Crypto Market Insights 2023Q2

After the boom in Q1, the crypto industry did not experience many ups and downs in Q2, but more changes from the traditional market. So what happened in Q2? What was the impact? Let's take a look.

After the boom in Q1, the crypto industry did not experience many ups and downs in Q2, but more changes from the traditional market. So what happened in Q2? What was the impact? Let's take a look.

After the boom in Q1, the crypto industry did not experience many ups and downs in Q2, but more changes from the traditional market. We reviewed the significant events and hot tracks in the past quarter, hoping to understand the development trend of crypto industry better, and summarize some patterns to better look forward to the future.

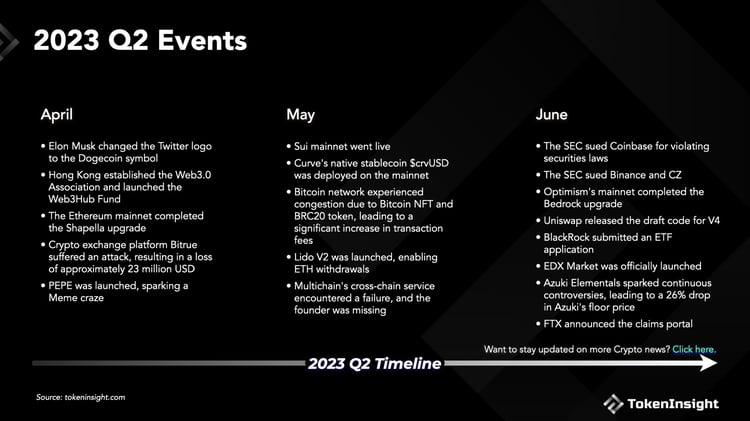

April and May were relatively quiet, with the exception of the successful completion of the Ethereum Shapella upgrade and the launch of PEPE, which was the biggest news story. June was dominated by dramas: the SEC sued two of the world's largest centralized exchanges, Coinbase and Binance, and controversies erupted over the Azuki Elemental offering. There was also the good news of BlackRock filing an application for a Bitcoin Spot ETF.

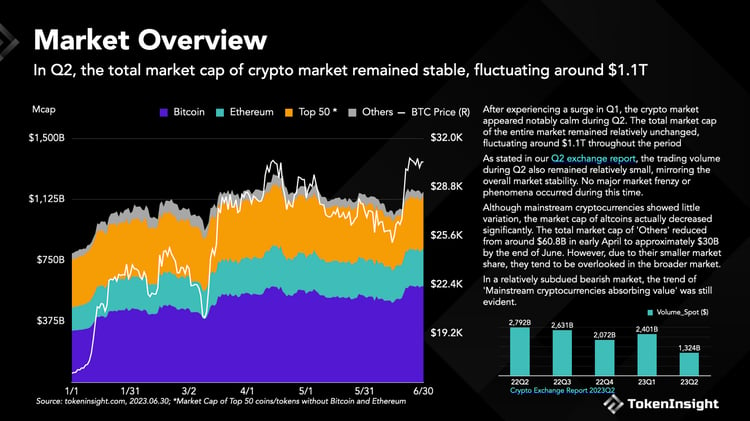

Q2 Crypto Market Cap Fluctuates Around $1.1T, Bitcoin&Ethereum Share Expands to Over 70%, Altcoin Share Slips Badly

After the surge in Q1, the crypto market was quiet in Q2. The total market cap of the global crypto market remained relatively unchanged, fluctuating around $1.1T.

As stated in our Q2 exchange report, the trading volume during Q2 also remained relatively small. There's no major market frenzy or phenomena occurring in this quarter.

Bitcoin and Ethereum continue to dominate the market in Q2, with a market share of more than 70%, up 5% from 65% in Q1. Coins other than Bitcoin and Ethereum in the Top50 accounted for 27.39% of the global crypto market cap, a drop of 8.71% from the previous quarter. The share of coins outside of the Top50 fell by about 53.19%.

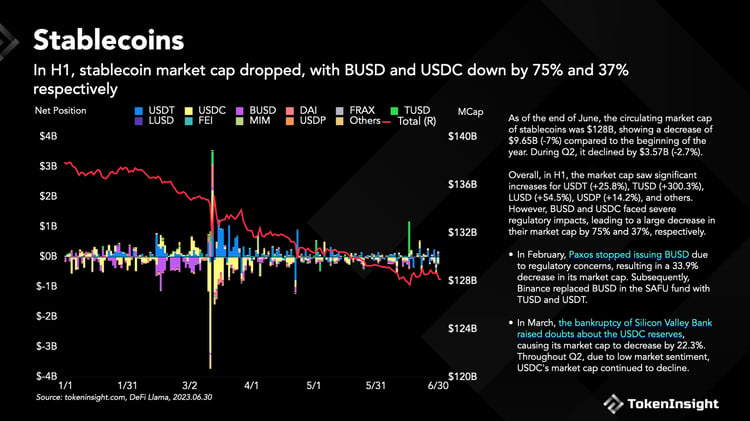

Stablecoin Market Cap Continues to Decline, Ending Q2 with $128B in Circulating, Net Outflow of 2.7%

At the end of June, the circulating market cap of stablecoin was $128B, showing a decrease of $9.65B (-7%) compared to the beginning of the year. Q2 saw a decrease of $3.57B (-2.7%).

Overall, in H1, the market cap saw significant increases for USDT (+25.8%), TUSD (+300.3%), LUSD (+54.5%), and USDP (+14.2%). However, the market cap of BUSD (-75%) and USDC (-37.2%) decreased severely due to market risk and industry regulation.

In February, Paxos stopped issuing BUSD due to regulatory concerns, resulting in a 33.9% decrease in its market cap. Subsequently, Binance replaced BUSD in the SAFU fund with TUSD and USDT.

In March, the bankruptcy of Silicon Valley Bank raised doubts about the USDC reserves, causing its market cap to decrease by 22.3%. Throughout Q2, due to low market sentiment, USDC's market cap continued to decline.

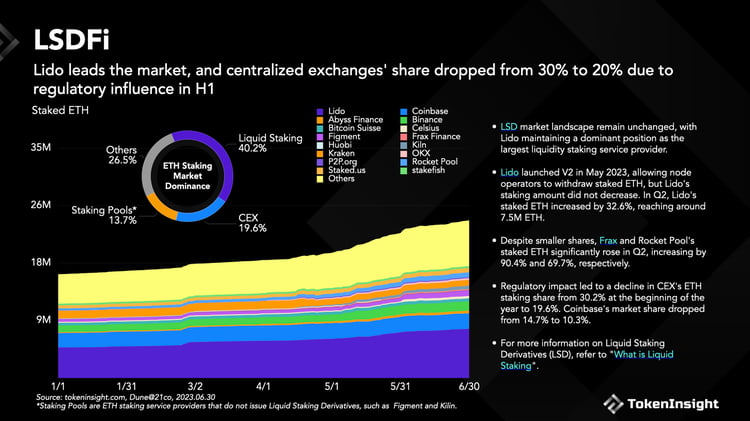

Staked ETH Increases Instead of Decreasing After Shapella Upgrade, Staking Rate Nearly 20% at End of Q2, LSDFi Growing Rapidly

Since the Shapella upgrade, Ethereum stakings have accelerated rather than declined. By the end of June, there were 23.54M staked ETH. Q2 ETH staking rate increased from 14.95% to 19.57%.

The LSD market landscape remains unchanged. Lido maintained a dominant position as the largest liquidity staking service provider, with 32% of the market share at the end of Q2 with 7.5M staked ETH.

CEX's share of ETH staking declined from 30.2% at the beginning of the year to 19.6% as a result of regulation. Coinbase's market share fell from 14.7% to 10.3%.

As the LSD market continues to expand, more and more DeFi protocols are integrating LSD. LSDFi is growing rapidly, and at the end of Q2, the TVL of the LSDFi market was around $570M.

Lybra Finance is currently the largest LSDFi protocol, launched in April this year. By the end of June, Lybra Finance had a market cap of $14.8M and a TVL of $187M.

The LSDFi market is still in a relatively early stage, with no significant competitive landscape. As of the end of June, the staked ETH value amounted to around $44.5B, and the TVL in the LSDFi market only accounts for 1%, leaving plenty of room for growth.

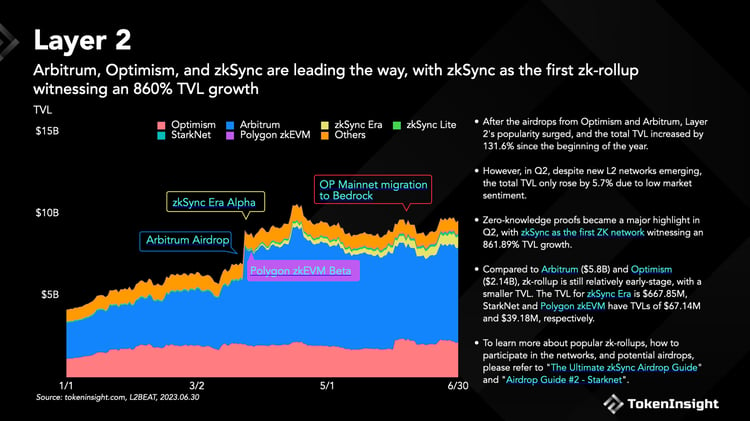

The total TVL of Layer-2s increased by 5.7% in Q2, with zkSync TVL reaching $688M, an increase of over 800%

In Q2, the total TVL of Layer-2s increased by 5.7%. Among them, zkSync, the first ZK-Rollup Layer-2 network, saw a TVL increase of 862%. Compared to Arbitrum ($5.8B) and Optimism ($2.14B), ZK-rollup is still relatively early and has a lower TVL. zkSync Era has a TVL of $668M, while StarkNet and Polygon zkEVM have a TVL of $67M and $39M.

As of the end of Q2, the Layer-2 networks with the highest daily transaction volumes were Arbitrum (1M), zkSync Era (669K), and Optimism (562K). However, none of them were able to exceed the daily transaction volume of the Ethereum mainnet (1.13M).

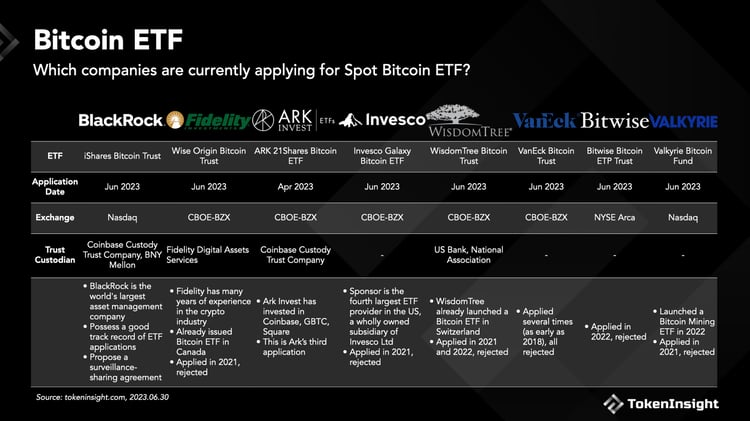

Traditional Institutions Start Looking at Bitcoin Spot ETFs, 8 Institutions Have Filed Applications

With the gradual implementation of regulations, traditional asset management companies in the market have set their sights on the "sweet spot" of Bitcoin ETFs. BlackRock was the first to submit the application, followed closely by Fidelity, Invesco, and WisdomTree.

Bitcoin

Ethereum

Stablecoins

Tether

Circle

Staking

Coinbase

Liquid Staking Derivatives (LSD)

Layer 2

Arbitrum

Optimism

zkSync Era

BRC 20

Index

Download

In This Article

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open