Liquidity vs. the Four-Year Cycle: Bitcoin Outlook for 2026

Bitcoin’s four-year halving cycle has guided market expectations for over a decade—but 2025 challenged the “post-halving bull year” rule. While Bitcoin still peaked in late 2025, the year ended negative, suggesting the cycle is shifting from a mechanical law into a behavioral framework. In 2026, institutional demand and macro liquidity may matter more than folklore.

Bitcoin’s four-year halving cycle has guided market expectations for over a decade—but 2025 challenged the “post-halving bull year” rule. While Bitcoin still peaked in late 2025, the year ended negative, suggesting the cycle is shifting from a mechanical law into a behavioral framework. In 2026, institutional demand and macro liquidity may matter more than folklore.

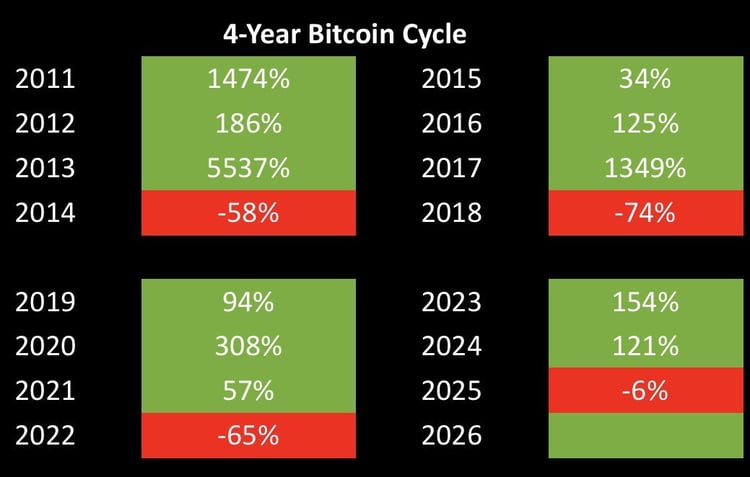

For over a decade, Bitcoin investors lived by a predictable "four-year clock" dictated by the halving—an event where the reward for mining new blocks is cut in half. Historically, this supply shock acted as a catalyst for a massive bull run in the following year (the "post-halving year"), followed by a painful "crypto winter." We saw this play out with clinical precision in 2012, 2016, and 2020. In each instance, Bitcoin reached dizzying heights—peaking at roughly $1,150 in 2013, $20,000 in 2017, and $69,000 in 2021—only to suffer dramatic drawdowns of 58% to 74% in the years that followed.

However, 2025 has rewritten the playbook, proving that while Bitcoin still follows a rhythmic pulse, its internal "biological" clock is changing.

Source: Simon Dixon https://x.com/SimonDixonTwitt

Bitcoin’s Four-Year Cycle: Still a Framework, No Longer a “Law”

In many ways, 2025 was the year the "Four-Year Law" was both broken and validated. On one hand, the traditional expectation of a massive, green annual return for the post-halving year failed to materialize; Bitcoin ended the year with a -6% return, despite reaching a new all-time high of $126,000 in October. This marked the first time in history that a post-halving year delivered a negative annual performance.

In other words, the cycle looked “broken” if you focus on calendar-year performance, yet it still “echoed” history if you focus on chronology: the market still topped late in the cycle window, but without the classic blow-off and without a strong year-end bid. That combination matters, because it suggests the halving narrative may be shifting from a deterministic price path into something closer to a behavioral framework—one that influences positioning and expectations, but competes with a much larger set of macro and structural drivers.

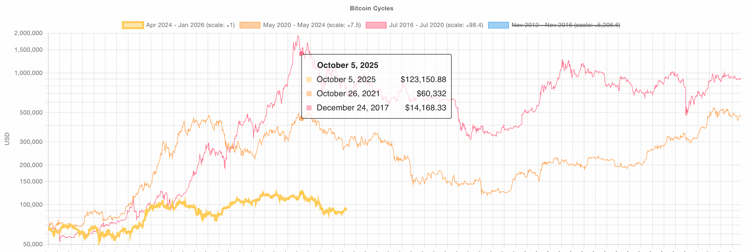

Bitcoin Top in Every Q4 of Post-halving Year(with different scales)

Why Halvings Matter Less Mechanically But More Narratively

There are sound reasons the halving’s mechanical impact has weakened over time. By the 2024 halving, close to 94% of total BTC supply had already been mined, and the event reduced Bitcoin’s annualized supply inflation from roughly ~1.7% to ~0.85%—still meaningful, but no longer the kind of supply shock that can dominate market structure on its own. As Bitcoin matures, the marginal reduction in new issuance becomes smaller relative to existing circulating stock, and therefore less capable—by itself—of overwhelming demand fluctuations.

At the same time, the demand side has changed. Regulated access points—especially spot Bitcoin ETFs—have made it easier for traditional allocators to express Bitcoin exposure without building crypto-native infrastructure, creating a steadier (and often less reflexive) source of demand than prior retail-driven cycles. This institutionalization does not eliminate volatility, but it can dampen the “all-or-nothing” liquidity regime that previously produced extreme boom-and-bust arcs.

Still, dismissing the four-year cycle entirely may be premature. Bitcoin has no cash flows, so price is unusually sensitive to expectations and narrative reinforcement. When enough market participants internalize a pattern, their behavior (de-risking into late-cycle strength, demanding higher risk premia after peaks, front-running distribution windows) can partially self-fulfill—even if the original supply catalyst is weaker.

A reasonable interpretation of this cycle, then, is that experienced holders began distributing earlier and more continuously, while newer “structural” bidders (ETFs, corporate allocators, multi-asset portfolios) absorbed that supply with less emotional urgency. The result can be a market that still respects late-cycle timing, but expresses it through choppier price action, weaker year-end closes, and less obvious mania.

2026: The Cycle Likely Persists—In a More Moderate Form

Going into 2026, the most plausible base case is not that the cycle disappears, but that it becomes less extreme. Investors who have lived through multiple cycles still tends to anchor to the four-year framework and may treat 2026 as a “traditionally difficult” year in the cycle calendar. Meanwhile, traditional financial institutions generally do not need the cycle to justify holding Bitcoin: they are more likely to size it as a long-duration hedge against monetary debasement risk or as a small strategic diversifier within multi-asset portfolios. Those objectives inherently de-emphasize short-term drawdowns and can provide a more consistent bid during periods when crypto-native participants de-risk.

That sets up 2026 as a tug-of-war: distribution pressure from long-term holders versus absorption from structurally stickier capital. If this balance holds, the market can still experience drawdowns and volatility, but the probability of a “clean” multi-year capitulation path may be lower than in earlier eras—especially if institutional flows remain positive and macro liquidity avoids a severe shock.

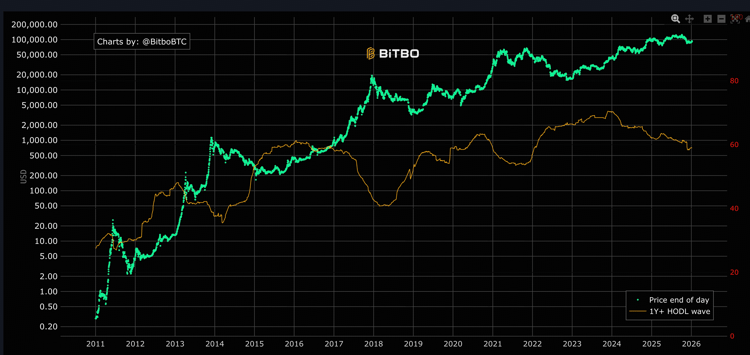

Long-term Holders Distributing Coin

The Macro Constraint: Liquidity Is Fragmented, Not Abundantly Easing

Even if the internal crypto supply-demand picture becomes more resilient, Bitcoin remains highly sensitive to global liquidity conditions. Lyn Alden’s research finds Bitcoin moves in the direction of global liquidity 83% of the time over rolling 12-month windows—higher than other major asset classes—making it an unusually direct liquidity barometer.

That matters because the macro setup entering 2026 looks more like tactical stabilization than a return to the ultra-easy post-2020 regime.

In the U.S., the Federal Reserve has ended balance-sheet runoff (QT) effective December 1, 2025, shifting to rolling over principal payments and reinvesting agency MBS principal into Treasury bills. Shortly after, it announced “reserve management purchases” of short-dated Treasury bills, with purchases amounting to $40 billion in the first month (with the pace dependent on market conditions). Importantly, Fed communication has framed this as an operational measure to maintain ample reserves, not a broad return to QE. The balance sheet itself is indeed around the mid-$6T range, consistent with the idea that QT has reduced assets materially from pandemic highs.

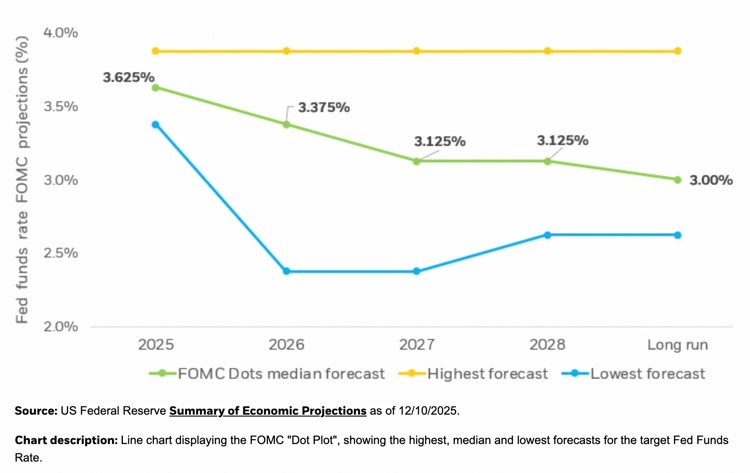

At the policy-rate level, the Fed ended 2025 with the target range at 3.50%–3.75%, and its December 2025 projections imply only modest additional easing. This is crucial: markets can rally on the end of tightening, but sustained “easy-money” tailwinds typically require a deeper easing cycle or a more aggressive balance-sheet expansion than what is currently signaled.

Source: tradingeconomics

Source: BlackRock

Outside the U.S., the picture is arguably tighter. The ECB has already discontinued APP reinvestments (since July 2023), and PEPP reinvestments ended at the end of 2024—both of which mechanically support ongoing balance-sheet shrinkage. In the UK, the Bank of England has continued its QT program, with the MPC voting to reduce gilt holdings by £70 billion over the October 2025–September 2026 period.

Japan is the potential swing factor for global risk liquidity. The Bank of Japan raised its policy rate to 0.75% on December 19, 2025, the highest in roughly three decades, reinforcing the message that Japan is no longer an unlimited source of ultra-cheap funding. A sustained tightening bias can accelerate the unwind of yen-funded carry trades during stress regimes, transmitting tighter financial conditions into global assets—including crypto—precisely when investors assume “liquidity is improving.”

Conclusion

Putting these pieces together, 2026 is best framed as a year where cycle expectations, structural adoption, and macro liquidity interact in a less synchronized way than in prior cycles. The halving still matters as a coordination device for narratives and positioning, but its direct supply-shock power is diminished. Institutional plumbing can stabilize demand, but it does not immunize Bitcoin from liquidity shocks—especially in a world where central banks may provide relief only reactively (to address funding strains) rather than proactively (to stimulate risk taking).

Bitcoin

Policy and Regulation

Disclaimer

For questions & inquiries

info@tokeninsight.com

For research & editorial

research@tokeninsight.com

2018 – 2026 © TokenInsight Ltd. All rights reserved

Use TokenInsight App All Crypto Insights Are In Your Hands

Open