TxFlow: A Perp DEX Built Around Shared Liquidity

TxFlow is a community-owned financial Layer 1 whose first live Channel is a fully onchain central limit order book perp DEX, designed to make liquidity composable across perpetuals, spot, prediction markets, and future financial applications.

TxFlow is a community-owned financial Layer 1 whose first live Channel is a fully onchain central limit order book perp DEX, designed to make liquidity composable across perpetuals, spot, prediction markets, and future financial applications.

Why Another Perp DEX?

Perp DEX (Perpetual decentralized exchanges) has become one of crypto's strongest thesis. Hyperliquid set the pace as market leader, while newer venues such as Lighter, EdgeX, and Grvt compete on different parts of the product stacks, such trading fees, execution performance, or yield-bearing features.

The growth in the perp market did not remove core product tradeoff. Centralized exchanges still offer faster execution, deeper books, and familiar pro-trading interfaces. Perp DEXs offer self-custody, onchain settlement, and fewer custodial risks. The market has been trying to combine the best part of both, but most product designs still compromise on at least one dimension: liquidity fragmentation, high fees, weak collateral efficiency or offchain execution that reduces transparency.

TxFlow is attempting to fill the gap between high-performance perp trading and multi-application onchain finance. Its core premise is that a perp DEX should not be the end product of a chain, but a first channel on top of a shared liquidity layer that future trading applications can reuse. The central claim is: liquidity should become shared infrastructure across multiple financial applications, rather than a moat trapped inside one exchange.

Introducing TxFlow

TxFlow is an open Layer 1 blockchain. Its first application is TxFlow DEX, a central limit order book, or CLOB, exchange for perpetual and spot trading. A CLOB matches buyers and sellers by price-time priority, the same basic market structure used by centralized exchanges and traditional financial venues.

TxFlow's orders placement, cancellations, matches, liquidations, and settlement are all run onchain on the TxFlow L1. The chain is built around DAG-based parallel execution, a multi-threaded transaction pipeline, 250,000 transactions per second, and one-block finality.

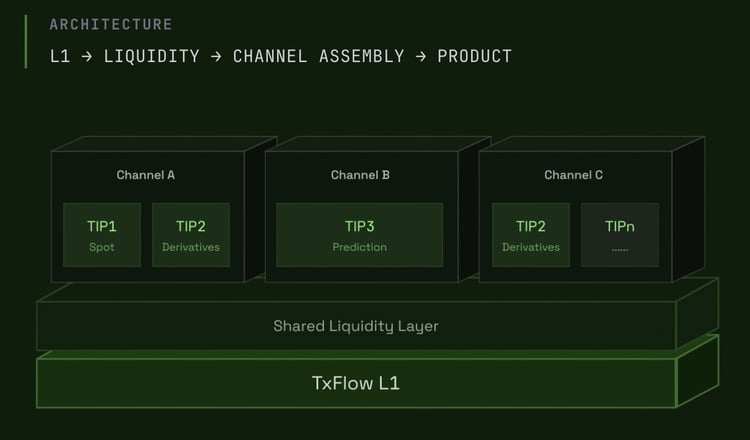

TxFlow is built for both traders and builders. Traders can have centralized exchange style execution without giving up self-cutody or onchain settlement, while builders can launch financial applications without rebuilding liquidity from zero. TxFlow calls these applications Channels. Each Channel can compose with TxFlow Improvement Proposal, or TIP, Liquidity Standards: TIP1 for spot, TIP2 for derivatives, TIP3 for prediction markets, and future TIP standards for additional products such as real-world assets or structured products.

Current Product

TxFlow’s current product mix is perps-first. The DEX offers 157 perps pairs alongside 9 spot pairs and over 7,000 outcome pairs, with coverage extending from major crypto assets into TradFi exposure, including precious metals, oil, and US stocks.

USDC is the core collateral asset for trading. Users can deposit USDC across multiple supported blockchain networks, trade through cross or isolated margin, and withdraw back to their own wallet. The current onboarding flow is designed to reduce friction: users can connect through an EVM wallet or email login.

No VC Funding

The project is positioned around no VC investor backing, with governance and ownership resting with the community. In a perp DEX market where many competitors are backed by large funds or exchange-linked investors, TxFlow uses community ownership as a core differentiator.

Why TxFlow Is Different

TxFlow’s differentiation starts below the exchange interface. Most perp DEXs compete as venues: deeper books, lower fees, more markets, better UX, or stronger incentives. TxFlow is competing as infrastructure. TxFlow DEX is the first channel on TxFlow L1, while the larger design is a shared financial layer where multiple applications can compose with the same liquidity, with prediction markets positioned as a future Channel.

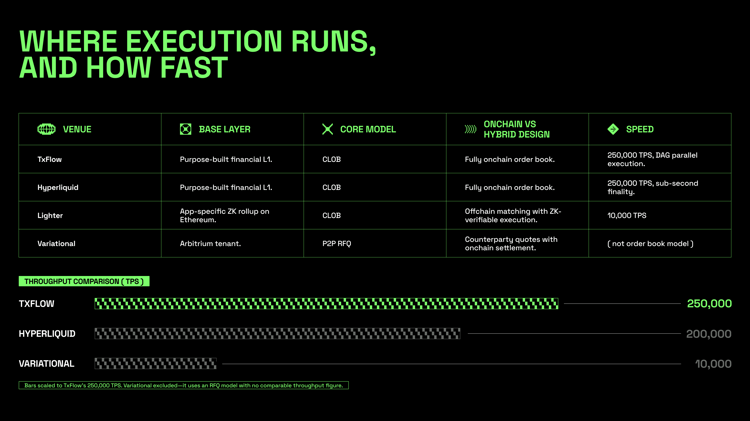

Purpose-Built Financial L1 With a Fully Onchain CLOB

Perp DEX execution quality starts at the infrastructure layer. The key distinction is whether the venue controls its own execution environment or operates as a tenant on another chain, rollup, or appchain.

Fully onchain order books make order entry, cancellation, matching, liquidation, and settlement part of the chain’s state transition. Hybrid systems move part of that flow offchain for speed, then settle or verify the result onchain. Some also use RFQ (request for quote) , which replaces continuous order-book depth with counterparty quotes.

TxFlow sits at the most infrastructure-native end of that spectrum. It is a purpose-built financial L1, and TxFlow DEX is its first Channel. A CLOB matches bids and asks by price-time priority. On TxFlow, that market process is designed to run directly on the L1, supported by DAG-based parallel execution, a multi-threaded pipeline, 250,000 TPS, and one-block finality.

The fast speed on chain level does not make TxFlow the best execution on the market on day one. Execution quality in practice also depends on liquidity depth, slippage, and fees, which will be discussed in the later section.

Capital Efficiency at the Chain Layer

TxFlow approaches capital efficiency at the network, and the distinction matters because at the account layer TxFlow is conventional. Collateral is USDC only, and margin modes are cross and isolated, not the unified portfolio margin that defines the account-level efficiency leaders. Grvt's unified margin system treats all trader collateral as one pool, recognizes natural hedges, and routes idle margin into onchain yield to pay up to 11% annual percentage yield (APY). TxFlow does not pay yield on idle margin; its yield path is opt-in vault deposits, and Protocol Vault deposits are not yet open to the community.

The edge TxFlow claims is the inefficiency one layer up: capital fragmented across applications. On a vertically integrated chain, a prediction market cannot draw on the liquidity backing a perpetuals book. On TxFlow, a Channel deploying the prediction-market module accesses the same liquidity layer powering the derivatives Channel. Capital that would otherwise be duplicated across separate venues is pooled once at the chain level. The proposition is that liquidity compounds across Channels rather than fragmenting.

Source: TxFlow

The two approaches are complementary. A Channel built on TxFlow could implement unified margin and yield-bearing collateral internally while still inheriting chain-level shared liquidity.

Multi-Asset Finance, Not Just More Markets

The perp DEX market is already expanding beyond BTC, ETH, and altcoin contracts. Competitors are adding equities, commodities, indices, prediction markets, and RWAs. TxFlow is aligned with that direction, but market count alone is not the strongest claim. Listing more pairs is easy to market and difficult to sustain without liquidity.

TxFlow’s stronger claim is that new product categories can become Channels on the same financial L1. Perps, spot, prediction markets, RWAs, and structured products can share common liquidity rather than source liquidity individually.

How TxFlow Works

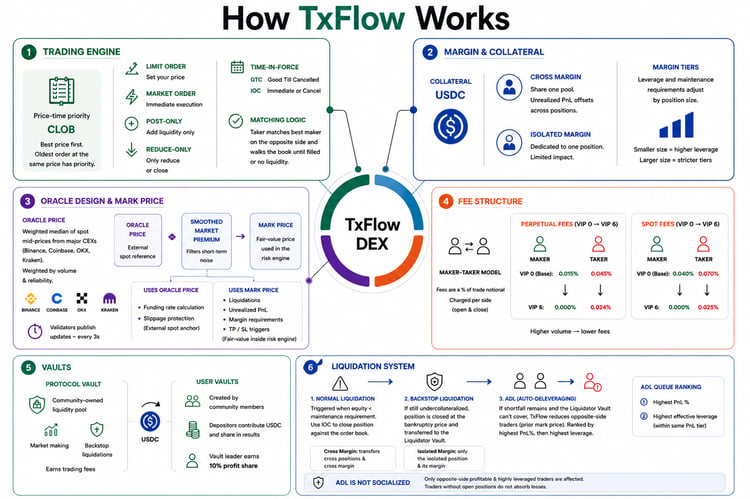

TxFlow’s product design is built around a fully onchain central limit order book, USDC collateral, a dual-price oracle system, tiered margin controls, and a community-facing vault layer.

TxFlow at a Glance

Trading Engine

TxFlow DEX uses a price-time priority CLOB. The best price executes first, and the oldest order at the same price has priority. When a taker order arrives, the engine matches it against the best maker order on the opposite side and executes at the maker’s price. If the order still has remaining size, the engine continues through the book until the order is filled or no crossing liquidity remains.

This gives TxFlow a market structure closer to centralized exchanges than AMM-based exchange. Traders can use limit orders for price control, market orders for immediate execution, post-only orders to ensure they add liquidity, and reduce-only orders to avoid increasing or flipping exposure when closing a position. Time-in-force controls include GTC orders, which remain active until expiration or cancellation, and IOC orders, which execute immediately against available liquidity and cancel the unfilled remainder.

Margin and Collateral

USDC is the sole collateral asset for TxFlow perpetual positions. Traders can choose cross margin or isolated margin. Cross margin lets all cross positions share one collateral pool, allowing unrealized PnL from one position to offset losses in another. Isolated margin dedicates collateral to one position, limiting liquidation impact but reducing capital efficiency.

Margin tiers define how leverage and maintenance requirements change with position size. Smaller positions can access higher leverage and lower maintenance margin rates. Larger positions move into stricter tiers, reducing maximum leverage and raising maintenance requirements. This reduces concentration risk for both traders and the platform.

Oracle Design and Mark Price

TxFlow separates oracle price from mark price. The oracle price is an external reference price, while the mark price is the fair-value price used inside the risk engine. This separation is important because perp markets need an independent spot reference for funding and slippage protection, but they also need a fair-value price that reflects the venue’s own order-book.

The oracle price is calculated as a weighted median of spot mid-prices from major centralized exchanges, including Binance, Coinbase, OKX, and Kraken. The prices are weighted by exchange trading volume and reliability, and validators publish updates roughly every three seconds. A weighted median is more resistant to outliers than a simple average, which helps reduce manipulation risk from one venue or one bad data point.

The mark price is Txflow's fair-value estimate of the perpetual contract. It is derived from the oracle price plus a smoothed market premium that filters out short-term noise.

The two prices serve different functions. Funding-rate calculation and slippage protection use the oracle price because those processes need an external spot anchor. Liquidations, unrealized PnL, margin requirements, and take-profit or stop-loss triggers use the mark price because they need a fair-value estimate that aligns with the platform’s liquidation logic.

Fee Structure

TxFlow uses a maker-taker fee model across perpetual and spot markets. Fees are charged as a percentage of trade notional and deducted immediately when an order executes. They apply per side, meaning opening and closing a position each incur a separate fee.

The base perpetual fee is 0.015% maker and 0.045% taker at VIP 0. Spot fees are higher at the base tier, starting at 0.040% maker and 0.070% taker. TxFlow now uses a volume-based VIP program instead of a flat-only model.

The fee curve is designed to reward active traders without making the base schedule difficult to understand. At the lowest tier, TxFlow’s perp fees match the common CLOB perp structure of lower maker fees and higher taker fees. At higher tiers, maker fees fall to zero and taker fees compress meaningfully, reaching 0.024% for perps and 0.025% for spot at VIP 6.

Vaults

TxFlow has two vault categories: the Protocol Vault and User Vaults. The Protocol Vault is the community-owned liquidity pool. It performs market making and backstop liquidations, earning trading fees.

User Vaults are created by community members. Depositors contribute USDC and share in the vault’s trading results. The vault leader receives a 10% profit share for managing the strategy. Vault strategies can vary, including directional or arbitrage approaches, so the risk profile is less standardized than the Protocol Vault.

Liquidation System

TxFlow liquidates positions when equity falls below maintenance requirements. In cross margin, liquidation is triggered when account equity across cross positions falls below total maintenance margin. In isolated margin, liquidation is triggered when the position’s dedicated margin falls below that position’s maintenance requirement.

If the position remains undercollateralized after the IOC attempt, TxFlow moves to backstop liquidation. The remaining position is closed at the bankruptcy price and transferred to the Liquidator Vault. In cross margin, the backstop can transfer cross positions and cross margin. In isolated margin, only the isolated position and its margin are affected.

ADL, or auto-deleveraging, is the final solvency layer. It only activates if the account or isolated position value becomes negative and the Liquidator Vault cannot cover the shortfall. At that point, TxFlow closes traders on the opposite side of the underwater position against it at the prior mark price. The purpose is to prevent platform bad debt after normal liquidation and backstop liquidation has failed.

ADL is not socialized across all users. Traders without open positions do not absorb losses. The ADL queue ranks opposite-side traders by profitability and leverage: first by highest PnL percentage, then by highest effective leverage within the same PnL tier. This means the most profitable and most leveraged traders on the opposite side are first in line to be reduced during an extreme market event.

Competitive Landscape

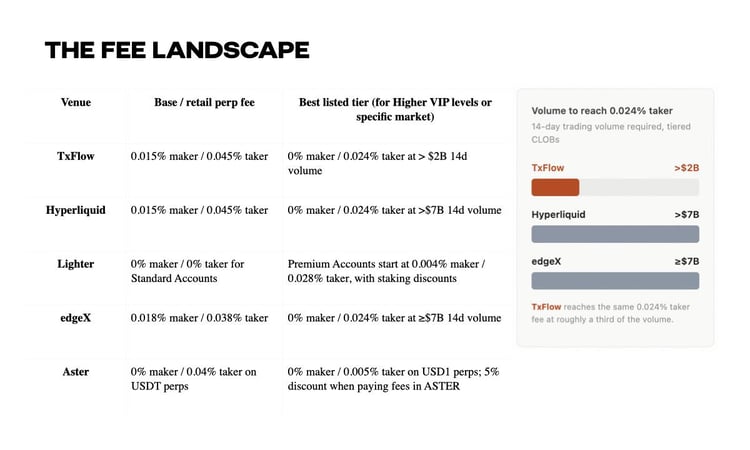

Fees

TxFlow’s base 0.015% maker and 0.045% taker fees for VIP 0 level are competitive but not market-leading. For example, Hyperliquid has the same base perp fee tier before discounts or staking discounts. Lighter charges zero maker and taker fees for standard accounts, Aster is cheaper on maker fees and USD1 markets.

Execution Cost

Execution cost is the real cost of getting filled. Fee tables only show one component. For marketable orders, the more useful measure is: Total execution cost = taker fee + buy-side slippage.

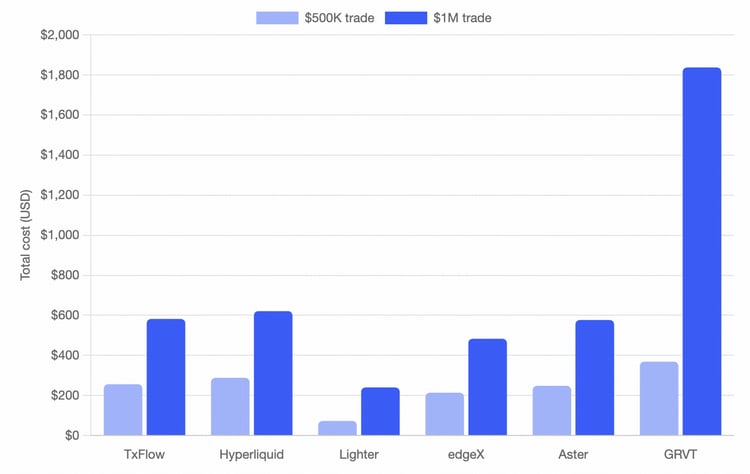

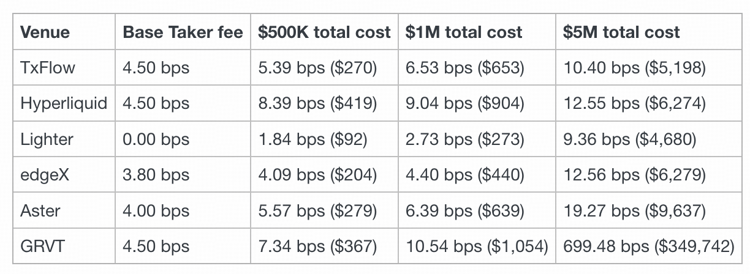

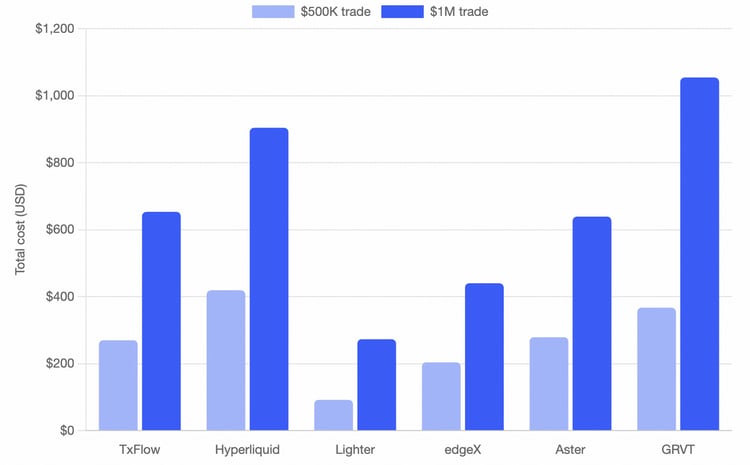

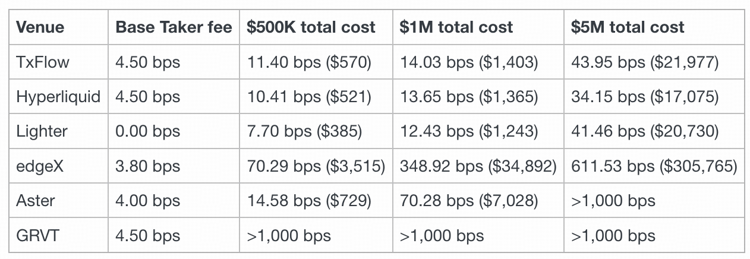

The table below compares one-way marketable buy execution across BTC, ETH, and XAU for leading perp DEX on the market. Figures are shown in basis points, with estimated dollar cost in parentheses.

BTC

ETH

TxFlow is not the cheapest venue on headline taker fees, and Lighter’s zero-fee standard account gives it a clear advantage in smaller BTC and ETH clips. But once slippage is included, TxFlow sits in the competitive range for major markets. On BTC, its $5 million total cost is lower than Hyperliquid, edgeX, Aster, and GRVT. On ETH, TxFlow is close to the best non-zero-fee venues at small sizes and remains competitive at $5 million.

XAU

XAU is the more important test because non-crypto markets usually have thinner onchain depth. In this sample, TxFlow’s XAU execution cost is close to Hyperliquid and Lighter through $1 million, and remains within the same band at $5 million. That is the stronger point than the fee schedule itself: TxFlow’s order book is not only functioning on crypto majors; it is showing usable depth on a TradFi-style market where many venues become expensive once order size increases.

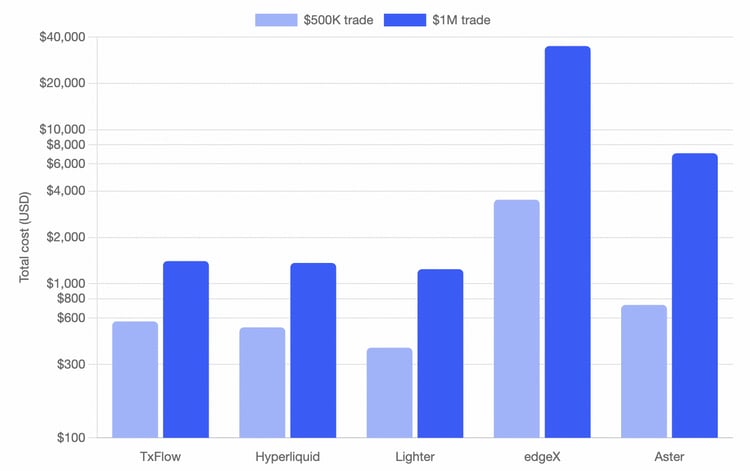

Liquidity and Slippage

Liquidity is the main constraint for any order-book perp DEX. Fees define the visible cost of trading, but depth and slippage determine whether a trader can enter size without moving the book. A low-fee venue can still be expensive if liquidity is thin, while a higher-fee venue can be competitive if the order book absorbs flow efficiently. This section compares TxFlow against five active perp DEX competitors: Hyperliquid, Lighter, edgeX, Aster, and GRVT.

TxFlow’s current depth profile is more differentiated across metals and selected high-volume altcoins than across crypto majors alone. On a combined bid-ask basis within the 1% book, TxFlow ranks first in the measured venue set for XAU, XAG, DOGE, XRP, SUI, and second for SOL and HYPE.

Txflow depth & slippage

Slippage remains size-dependent. At $500,000 and $1 million clips, TxFlow’s slippage is generally contained across its stronger markets. At $5 million, costs rise meaningfully in smaller or higher-beta assets, which is expected as trades move beyond top-of-book liquidity into the tail of the order book.

Risk Consideration

TxFlow’s risk surface follows its architecture. The protocol reduces offchain execution opacity by running order placement, cancellations, matching, liquidations, and settlement onchain, but that also makes the L1 trading engine itself the critical trust surface. The relevant security risk is not only smart-contract risk facing every perp DEX, matching logic, margin checks, liquidation logic all need to remain correct under live market load.

Oracle risk is not unique to TxFlow, but it becomes more important as the product surface expands beyond crypto majors. Like other perp venues, TxFlow uses an external oracle reference and an internal mark price for risk-engine functions. As TxFlow lists metals, oil, stocks, and other non-crypto markets, reference-market quality, update timing, weekend liquidity becomes more important risk variables.

Liquidation risk also remains central. TxFlow uses cross and isolated margin, margin tiers, backstop liquidation through the Liquidator Vault, and ADL as the final solvency layer. These mechanisms reduce the chance of broad socialized losses, but they do not eliminate forced deleveraging. In extreme market conditions, profitable and highly leveraged traders on the opposite side of an underwater position can still be reduced if normal liquidation and backstop liquidity fail.

Finally, TxFlow is also newer than the largest perp DEX venues, so execution quality, uptime, oracle reliability, and liquidation performance all need to be tested through high-volume sessions and market stress.

Closing View

TxFlow’s strongest case is execution quality plus composability. The DEX is built on a fully onchain CLOB where orders, cancellations, matches, and liquidations settle onchain, while the L1 targets 250,000 TPS through DAG-based parallel execution, a multi-threaded pipeline, and one-block finality. That design gives TxFlow the infrastructure needed to support order-book trading without pushing the core trading lifecycle into an offchain matcher.

The practical result is visible in execution cost. TxFlow’s fully onchain CLOB already shows competitive all-in execution on major crypto and tradfi pairs. The depth profile is also strongest beyond the narrow BTC and ETH benchmark. In the measured venue sample, TxFlow has the deepest ask-side book within the tested band for XAU, XAG, DOGE, XRP, SUI, and ranks second for SOL and HYPE.

That is the closing case for TxFlow: a new perp DEX with measurable depth in key crypto, altcoin, and commodity markets; competitive all-in transaction cost once slippage is included; and a standards layer designed to make liquidity reusable across financial applications. If that depth persists through volatility, TxFlow’s first DEX becomes more than a trading venue. It becomes the first production Channel of a shared-liquidity financial L1.

DEX

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open