Crypto Regulation 101

The crypto market continues cooling down and there are few exciting projects and news coming out. While the market is quiet, governments across the globe are busy drafting crypto regulation frameworks. A proper and clear supervision framework is key for the future development of crypto.

This article summarizes crypto regulation development in some major countries and regions. It serves as a bird's view of what is happening around the world.

The crypto market continues cooling down and there are few exciting projects and news coming out. While the market is quiet, governments across the globe are busy drafting crypto regulation frameworks. A proper and clear supervision framework is key for the future development of crypto.

This article summarizes crypto regulation development in some major countries and regions. It serves as a bird's view of what is happening around the world.

TL;DR

- If a token is categorized as a security, it is most likely to fall under the regulation of securities, and all countries have existing frameworks to supervise securities activity;

- Since it is almost impossible for a crypto project to comply with securities law, most crypto projects have to try their best effort to avoid their tokens being classified as securities. Instead, they prefer to label their tokens as utility tokens or governance tokens;

- While some countries and regions (like E.U.) have already drafted a comprehensive crypto regulation framework encompassing both security tokens and utility tokens, others are only at the preliminary research phase (like the U.K.) to study how to regulate crypto activities;

- Most countries and regions have established a framework to register centralized crypto service providers (e.g. exchanges, custodian wallet), however, decentralized crypto service providers such as DeFi, DAO, seem to have not been covered in any of them yet;

- Most countries and regions do not have a specific regulation for stablecoins, however, if a stablecoin is fully backed by fiat and operated by a company, it is most likely to fall into exiting financial regulation related to electronic payment tokens or e-money;

- From a global perspective, the progress in the U.S. is no doubt the most important one, it is also the most complicated one due to the nature that the U.S. financial regulatory structure is complex, with responsibility fragmented among multiple agencies that have overlapping authorities. Therefore, I will start with E.U. and U.K. to have a general idea of the crypto regulation in these most developed countries and then follow by U.S., so that you could find out why the situation in the U.S. is complicated.

This article covers countries and regions in below order:

- E.U.

- U.K.

- U.S.

- Singapore

- Dubai

- Hong Kong

E.U. - Most Comprehensive Crypto Regulation Framework

While a few European countries, like Germany, already have basic crypto regulations, I would like to focus on E.U. as a whole rather than dig into each country's particular situation.

The E.U. as a whole has proposed one of the most comprehensive regulations for crypto in the world.

The framework involves two major parts:

- Market in Crypto Asset (MiCA) - E.U. has rolled out a provisional agreement of "Market in Crypto Asset"- MiCA regulation to give issuers of crypto assets and service providers of related assets a unified rule to serve clients across E.U. MiCA focuses on assets that are not classified as securities.

- DLT (Distributed Ledger Technology) Pilot Regime - if a crypto asset is considered to be a financial instrument, it will be regulated under the European securities law (MiFID II). The DLT Pilot Regime provides a test phase for crypto assets considered to be securities and gives some regulatory exemptions from the existing securities law - MiFID II.

MiCA - the First Comprehensive Crypto Regulation

MiCA is the first crypto regulation in the world that clearly outlines a comprehensive framework. MiCA focuses on all crypto asset that is not subjected to other regulations, such as security token (which are subject to securities law) or central bank digital currencies.

MiCA covers:

- E-money tokens

- Asset-referenced tokens

- Utility tokens

MiCA clearly set out some requirements for crypto asset issuance, such as:

- The publication of a whitepaper with some similarities to a security issuing prospectuses

- The necessity of being authorized to issue crypto asset

Crypto asset services providers that provide custody, administration, and provision of advice on crypto assets are all regulated under MiCA.

DLT Pilot Regime - a Test Sandbox for Securities Tokens

If apply the current securities law to crypto securities tokens, no project could be able to issue tokens at all. The DLT Pilot Regime seek to offer some exemption from securities law for securities token and place a cap on the capital involved.

Summary

E.U. is about to finalize one of the world's most comprehensive crypto regulation frameworks, encompassing both securities tokens and utility tokens. It has also offered the DLT Pilot Regime for securities tokens rather than applying the current securities law in full to securities tokens.

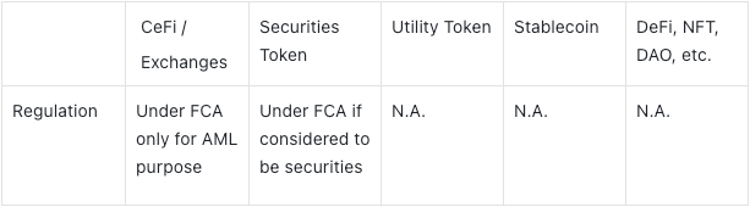

U.K.

The Major Regulatory Body for Crypto - FCA

FCA - Financial Conduct Authority regulates the securities and financial service industry and is now the main body responsible for crypto regulation. Currently, crypto exchanges must register with FCA to conduct business in the U.K.

FCA's role in registering crypto exchanges is solely for anti-money laundering purposes, whilst most crypto assets and associated businesses remain unregulated.

Recent Progress

In April 2022, the U.K. government announced plans to become a "global crypto-asset technology hub" with stablecoins being used "as a recognized form of payment".

Some highlights of the plan include:

- A financial market infrastructure sandbox to enable firms to experiment and innovate

- A crypto asset engagement group to work closely with the industry

- Initiate a research program to explore the feasibility of using distributed ledger technology for sovereign debt instruments

Summary

The crypto regulation in the U.K. is still in the preliminary consultation phase. Due to the fall of Terra, stablecoin regulation could probably first be drafted, and the regulation for broader crypto industry, including token issuance and DeFi has not been put on the agenda.

U.S. - Complex, and Entangled

The crypto regulation in the U.S. is complex in terms of two dimensions:

- Different rules/approaches have been implemented by state-level governments, while the Federal government level has not yet had a formal rule regarding crypto;

- At the Federal level, different agencies held different views regarding crypto regulation, where the Securities and Exchange Commission (the SEC) poses a tougher stance and the Commodity Futures Trading Commission (the CFTC) is much friendlier. Whether crypto shall be regulated by the SEC or the CFTC is undecided, and the results could result in a stark difference in regulation stance.

Federal Governance-Level Regulation

There is currently no crypto regulation at the Federal level that covers crypto-related activities and authorizes Federal Agencies to regulate crypto. A number of crypto bills have been proposed by different senators.

The process in the U.S. political structure for a bill to pass follows the below procedure:

- Get agreement from several political committees, including (but not limited to) Banking Committee, Agriculture Committee (which oversees commodities), etc.

- Present to U.S. Senator for a vote, if approved,

- Send to House of Representatives for a vote, if approved,

- Sign by the U.S. president into law, the whole process is complete.

No crypto bill has even finished the first step. So, it is still a long way to go for a Federal level crypto regulation.

The most important bill up to date is the one proposed by Cynthia Lummis and Kirsten Gillibrand, the "Responsible Financial Innovation Bill". If you are interested in a detailed explanation for this bill, here is a video by Coin Bureau.

State Government-Level Regulation

Federal-level regulation may not be enacted any time soon, making it worthwhile to have an overview of how different states regulate crypto activities.

There have generally been two approaches to regulation at the state level.

Some states have quite favorable regulations exempting crypto from state securities law and/or money transmission statutes. Examples of this category include:

- Wyoming: it allows a new type of crypto banks; it also gives DAO a legal status as DAO LLCs; (Reference: Regulatory Landscape in Wyoming and Wyoming's Leadership in Cryptocurrency)

- Colorado: it exempts crypto from state securities regulations and accepts taxes payment in crypto;

- Ohio: it accepts taxes in crypto;

- Oklahoma: it introduces a bill authorizing crypto to be used, offered, sold, exchanged, and accepted as an instrument of monetary value within its government agencies;

Some other states hold a tougher stance regarding Crypto, such as New York, Maryland, and Iowa.

Singapore

In Singapore, the Monetary Authority of Singapore (MAS) is responsible for crypto regulation.

The way MAS regulates crypto is to apply the existing legal framework where possible, rather than draft an independent new crypto regulatory framework.

Crypto activity is subject to two key regulations

- Payment Services Act 2019 (PSA) - this is to regulate the service providers to include the transfer of tokens, provision of custodial wallet service, etc.

- Securities and Futures Act (SFA) - crypto tokens that constitute financial instruments are regulated by the existing securities law (SFA). If tokens are deemed to be financial instruments, it is required to prepare a prospectus and register the offer with the MAS.

For stablecoin, if it is a fiat-backed centralized stablecoin, it will be classified as "e-money" and is covered in PSA.

Dubai

Instead of regulating crypto-related activity under existing regulatory bodies, Dubai set up a completely new authority for crypto assets - the Dubai Virtual Assets Regulatory Authority (VARA).

VARA is mandated to organize and set rules and controls for virtual asset-related activities. It covers full range of activities:

- Issuing and trading of tokens;

- Authorizing crypto services providers;

- Organizing the operation of crypto platforms and portfolios.

Hong Kong

SFC and HKMA are responsible for regulating crypto-related activities:

Securities and Futures Commission (SFC) - responsible for securities and futures markets

The Hong Kong Monetary Authority (HKMA) - responsible for financial stability and the banking system.

In early 2022, HKMA and SFC jointly introduced a new regime for financial intermediaries to deal with "virtual asset" - related products and provide crypto asset trading and advisory services.

The framework mainly focuses on CeFi entities, no clear regulatory progress regarding token issuance, DeFi, or DAO.

Closing Thoughts

This article is not a comprehensive summary of crypto asset regulations around the world. It's just a brief of the regulatory process in each of the major jurisdictions to date. We hope that readers will gain a basic understanding of the key milestones in crypto asset regulation through the article. In addition, because the crypto industry is evolving so rapidly, lots of information in this article may no longer be accurate in terms of timeliness. We welcome readers to point them out at any time and we will make corrections as soon as possible.

Policy and Regulation

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open