The crypto market continues cooling down and there are few exciting projects and news coming out. While the market is quiet, governments across the globe are busy drafting crypto regulation frameworks. A proper and clear supervision framework is key for the future development of crypto.

This article summarizes crypto regulation development in some major countries and regions. It serves as a bird's view of what is happening around the world.

The crypto market continues cooling down and there are few exciting projects and news coming out. While the market is quiet, governments across the globe are busy drafting crypto regulation frameworks. A proper and clear supervision framework is key for the future development of crypto.

This article summarizes crypto regulation development in some major countries and regions. It serves as a bird's view of what is happening around the world.

This article covers countries and regions in below order:

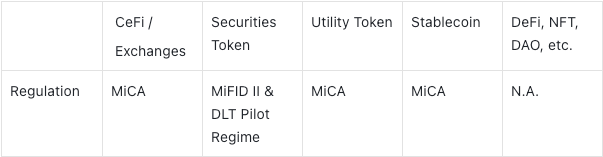

While a few European countries, like Germany, already have basic crypto regulations, I would like to focus on E.U. as a whole rather than dig into each country's particular situation.

The E.U. as a whole has proposed one of the most comprehensive regulations for crypto in the world.

The framework involves two major parts:

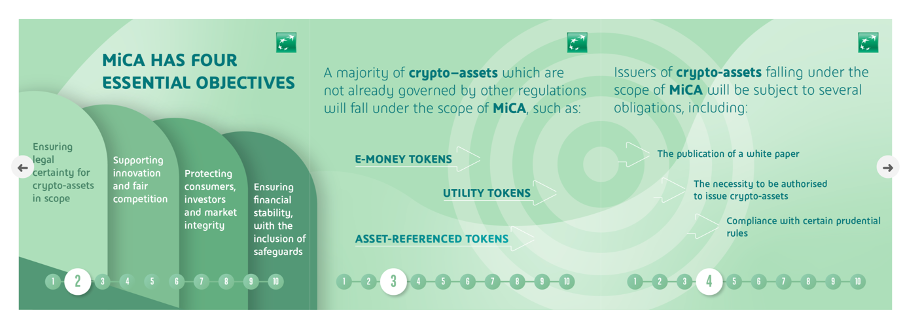

MiCA is the first crypto regulation in the world that clearly outlines a comprehensive framework. MiCA focuses on all crypto asset that is not subjected to other regulations, such as security token (which are subject to securities law) or central bank digital currencies.

MiCA covers:

MiCA clearly set out some requirements for crypto asset issuance, such as:

Crypto asset services providers that provide custody, administration, and provision of advice on crypto assets are all regulated under MiCA.

If apply the current securities law to crypto securities tokens, no project could be able to issue tokens at all. The DLT Pilot Regime seek to offer some exemption from securities law for securities token and place a cap on the capital involved.

E.U. is about to finalize one of the world's most comprehensive crypto regulation frameworks, encompassing both securities tokens and utility tokens. It has also offered the DLT Pilot Regime for securities tokens rather than applying the current securities law in full to securities tokens.

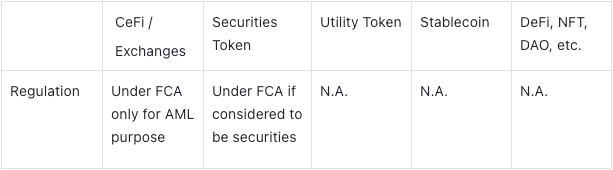

FCA - Financial Conduct Authority regulates the securities and financial service industry and is now the main body responsible for crypto regulation. Currently, crypto exchanges must register with FCA to conduct business in the U.K.

FCA's role in registering crypto exchanges is solely for anti-money laundering purposes, whilst most crypto assets and associated businesses remain unregulated.

In April 2022, the U.K. government announced plans to become a "global crypto-asset technology hub" with stablecoins being used "as a recognized form of payment".

Some highlights of the plan include:

The crypto regulation in the U.K. is still in the preliminary consultation phase. Due to the fall of Terra, stablecoin regulation could probably first be drafted, and the regulation for broader crypto industry, including token issuance and DeFi has not been put on the agenda.

The crypto regulation in the U.S. is complex in terms of two dimensions:

There is currently no crypto regulation at the Federal level that covers crypto-related activities and authorizes Federal Agencies to regulate crypto. A number of crypto bills have been proposed by different senators.

The process in the U.S. political structure for a bill to pass follows the below procedure:

No crypto bill has even finished the first step. So, it is still a long way to go for a Federal level crypto regulation.

The most important bill up to date is the one proposed by Cynthia Lummis and Kirsten Gillibrand, the "Responsible Financial Innovation Bill". If you are interested in a detailed explanation for this bill, here is a video by Coin Bureau.

Federal-level regulation may not be enacted any time soon, making it worthwhile to have an overview of how different states regulate crypto activities.

There have generally been two approaches to regulation at the state level.

Some states have quite favorable regulations exempting crypto from state securities law and/or money transmission statutes. Examples of this category include:

Some other states hold a tougher stance regarding Crypto, such as New York, Maryland, and Iowa.

In Singapore, the Monetary Authority of Singapore (MAS) is responsible for crypto regulation.

The way MAS regulates crypto is to apply the existing legal framework where possible, rather than draft an independent new crypto regulatory framework.

Crypto activity is subject to two key regulations

For stablecoin, if it is a fiat-backed centralized stablecoin, it will be classified as "e-money" and is covered in PSA.

Instead of regulating crypto-related activity under existing regulatory bodies, Dubai set up a completely new authority for crypto assets - the Dubai Virtual Assets Regulatory Authority (VARA).

VARA is mandated to organize and set rules and controls for virtual asset-related activities. It covers full range of activities:

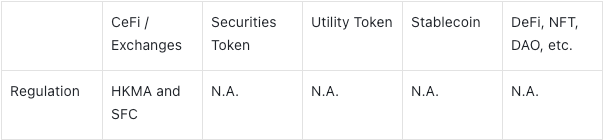

SFC and HKMA are responsible for regulating crypto-related activities:

Securities and Futures Commission (SFC) - responsible for securities and futures markets

The Hong Kong Monetary Authority (HKMA) - responsible for financial stability and the banking system.

In early 2022, HKMA and SFC jointly introduced a new regime for financial intermediaries to deal with "virtual asset" - related products and provide crypto asset trading and advisory services.

The framework mainly focuses on CeFi entities, no clear regulatory progress regarding token issuance, DeFi, or DAO.

This article is not a comprehensive summary of crypto asset regulations around the world. It's just a brief of the regulatory process in each of the major jurisdictions to date. We hope that readers will gain a basic understanding of the key milestones in crypto asset regulation through the article. In addition, because the crypto industry is evolving so rapidly, lots of information in this article may no longer be accurate in terms of timeliness. We welcome readers to point them out at any time and we will make corrections as soon as possible.

APP

APP