TI - November Major Asset Class Outlook

In the fourth quarter of 2021, investors will focus on the attitude of policy makers. Judging from the recent statements of the People's Bank of China, China goverment will still adhere to a normal monetary policy, and it is difficult for the equity market to undergo phased changes during the year. At the same time,Fed has already stated at the FOMC meeting in November that it will start Taper. Nasdaq has taken on a lot of pressure on expectations in the past few months. Looking ahead to next year, the winter of highly valued assets may be on the way.

In the fourth quarter of 2021, investors will focus on the attitude of policy makers. Judging from the recent statements of the People's Bank of China, China goverment will still adhere to a normal monetary policy, and it is difficult for the equity market to undergo phased changes during the year. At the same time,Fed has already stated at the FOMC meeting in November that it will start Taper. Nasdaq has taken on a lot of pressure on expectations in the past few months. Looking ahead to next year, the winter of highly valued assets may be on the way.

Market Backdrop

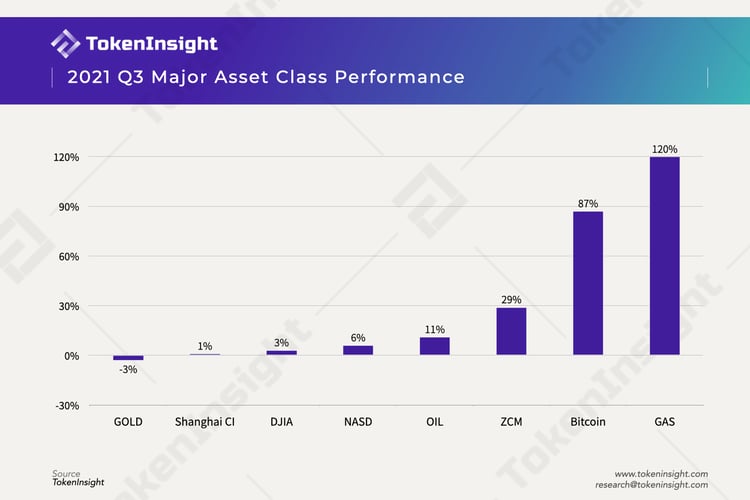

As we predicted last week, commodities continued to surge in November. First of all, from the perspective of earnings performance, the performance of energy commodities such as crude oil and natural gas has been surprising, and their prices have reached historical highs. At the same time, gold has once again become the worst-performing asset category. In the context of tightening liquidity, the cumulative decline in US stocks has not happened. Due to the lack of corresponding stimulus policies, China's economic activity has also fallen to a certain extent. The U.S. 10 years treasury yield exceeded 1.7%. The capital market has shown a performance rotation.

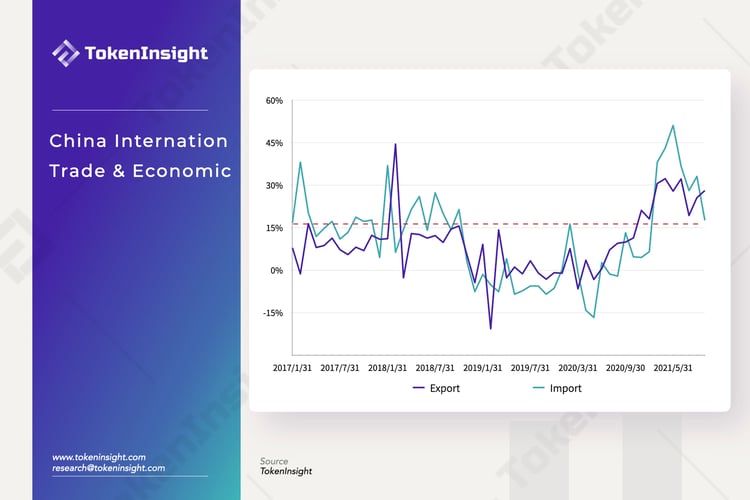

Monetary policy is converting and domestic economic downturn is confirmed. Judging From the global market: After two more hawkish interest rate meetings in June and September, the tone of the Fed's November interest rate meeting was more balanced. The implementation of reduced bond purchases means that the Fed has officially begun to withdraw from the easing monetary policy. Focusing on the domestic market: In the case of insufficient global production capacity, exports still show strong momentum; in September, the export growth rate soared to 28.1%, and the monthly export value broke 300 billion US dollars to set a new record. In 2018, the significant weakening of the import margin reflects the insufficient endogenous power of the economy, and imports from major countries have fallen sharply. Due to the stricter restrictions on electricity and production in Q4, it will have a greater disturbance to the production of enterprises.

Asset Class Analyze

Bond Market

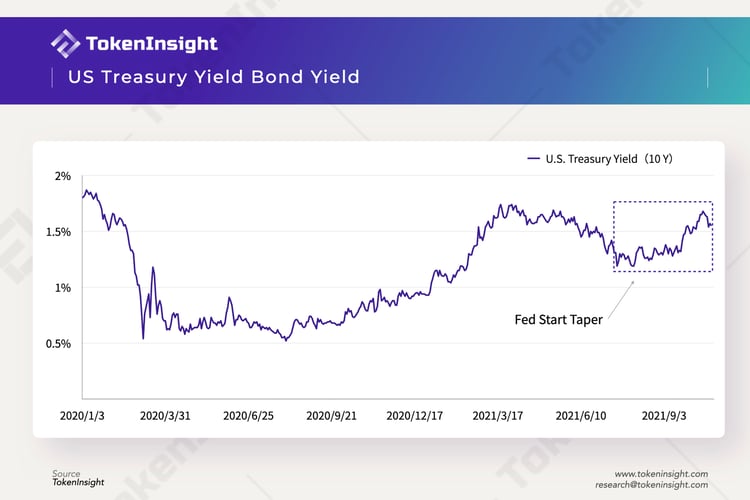

Overseas Bond Market: The Fed starts to taper as expected in November. Combined with the interest term structure, Taper has been fully priced by investors, and the key factors affecting treasury yield have been transformed into interest rate hike expectations, inflation risks, and tightening policies of other central banks. From 2021 to the first half of 2022, under the multiple effects of interest rate hike expectations and liquidity contraction, the rate of increase in interest rates may exceed investor expectations.

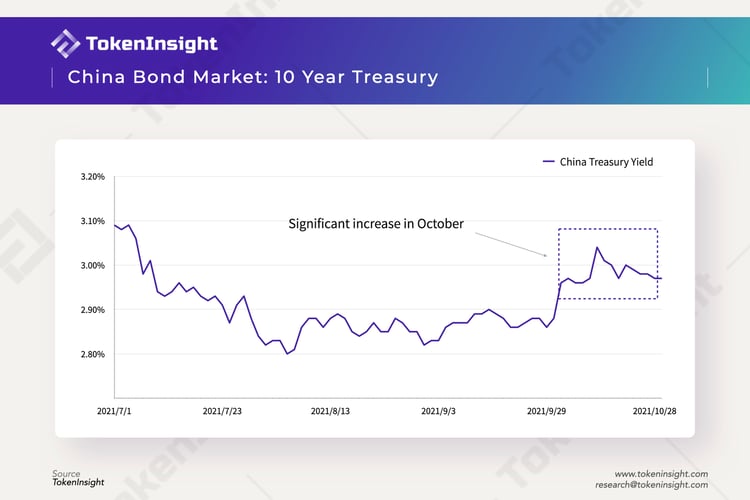

Domestic Bond Market: Since October, the bond market has broken the downward trend of the past two months and started a round of rapid adjustment. The main reason for this comes from the government’s easing expectations for real estate. At the same time, Policymakers explained at the financial statistics press conference that there will be no interest rate cuts expected the rest of the year which means there is limited room for monetary policy in the future. Generally speaking, the probability that the medium-term economy will fall below the potential growth rate is relatively high, which determines that the adjustment of the bond market is not a trend.

Equity Market

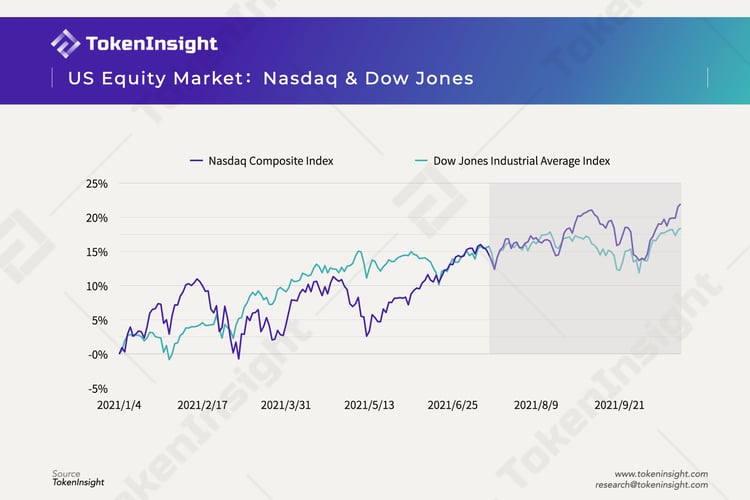

DM Equity Markets: In September, Treasury yield and the Dollar Index continued the pattern of double-rising. The driving force behind it came from the strengthening of the Fed’s tightening expectations. The difference from August is that equitys' earnings are no longer strong, showing the biggest monthly decline since the second quarter of last year. When the double-tight combination of treasury yield and dollar index shifts from economic recovery to tightening of liquidity, it is very detrimental to risky assets. Therefore, the probability of a continued decline inequity in the fourth quarter is greater. Make a new record after minor adjustments.

Domestic Equity Market: Mainly investors believed that China's economy will rotate from stagflation to the recession quadrant. The stock market seems to have begun trading the logic of "recession", and thematic opportunities are more focused, and it is necessary to use a medium-term vision to deal with short-term confusion. On October 23, 2021, the Thirty-first Meeting of the Standing Committee of the Thirteenth National People's Congress passed the "Decision on Authorizing the State Council to Launch Real Estate Tax Reform Pilot Work in Certain Regions." China's A-share listed companies began to disclose their results for the third quarter in October. With the clarification of the economic turning point, the overall profit decline is expected by investors. Specific observations: First, the market profit growth rate has begun to fall, the performance differentiation has intensified again, and the profit improvement has shrunk back to the top companies; second, commodities created resistance to the midstream and downstream performance, and corporate profits came to a fork. In the fourth quarter, the PPI still has the possibility of upward movement, which will further show its restraint on downstream demand.

Commodity Market

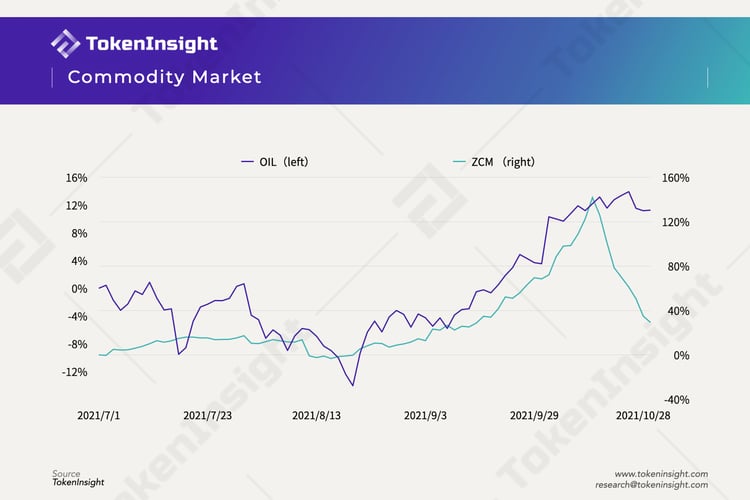

The Chinese government resolutely curbs the speculation of coal hoarding. Affected by this, thermal coal futures fell more than 30% from the high point this week, and domestic futures prices such as coke also fell more than 10%. In recent years, European governments have vigorously promoted the "dual carbon" policy of energy transition, which has boosted natural gas prices. Since August, the hurricane-driven supply contraction has pushed oil prices to rise. After October, global energy supply shortages have gradually become prominent. Prices of electricity and natural gas have been high. Crude oil prices have once again been the main driving force for this round of rising oil prices. Because of the general rise in energy prices。

Cryptocurrency Market: The cryptocurrency market showed strong profitability in the third quarter, and the current market is in a state of risk appetite differentiation: Bitcoin and Ethereum have experienced some signs of sideways at their historical highs after experiencing a renewed price hike. Meme and other altcoins have shown a strong upward trend, At the same time, the funding rate of perpetual contracts continues to rise and has returned to the level of May this year... Such a market situation is unstable, and it is expected that there will be a risk of increased volatility in the future.

Outlook

Summary: In the face of changes in macro factors, the overseas and domestic capital markets have undergone certain adjustments. In the fourth quarter of 2021, commodities are expected to continue to strengthen. Crude oil and natural gas may hit a record high. In contrast to the equity and bond markets, policymakers are more willing to tighten policies rather than relax. The adjustment of risky assets may not be over yet, if it is safe adequate margin could provide a good investment opportunity for China treasury bonds.

DeFi

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open