Deep Dive of Pendle

Pendle pioneered on-chain yield trading via PT/YT, yet its 2025 expansion was largely incentive-amplified. This report reviews the TVL drawdown, long-run fee-rate compression risk, and the Boros’ push for sticky demand.

Pendle pioneered on-chain yield trading via PT/YT, yet its 2025 expansion was largely incentive-amplified. This report reviews the TVL drawdown, long-run fee-rate compression risk, and the Boros’ push for sticky demand.

Key Takeaways

- Pendle tokenizes yield by splitting yield-bearing assets into PT (principal) and YT (yield). This lets users trade/hedge future yield and choose fixed-like vs floating exposure.

- Pendle’s 2025 TVL boom was largely driven by points/airdrop incentives and leverage loops. Capital flowed in because the carry was attractive and scalable.

- The TVL collapse was mechanical once incentives ended and yield compressed below borrowing costs. When carry turned negative, users deleveraged and redeemed at speed.

- Pendle's “undervaluation” narrative ignored weak value capture relative to TVL. High MC/TVL and elevated P/F reflected premium expectations more than durable earnings power.

- Long-run margins may compress as crypto yield trading matures. TradFi IRS markets are high-volume but low-margin, and on-chain rates trading may converge toward that profile in a more institutional/competitive regime.

- Boros (V3) is positioned as a pivot toward more capital-efficient yield speculation. The key question is whether it can create “sticky” usage without incentive-driven liquidity.

What is Pendle?

Pendle is a DeFi yield-trading protocol that “unbundles” the cashflows of yield-bearing assets so they can be priced, traded, and hedged like fixed-income instruments. Instead of only holding a yield token (e.g., staked ETH, lending receipts, LP positions) and accepting whatever APY comes, Pendle lets markets discover the price of future yield and lets users choose between something closer to fixed-rate vs floating-rate exposure.

Mechanically, Pendle routes a yield-bearing position through a standardized wrapper called SY (Standardized Yield), then mints two tokens in equal amounts:

PT (Principal Token): a claim on the principal at maturity (economically similar to a zero-coupon bond).

YT (Yield Token): a claim on the variable yield stream produced up to maturity (economically similar to a yield strip / floating leg).

This split is what makes “yield” tradable as a standalone instrument.

Pendle runs markets that are designed around the behavior of PT/YT as they approach expiry. In V2, the AMM is explicitly tuned for yield trading dynamics (e.g., price range behavior and time-to-maturity effects), and was adapted from Notional’s AMM model. In practice, the most important mental model is: PT trades at a discount before maturity and converges toward redemption value at maturity. That discount effectively encodes an implied fixed yield (bond math intuition). On the other hand, YT becomes the levered “bet” on realized yield versus what the market priced in.

Tokenized yield can materially improve capital efficiency in DeFi. Conventional yield farming often requires long lockups, which reduces liquidity and flexibility. Pendle allows users to monetize or transfer yield exposure without unwinding the underlying position, creating more options: realizing yield upfront, hedging future yield, deploying leverage more efficiently, or rebalancing without waiting for rewards to accrue.

Despite the protocol’s strong innovation and narrative positioning, both Pendle’s Total Value Locked (TVL) and the $PENDLE token price have been in a sustained decline since late 2025. The sections that follow examine the drivers of that downturn and analyze Pendle’s underlying business model and revenue structure to better understand its place within the broader DeFi landscape.

The Falling of Pendle TVL

Pendle’s rise in 2025 was tightly linked to the broader “points/airdrop” trade: protocols seeking distribution used incentives to attract liquidity, while sophisticated users used Pendle to structure yield positions that maximized reward capture and capital efficiency. Even exchange and research content in the market increasingly described Pendle as a key venue for token launches and airdrop-style farming flows, rather than only a neutral yield marketplace.

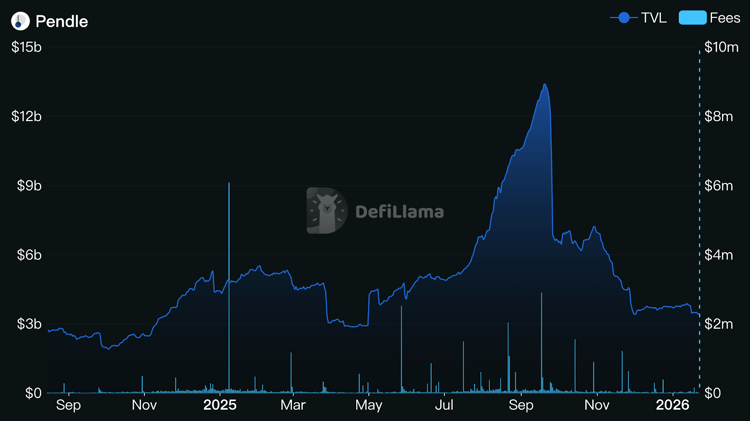

Despite the conceptual breakthrough and strong narrative momentum, Pendle’s on-chain traction weakened after late 2025. In January 2026, Pendle’s TVL was $3.44B, representing a 74.2% decline from a $13.38B peak in September 2025. Over a similar window, $PENDLE fell from an August 2025 high of $6.85 to $2.13 (a 68.9% drop).

To explain why the unwind was so violent, we anchors the story in the rally that preceded it: between May and August 2025, Pendle’s TVL surged from roughly $3B to $10B, adding about $7B of liquidity in a short period—an expansion framed as extraordinary even by crypto standards. This growth coincided with the rise of yield-bearing stablecoin strategies, particularly those associated with Ethena, which used Pendle as a venue to structure and lever yield trades.

Pendle's TVL (left) and Fees (right)

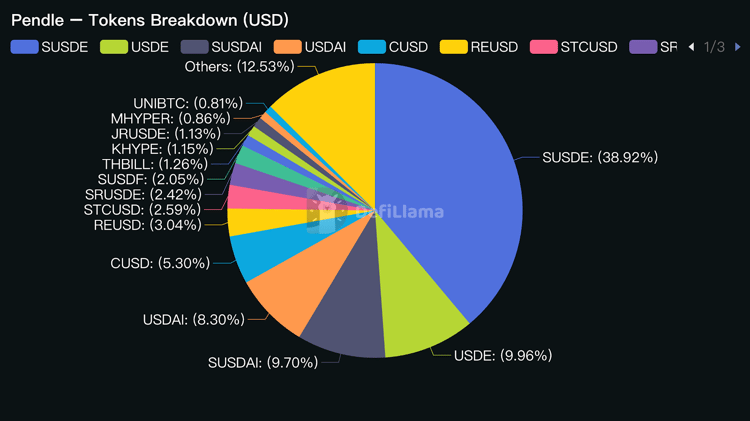

At the time, roughly 70% of Pendle’s stablecoin TVL was concentrated in USDe and related derivatives, and even after the peak period these assets still represented about half of the protocol’s locked capital. The driver was straightforward: Ethena’s USDe sustained yields that outperformed many mainstream liquid staking tokens benchmarks, while Pendle’s PT/YT framework provided the infrastructure to convert that yield into tradable and levered rate exposure.

The dominant strategy was a recursive leverage loop. Users could acquire PT, post it as collateral to borrow stablecoins, swap the borrowed liquidity back into USDe, and repeat the process to scale exposure. In parallel, YT offered two paths: hold it to earn the variable yield and rewards through maturity, or sell it upfront to monetize expected yield immediately. During the peak phase, the implied fixed yields on PT USDe and PT sUSDe were approximately 13% and 12%, while stablecoin borrowing costs on Aave were around 5%–7%. That spread translated into an estimated 5%–6% net carry per leverage cycle, which largely explains the rapid expansion in both leverage demand and headline TVL.

The reversal came when incentives faded and the economics turned against the loop. In September 2025, the end of Ethena’s Season 4 incentives coincided with a sharp exit of short-term, yield-sensitive liquidity from Pendle. At the same time, 33 Ethena-linked pools with roughly $1.35B in value reached maturity, forcing users into PT/YT redemption decisions. When market participants evaluated rolling positions, sUSDe APY had compressed from roughly 12%–13% to about 4.7%, falling below an approximately 5% USDC borrowing cost on Aave. Once the carry flipped negative, the unwind became mechanical: users repaid Aave debt, reduced PT/YT exposure, and redeemed USDe, triggering a cascading outflow.

In effect, the Pendle–Ethena–Aave feedback loop amplified TVL across all three protocols. It was a classic “Mega Points” structure: incentives and yield differentials attracted fast-moving capital into a reflexive leverage loop, and once profitability disappeared, liquidity withdrew with equal speed.

Tokens locked in Pendle

The “Undervaluation” Myth: Narrative Strength vs Monetization Reality

At its zenith in September 2025, Pendle achieved a TVL of $13.38B, briefly securing a position among the top five DeFi protocols globally. While the prevailing market consensus—driven by a market cap and FDV exceeding $1 billion—viewed Pendle as significantly undervalued, a cold analysis of its fundamental architecture suggests that this $1B valuation was a fair, if not generous, reflection of its operational reality.

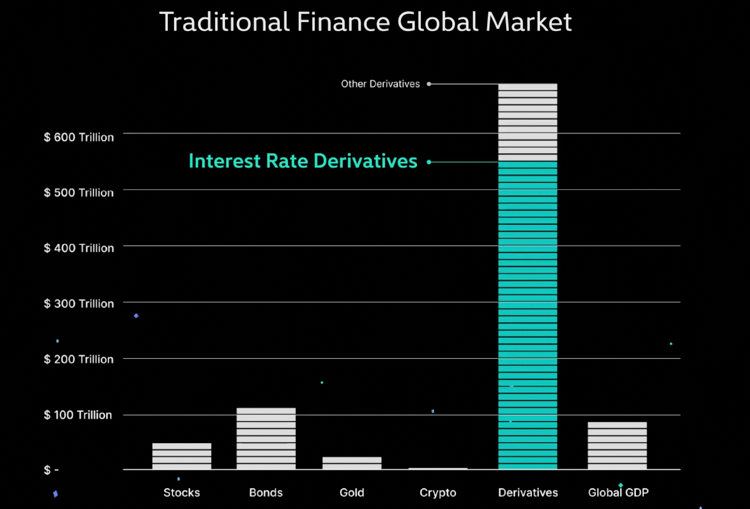

Pendle pioneered the on-chain Interest Rate Swap (IRS) market, a sector that remains one of the largest pillars of traditional finance. In TradFi, nearly all yield-bearing assets are actively traded via derivatives; in the crypto ecosystem, however, yield trading penetration currently sits at a mere 3% to 5%.

Trading volume across global markets

As the dominant liquidity layer for this niche, Pendle is strategically positioned to capture future Real-World Asset (RWA) rate swap volumes. While this "sector-leader" narrative is a compelling driver for analysts, it often overlooks the immediate discrepancy between a protocol's total addressable market and its current capital efficiency.

Valuation Through Two Lenses: MC/TVL and P/F

A data-driven view produces a more balanced conclusion.

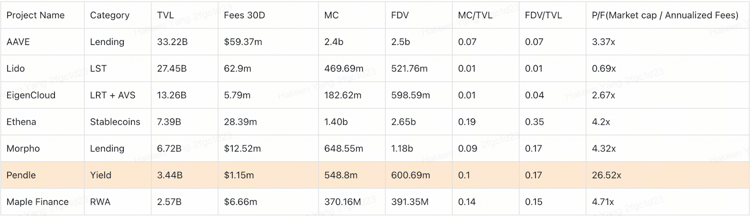

MC/TVL

With TVL around $3.44B and a market cap (MC) near $548.8M, Pendle’s MC/TVL falls in the 0.07–0.19 range. This ratio serves as a barometer for how much the market is willing to pay for every dollar of managed capital. In the DeFi hierarchy, high-innovation protocols typically command a premium, whereas "utilitarian" lending protocols like Aave often trade at lower multiples (approx. 0.07).

P/F (Price-to-Fees)

P/F highlights another dimension: how the market prices a protocol’s fee-generating capacity. Fees are not the same as net revenue, but they are still a practical proxy for monetization efficiency. Pendle stands at an elevated 26.52x. This indicates a significant "earning efficiency" deficit. Ethena, by comparison, has been cited at roughly 4.2x P/F with around 0.19 MC/TVL.

Overview of major DeFi products

Unbiased Judgment of Valuation of Pendle

To derive an objective valuation, Pendle must be viewed within the broader context of the DeFi landscape, where three specific truths become evident:

Systemic Valuation Compression: The DeFi sector at large is currently suffering from a valuation disconnect. The market frequently gravitates toward high-velocity "shiny" innovations while neglecting the compounding value of mature, foundational infrastructure like Aave or Morpho.

The Baked-In Premium: Based on its current P/F ratio, the market has already granted Pendle a substantial valuation premium. Maintaining an MC/TVL of 0.1 in the face of low value-capture capabilities suggests that aggressive future growth is already priced into the current token value.

Asset Stickiness and Value Leakage: The market has correctly identified that a significant portion of Pendle’s peak TVL was "mercenary capital" chasing airdrop incentives with low long-term stickiness. Furthermore, because the leverage loops (e.g., the "Mega Points" strategy) required external lending protocols to function, Pendle effectively outsourced the most lucrative part of the transaction—the lending fees—to third-party platforms.

The RWA Interest Rate: Trillion-Dollar Story, Thin-Margin Business

The transition toward on-chain RWA necessitates a rigorous re-evaluation of Pendle’s business model and revenue durability. As the crypto market matures, the "trillion-dollar" narrative of IRS must be reconciled with a fundamental market truth: the IRS sector is a high-notional, low-margin industry.

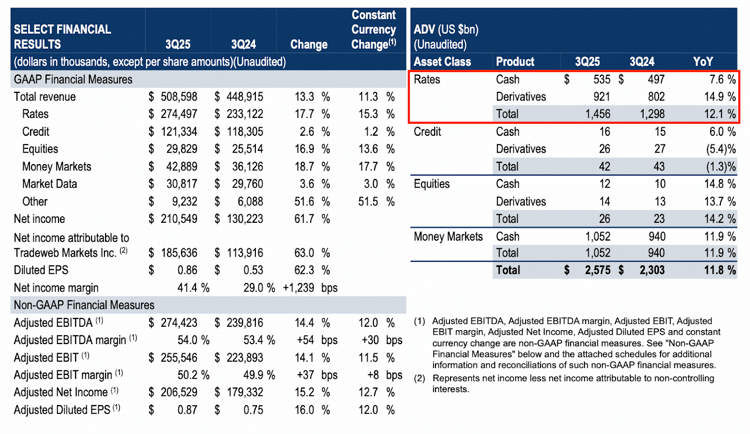

Tradeweb's Q3 Results

As a market leader commanding a 55% market share, Tradeweb’s Q3 2025 performance offers a critical baseline for institutional yield trading. In this period, the Average Daily Volume (ADV) for IRS reached $1.456T, contributing to an annualized volume exceeding $372T. While the "Rates" segment (comprising cash and derivatives) remains a revenue pillar—generating $274.5M, or 54% of total revenue—the unit economics are notably thin.

Every $1M in trading volume in the IRS market generates a mere $2.17 in revenue. For context, this is a fraction of the $28 in revenue generated per $1M in equity trading. This high-volume/low-margin profile is the hallmark of a mature, institutionalized financial market where competition and transparency compress spreads to their absolute limit.

In stark contrast, Pendle’s current monetization strategy appears remarkably efficient within the DeFi landscape. Its revenue is derived from two primary channels:

Yield Fees (YT Fees): The protocol extracts a 5% commission on all yields accrued by Yield Tokens (YT).

Swap Fees: Pendle collects maturity-scaled fees on Principal Token (PT) pairs. For example, a $10,000 trade in a USDT-PT sUSDe pool typically yields approximately $2.70 in fees.

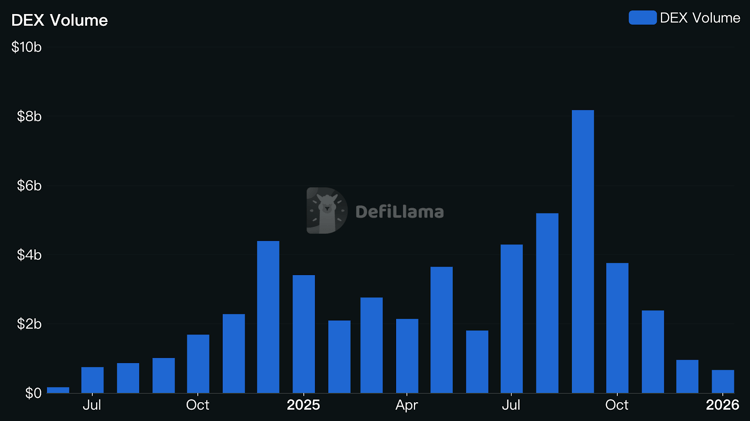

Data from September 2025 reveals that Pendle generated $6.09M in fees on $8.17B in volume. This translates to approximately $745.41 per $1M traded—a monetization rate around 340 times higher than its traditional counterparts. While the trading volume of Pendle continues declining after September 2025, revenue from such business model still relies heavily on its ability to retain high-quality TVL and sustain attractive, realizable yields in the underlying assets—because both YT fees and swap fees ultimately depend on persistent yield demand and active secondary-market trading.

Pendle's Trading Volume

Conclusion

The preceding analysis leads to a definitive conclusion regarding Pendle’s current market positioning and its long-term viability. While the protocol has successfully pioneered a new vertical, its current valuation rests on a precarious foundation of temporary incentives.

Pendle’s exponential TVL growth is largely an artifact of "point-farming" and recursive leverage rather than organic demand for interest rate hedging. This creates a veneer of success that we define as liquidity fragility. Because this capital is "mercenary" in nature—driven strictly by the pursuit of external airdrop rewards—it lacks fundamental stickiness. Once these incentive programs reach their inevitable conclusion, a massive contraction in AUM is expected. Furthermore, Pendle’s fee generation remains fundamentally decoupled from its TVL; without consistent, high-velocity trading volume, the protocol is left with an alarmingly high P/F ratio that current revenues cannot justify.

The Valuation Disconnect: Inefficient Value Accrual

From a vertical valuation standpoint, Pendle’s current revenue model exhibits significant inefficiencies when compared to its DeFi peers:

Aggressive Forward Pricing: The high MC/TVL ratio suggests that the market has already "priced to perfection," factoring in several years of optimistic growth and narrative dominance.

Diluted Value Capture: Despite managing billions in assets, the actual yield flowing back to $PENDLE holders and the protocol treasury is disproportionately low. In the hierarchy of DeFi value capture, Pendle currently functions as a high-overhead infrastructure layer rather than a high-margin cash flow engine.

Narrative of on-chain RWA : High Volume, Thin Margins

The core of the "bull case" for Pendle relies on the integration of the trillion-dollar TradFi IRS market. However, a deep dive into institutional finance reveals a sobering reality: IRS is a high-notional, low-margin business. In mature markets, the bargaining power of institutional players and the transparency of the product suite drive fees to the absolute minimum. Transitioning these swaps to a blockchain environment will not magically resolve these underlying profitability constraints. Even if Pendle achieves massive notional trading volume before September 2025, the actual fee capture in the future is likely to remain negligible due to shrinking trading volume after "Mega Points" era.

The Post Mega Points Era and the Boros Pivot

The "Mega Points" era provided Pendle with a historic bootstrapping opportunity, but it also created a deceptive growth profile dominated by impatient, short-term capital. The current high revenue efficiency is a localized anomaly—a byproduct of an immature market where retail participants are willing to pay a premium for levered exposure. As the crypto-financial landscape professionalizes, we anticipate a significant compression of revenue efficiency, ultimately aligning with the lean margins characteristic of traditional finance.

Pendle’s "grand narrative" currently faces a fundamental disconnect from its commercial reality. In a mature market, trillion-dollar platforms often struggle with unattractive business models due to institutional fee pressure. Therefore, maintaining a high valuation premium based solely on incentive-driven volume is unsustainable.

The protocol’s future now hinges on its ability to cultivate organic stickiness. The launch of Boros (formerly Pendle V3) represents a critical strategic pivot. By moving toward a more capital-efficient architecture for margin trading and genuine yield speculation, Pendle is attempting to transition away from the "mercenary capital" cycle. This evolution acknowledges the ultimate market axiom: "Capital never sleeps." Airdrop-driven liquidity can serve as a catalyst, but it can never function as a permanent anchor for valuation.

DeFi

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open