Circle After the Beat: from USDC Growth to Distribution Economics

Circle’s latest quarter offered further evidence that its earnings base is becoming more resilient than the broader crypto market. Yet while concerns around USDC scale have eased, a more important risk is emerging in the form of potential regulatory pressure on the company’s long-standing distribution arrangement with Coinbase.

Circle’s latest quarter offered further evidence that its earnings base is becoming more resilient than the broader crypto market. Yet while concerns around USDC scale have eased, a more important risk is emerging in the form of potential regulatory pressure on the company’s long-standing distribution arrangement with Coinbase.

Key Takeaways

- Circle’s Q4 beat reinforced that its earnings engine remains primarily reserve-income driven, with USDC scale more than offsetting the decline in reserve yield. More importantly, USDC supply has held up far better than in prior crypto downturns, suggesting Circle’s earnings base is becoming less sensitive to crypto price volatility.

- The investment debate is now shifting away from USDC scale and toward distribution economics. The main uncertainty is whether future U.S. regulatory interpretation could constrain how reserve income is shared with partners such as Coinbase, potentially pressuring Circle’s most important distribution channel.

- Circle is making progress in building payment and infrastructure revenue streams, but these remain secondary to the reserve-income model for now. As a result, the stock’s medium-term rerating still depends more on regulatory clarity and monetization structure than on diversification narrative alone.

Introduction

Beneath the headline revenue beat, Circle’s earnings base remains fundamentally reserve-driven. What matters more for the investment case is not the quarter’s upside surprise itself, but whether the three key variables behind the model remain intact: reserve yield, USDC scale, and distribution economics.

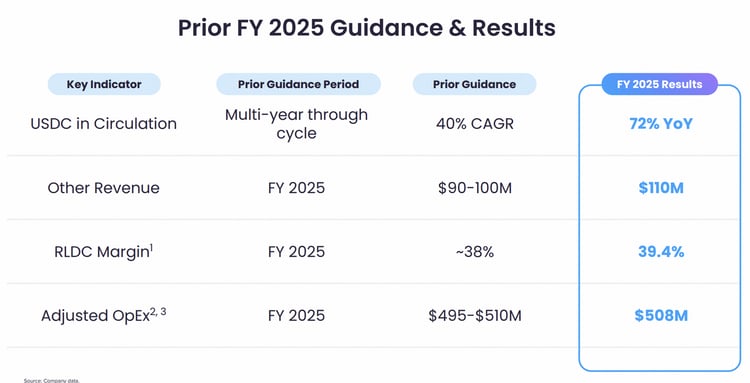

On the first two, the picture was constructive. Circle reported Q4 2025 total revenue and reserve income of $770 million and ended the year with $75.3 billion of USDC in circulation, up 72% year over year. The market responded immediately to the beat, but the more important takeaway is that Circle’s reserve-income engine continues to hold up even as crypto prices weakened materially.

The debate now shifts away from whether USDC can keep its scale through a weaker crypto tape, and toward whether Circle can preserve the economics of distributing that scale.

Q4 Snapshot and the Structure of Circle’s Earnings Model

Circle’s Q4 results reinforced the extent to which the business still depends on reserve income. The company generated $733 million of reserve income in the quarter, up 69% year over year, despite a 68 basis point decline in its reserve return rate. In other words, the expansion in average USDC in circulation more than offset the decline in the yield earned on reserves.

At the same time, total distribution, transaction, and other costs rose to $461 million, up 52% year over year, underscoring that USDC growth still relies heavily on third-party distribution. This remains a critical point for valuation. Circle’s earnings model is best understood as a function of three variables: the level of short-term rates, the stock of USDC in circulation, and the terms on which reserve economics are shared across distribution channels.

Circle is attempting to broaden the model beyond reserve monetization. Full-year 2025 other revenue reached $110 million, and management guided to $150 million to $170 million for 2026. That supports the strategic narrative around payments infrastructure, treasury connectivity, and developer tooling. Still, non-reserve revenue remains small relative to the company’s overall earnings base, so the investment case continues to be anchored primarily in reserve income rather than in application-layer monetization.

USDC Scale Has Become More Resilient to Crypto Market Weakness

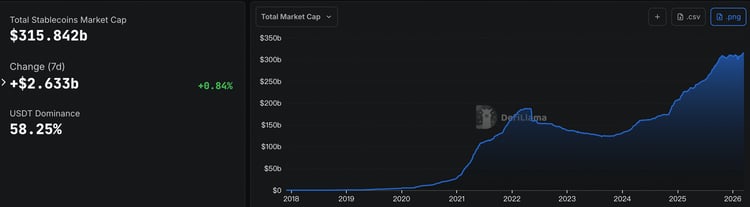

One of the more important developments in this cycle is that stablecoin supply has held up materially better than in previous crypto drawdowns. Total stablecoin market capitalization remains near record levels at roughly $315 billion according to DefiLlama, even after a sharp correction in broader crypto prices. That is a notable departure from prior bear-market episodes, when large crypto drawdowns were more often accompanied by visible stablecoin contraction, disorderly depegging, or capital flight from the ecosystem.

Source:DefiLlama (17/03/2026)

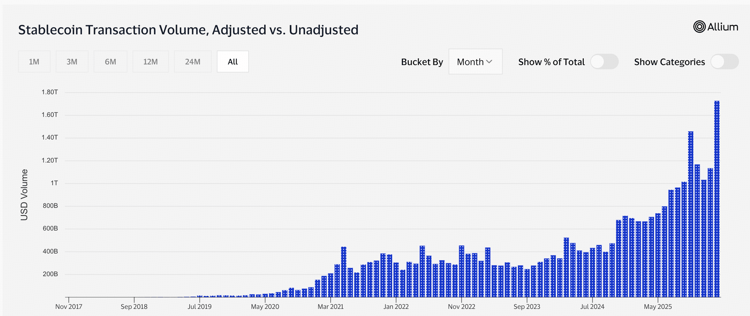

The implication for Circle is straightforward. If stablecoin balances are becoming less cyclical than the underlying prices of crypto assets, then the reserve base that supports Circle’s earnings is also becoming more durable. This does not mean stablecoins are fully detached from crypto market conditions, but it does suggest that the relationship has weakened meaningfully as the category has matured. Stablecoins are increasingly used not only as trading collateral, but also in cross-border settlement, treasury operations, and onchain payments. Visa’s onchain analytics dashboard, while methodology-dependent, also points to continued strength in adjusted stablecoin activity and supply metrics, consistent with a broader pattern of resilient usage.

Stablecoin transaction volume, adjusting for inorganic activity from bots and other artificially inflationary practices. Source: https://visaonchainanalytics.com/transactions

This matters for the stock. Circle’s equity still tends to trade like a high-beta crypto proxy, yet the underlying economics of the business are beginning to look less tied to spot crypto price action than in prior cycles. If stablecoin adoption continues to deepen outside purely speculative use cases, that gap between business fundamentals and stock behavior may narrow over time.

The Real Swing Factor Is Distribution Economics

The most important uncertainty for Circle now lies in distribution economics rather than in USDC scale itself. Specifically, the emerging question is whether U.S. regulators will take a restrictive view of commercial arrangements in which reserve economics are shared with distribution partners that, in turn, offer rewards tied to stablecoin balances.

That issue has come into focus through the OCC’s proposed rulemaking under the GENIUS Act. The proposal is not yet final, but outside legal analysis has highlighted that the OCC’s draft framework could create a rebuttable presumption against certain affiliate and third-party arrangements that economically resemble prohibited interest or yield payments to stablecoin holders. In practical terms, this raises the possibility that some exchange-based rewards structures could face heightened scrutiny if regulators conclude that issuer reserve income is being passed through indirectly to end users.

This is particularly relevant for Circle because Coinbase remains a central distribution partner for USDC. Coinbase has disclosed that, under its updated arrangement with Circle, it participates in the economics of the reserves backing stablecoins in circulation both on and off platform, and that it pays rewards to certain customers who hold USDC where permitted. That makes the partnership strategically valuable, but also places it closer to the area where future regulatory interpretation could matter most.

The key investment point is not that the Circle-Coinbase structure is already impaired. It is that the regulatory perimeter around this model has become less certain. If final rules ultimately constrain how reserve income can be shared with intermediaries that use those economics to fund user rewards, then Circle could face pressure on the most important part of its current go-to-market model. For a business still heavily dependent on exchange-led distribution, that would directly affect margins, growth efficiency, and the monetization of incremental USDC supply.

Bottom Line

Circle’s Q4 results strengthened confidence in two parts of the model. Reserve-driven earnings remain intact, and USDC scale appears materially more resilient to crypto market weakness than in earlier cycles. Those are important positives.

The main open question now is distribution economics. Until the OCC rulemaking is finalized and the treatment of third-party reward structures becomes clearer, the Circle-Coinbase arrangement remains the most important swing factor in Circle’s medium-term earnings profile. In that sense, the investment debate has moved on from whether Circle can grow, and toward how much of that growth it will ultimately be allowed to keep.

Circle

In This Article

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open