an over-collateral secured loan. Because the trading account is eventually owned by DMA-PB, if the client's collateral has been completely lost, DMA-PB can just execute contingency plan to unplug the trading API key & secret, and liquidate all the positions and assets in the accounts to recover their loan principal + interest (slippage expected for large positions or low liquidity instruments).

The risk for DMA-PB, is that if the client's trading goes wrong for whatever reason and loses money drastically, DMA-PB has to stay aware of the incident instantly, and immediately execute contingency plan to verify situation and halt trading to protect the principal.

3. Advanced Infra for Trading Firms/Profit Sharing for DMA-PB

Some DMA-PB has advanced infrastructure that is superior to the market level.

One example is co-location with exchanges for shortest possible latency. In crypto market, trading firms usually implement basic co-location, which is to run strategies in the same AWS region, say running strategy in AWS Tokyo where Binance matching engine sits.

While there is advanced co-location, which is using Virtual private clouds (VPC) and VPC endpoints to get/ post API requests, which brings best possible latency (can be faster than basic co-location by few ms). However, exchanges allow this to very limited partners, who bring top volume or top liquidity. With aggregation of volume, DMA-PB combines the bargaining power to have advanced co-location implemented.

There’s both pros and cons for trading firm clients though. If their trading strategy is latency sensitive, profitability will be improved. However, this requires the strategy to be running on PB’s servers (IP whitelist) where they might have concern on their strategy privacy.

To make stronger relationships and minimize trust concerns, some DMA-PB plays the role of FoF, and share PnL with those high frequency trading firms who have strong need for both advance infra and strategy privacy.

Key Operations and Risks of DMA-PB

LTV/Collateral Coverage Ratio

As DMA-PB facilitates leverage to trading firms, primarily through loans secured by the equity balance of their clients, DMA-PB is exposed to the risk of loss when the value of collateral held as equity declines below the loan value, and the client is unable to repay the deficit.

Here the core metric is LTV, by comparing the loan vs. total asset value shown in the accounts. Some firms might use collateral coverage ratio which is mirror expression of LTV (total asset value / loan). In general, LTV has to be below 1 and collateral coverage ratio has to be above 1.

Trading Risks

Pre-trade risk compliance

When setting up new sub-account, or generating API in exchanges like Binance, FTX, OKX... There are settings to set trading scope, leverage ratio...

Pre-trade risk control cannot happen in DMA, because the trades are directly sent to exchanges. Once API key set up is done, there's no other way that DMA-PB could block trades.

If DMA-PB has to set an OMS between trading clients and exchanges for pre-trade compliance, it will cause additional latency and typically won't be accepted by algo traders.

On-Trade Trading Metrics/Exposure

This is the most effective and realistic measure for DMA-PB to control risk.

As mentioned above, to ensure loan safety, DMA-PB requires financed trading firms to use only delta neutral strategies, with max. 2-3x leverage rate in the exchange to ensure low drawdown and low risk of liquidation. DMA-PB should implement below monitors to make sure the strategy is consistent with the thesis.

Post-Trade Contingency Plan

There has to be a contingency plan once the client LTV / collateral coverage ratio gets unhealthy. but it's not wise to make immediate liquidation. The reason is that the trading client

So the common approach, is that once the collateral level gets risky:

- The risk monitor sends immediate alert / margin call to the PB risk control team and the trading client

- Risk control teams go check the exchange account to confirm the situation and contact the trading client

- If the client commits to top up collateral in the agreed timeline, that's ok. But if the situation is bad (e.g., client does not respond while loss is quickly increasing, or client refuses or fails to top up collateral in time), DMA-PB will -

- switch their client's API keys from trading to read-only, so client cannot trade any more. 3.2 DMA-PB will switch their monitor key from read-only to trading, and switch on a forced liquidation program to clear all the positions and convert all the assets into loan currency (e.g., USDT)

Usually, a slippage is expected during liquidation, so the DMA-PB has to take immediate action before the client loses all collateral, and if the client trades low cap altcoins (typical for funding rate arbitrage) the LTV level has to be more convervative.

Custody

DMA-PB keep all the funds under their own exchange accounts while they need to distribute API keys and secrets to clients. It’s crucial to keep all the API keys and secrets within 100% safe control.

There can be different layers of exchanges API key

- Read-only: for monitoring and trade reconciliation purpose

- Withdraw / transfer: for moving fund within the DMA accounts

- Trading (spot / derivatives): for placing and cancelling orders

- Usually there should be clear hierarchies to access those keys for different purpose

- Read-only: for portfolio and risk management system

- Withdraw / transfer: has to be enabled based on whitelist so fund can only be transferred within DMA-PB's accounts

- Trading: for trading clients to trade and strictly limit IT address

There has to be real-time monitoring and alerting system to ensure everything is in order. When there’s anything going wrong, a circuit breaker mechanism has to be implemented by deleting the trading key and liquidating all the positions to protect the loan principal.

Potential Advanced Features - DeFi Trading

DMA-PB used to support on top CEX like Binance, FTX, OKX… With the emerging demand from DeFi trading, there are some PB starting to provide access to DeFi which requires more advanced features in blockchain wallet management.

There are certain risks around each DEX, for example there’s FAST_WITHDRAWAL function in DYDX that can withdraw fund directly from L2 protocol to any L1 address with API key & secret (private key of L1 wallet not required), where the DMA-PB has to make adequate measures to control the risk.

Click here to read more about how 1Token supports crypto fund managers.

Reference

[1] It’s Prime Time for Crypto Prime Services

https://www.coindesk.com/sponsored-content/its-prime-time-for-crypto-prime-services/

[2] What does Prime Brokerage look like for Digital Assets?

Fund

Lending

Derivatives

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open