Binance was undoubtedly the biggest winner in the crypto exchange industry in 2022. FTX, a potential challenger to Binance, was completely wiped out in about a week. In the DEX world, GMX emerged as the dark horse in the bear market. Read the report for more data analysis of crypto exchanges in 2022.

Binance was undoubtedly the biggest winner in the crypto exchange industry in 2022. FTX, a potential challenger to Binance, was completely wiped out in about a week. In the DEX world, GMX emerged as the dark horse in the bear market. Read the report for more data analysis of crypto exchanges in 2022.

2022 was a tumultuous year for the crypto industry. In addition to the significant price declines of almost all coins, there have been numerous layoffs, rugs, and even multiple bankruptcies in the industry. Exchanges are one of the most important segments of crypto, and changes in trading volume and market share are the most direct manifestation of the industry's rise and fall.

TokenInsight, as a crypto rating and research company, has been tracking the data of coins and exchanges. We have summarized the data performance of the exchange industry over the year and selected the top 10 centralized and decentralized exchanges, hoping to get a clear picture of the changes over the year and the competition in the exchange market through the changes in data.

The data below summarizes the top 10 exchanges selected by TokenInsight and does not include the total trading volume of all exchanges. This is done for two main reasons

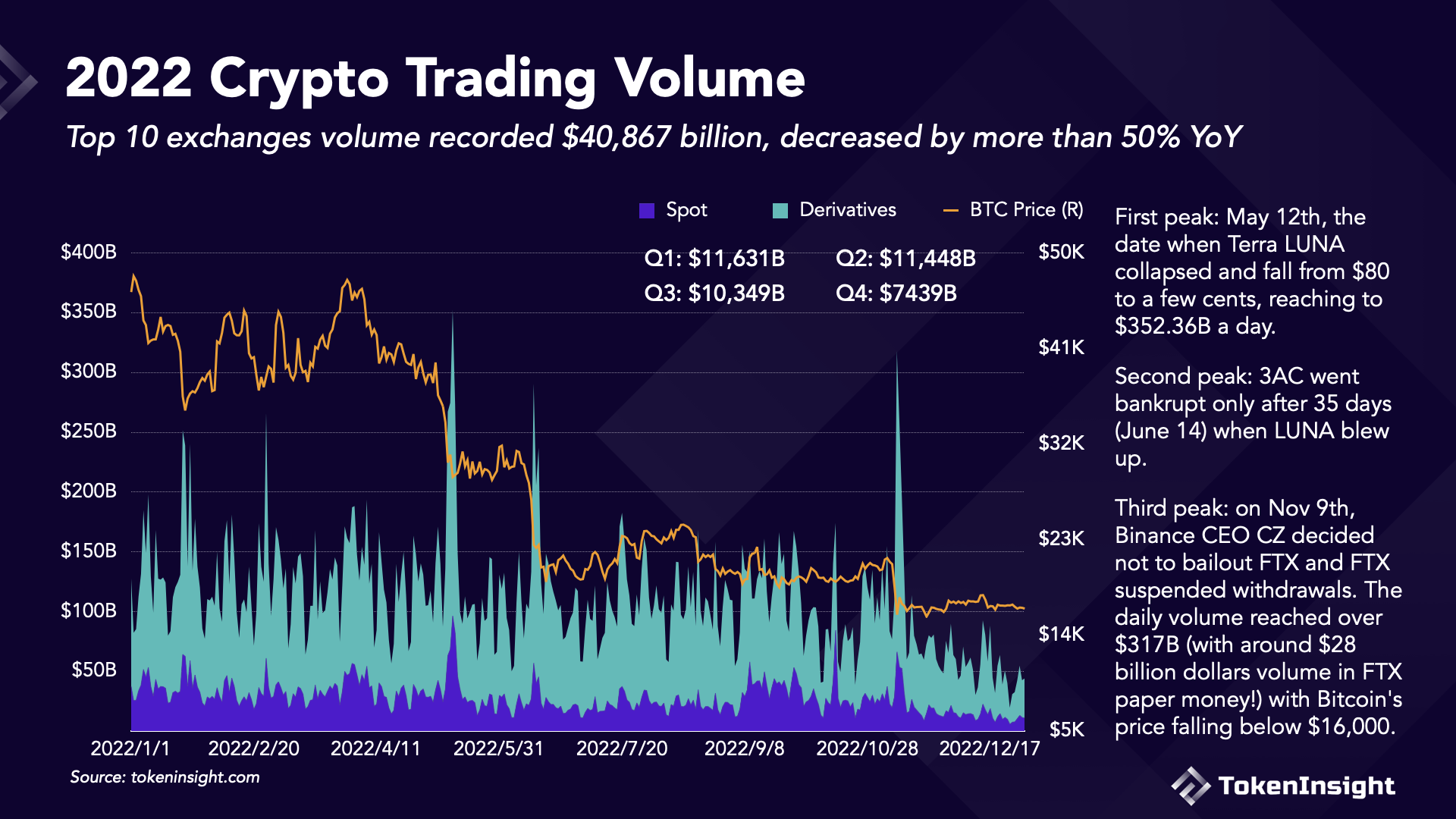

In 2022, the top 10 centralized exchanges total trading volume (spot + derivatives) reached $40.867 trillion, dropping more than 50% compared to 2021. A total of 3 peaks appeared in May, June, and November.

The highest daily volume peak happened on May 12, when Terra LUNA (now LUNC) collapsed and fell from $80 to a few cents, reaching $352.36 billion daily.

The fall of Terra: On May 7, the price of the then $18-billion algorithmic stablecoin terraUSD (UST), which is supposed to maintain a $1 peg, started to wobble and fell to 35 cents on May 9. Its companion token, LUNA, which was meant to stabilize UST's price, fell 96% by May 12. Meanwhile, Terras' largest DeFi protocol, Anchor, an asset management protocol providing a 20% interest rate for holding UST, also shrunk $11 billion total locked value (TVL) from its pool a day.

Following the fall of Terra, Three Arrows Capital (3AC), one of the most prominent hedge funds in crypto founded by Su Zhu and Kyle in 2012, went bankrupt only after 35 days (June 14) when LUNA blew up. The liquidation of 3AC not only dragged Bitcoin prices to fall 15.8%, spiking the total market trading volume to $290 billion on June 14, but also set off a contagion like the huge loss of crypto exchanges like Blockchaincom, FTX, AAX, lenders like Celsius, Genesis, and BlockFi, and the bankruptcy of digital asset brokerage Voyager Digital.

3AC managed around $10 billion in assets in March 2022, invested $200 million in LUNA in February, and had heavy positions in Anchor protocol.

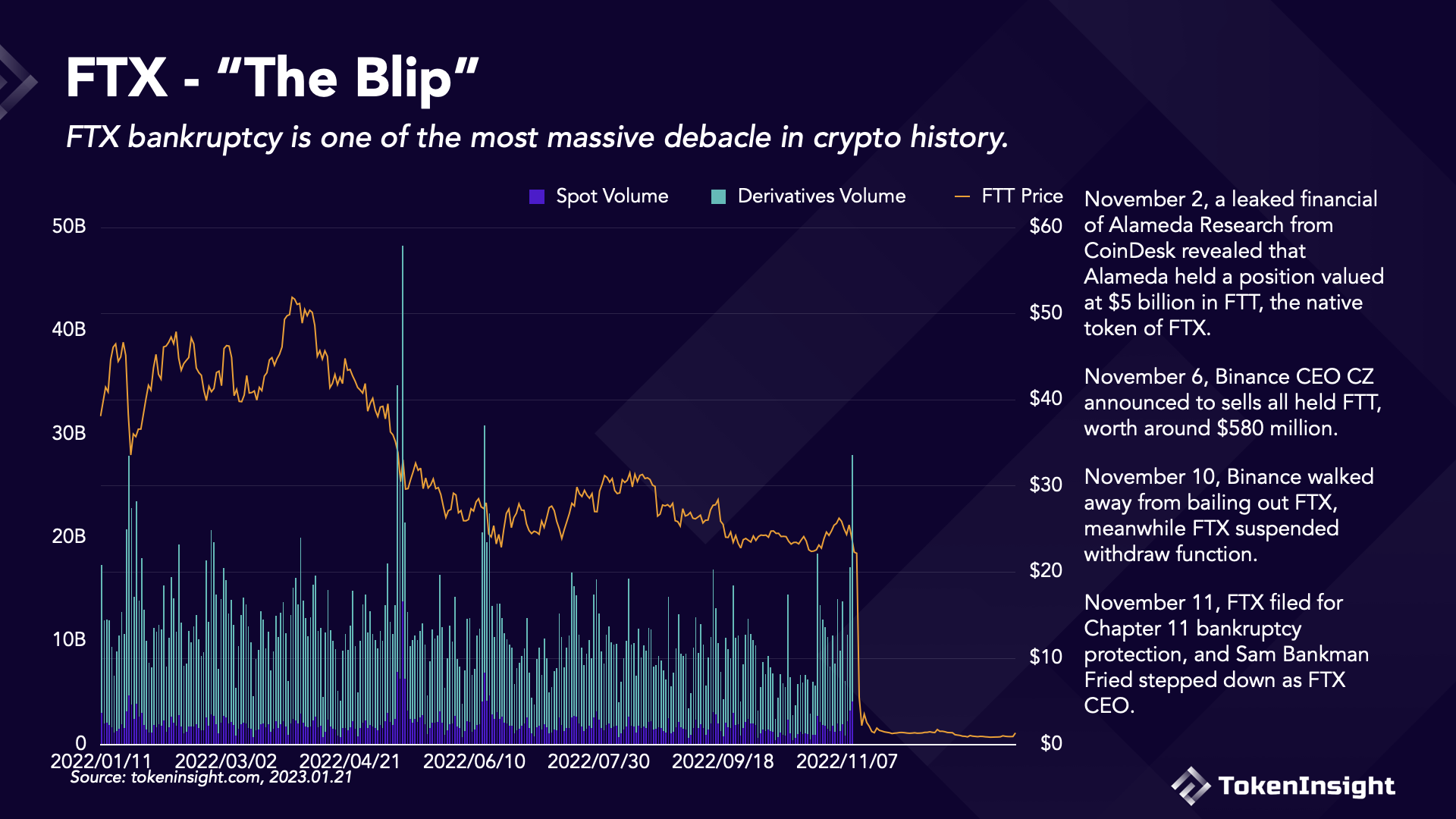

The third peak happened on November 9, when Binance CEO Changpeng Zhao (CZ) decided not to bail out FTX, and FTX suspended withdrawals. On November 9, the daily trading volume reached over $317 billion (with around $28 billion volume in FTX paper money!) with Bitcoin's price falling below $16,000.

On November 2, a leaked financial of Alameda Research, a crypto trading firm founded by FTX's founder SBF, showed that it has a close relationship with FTX. A few days later, on November 6, CZ decided to sell around $580 million worth of FTT, the exchange token of FTX, triggering the crash of FTX.

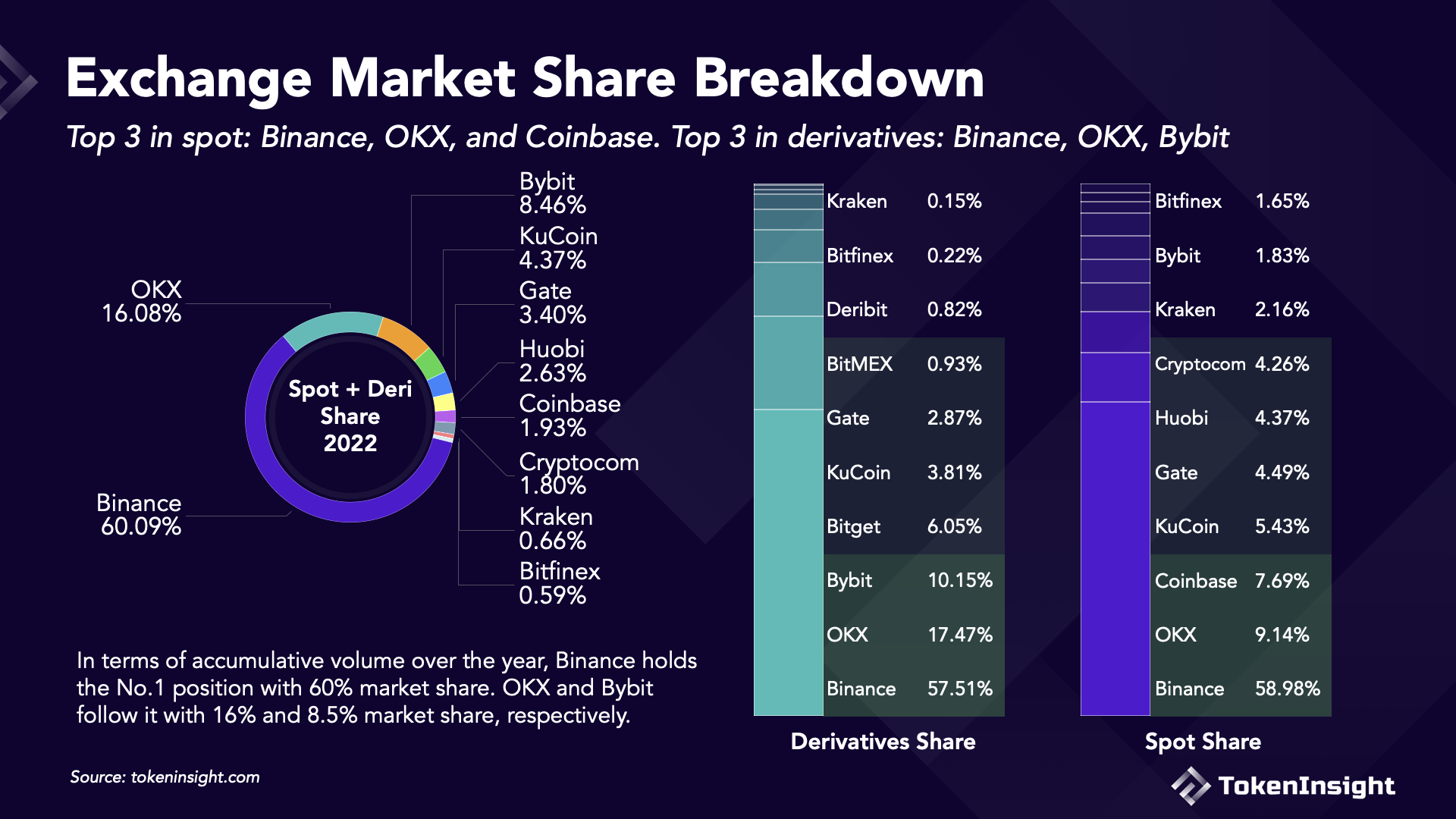

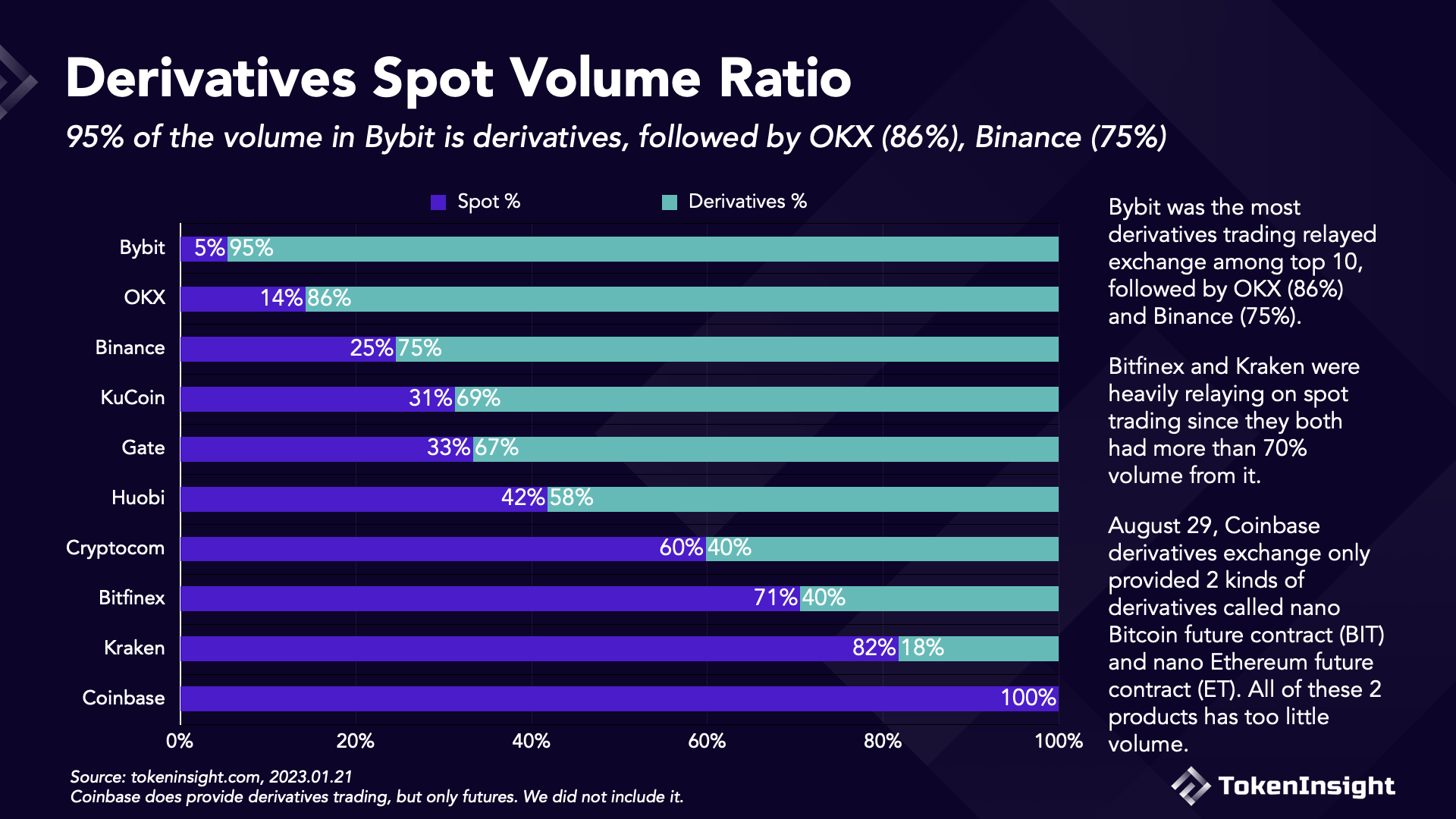

The top 10 list is slightly different after breaking down exchange volume into spot and derivatives.

Binance and OKX are the Top 2 in every category. Bybit, KuCoin, Gate, Kraken, and Bitfinex are on both lists. Coinbase, Huobi, and Cryptocom are in the Spot Top 10 only, while Bitget, BitMEX, and Deribit are in the Derivatives Top 10 only. Crypto derivatives generate much more volume than spot. Thus Bybit ranks third in the combined list whereas Coinbase only ranked seventh.

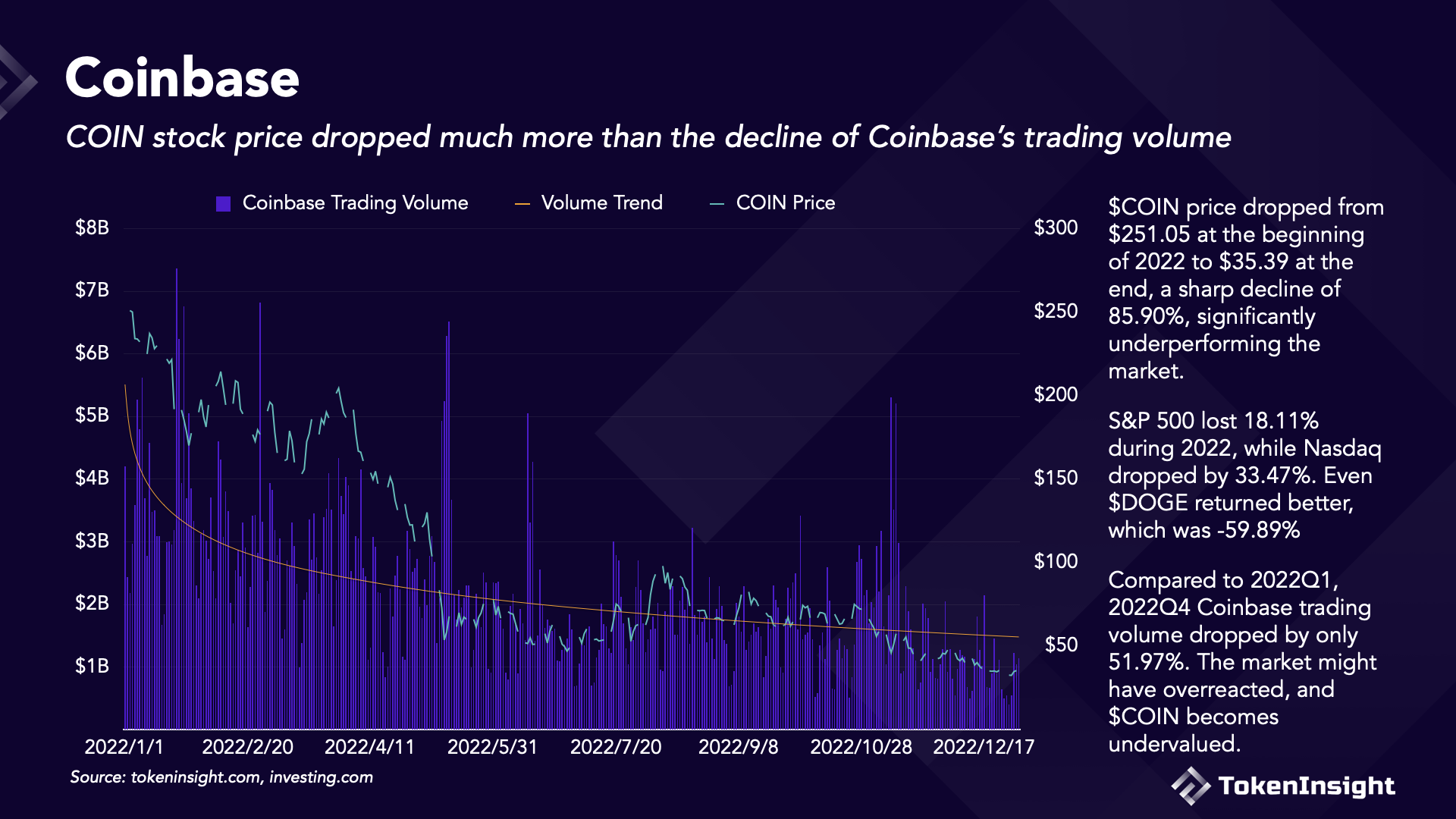

$COIN price dropped from $251.05 at the beginning of 2022 to $35.39 at the end, a sharp decline of 85.90%, significantly underperforming the market. S&P 500 lost 18.11% during 2022, while Nasdaq dropped by 33.47%. Even $DOGE returned better, which was -59.89%.

On the other hand, Coinbase's trading volume didn't drop as much. Compared to 2022Q1, 2022Q4 Coinbase trading volume dropped by only 51.97%. The market might have overreacted, and $COIN became undervalued.

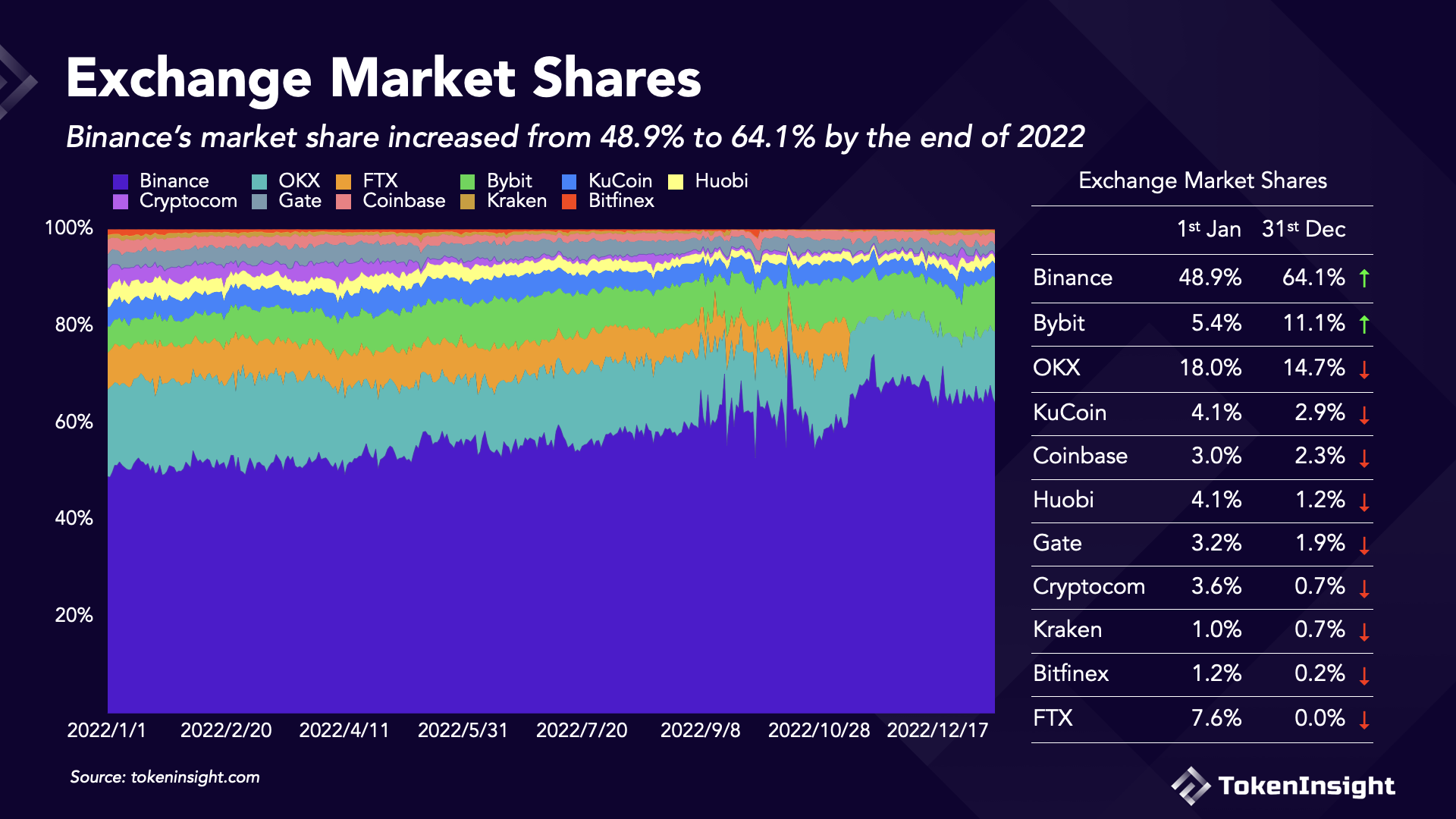

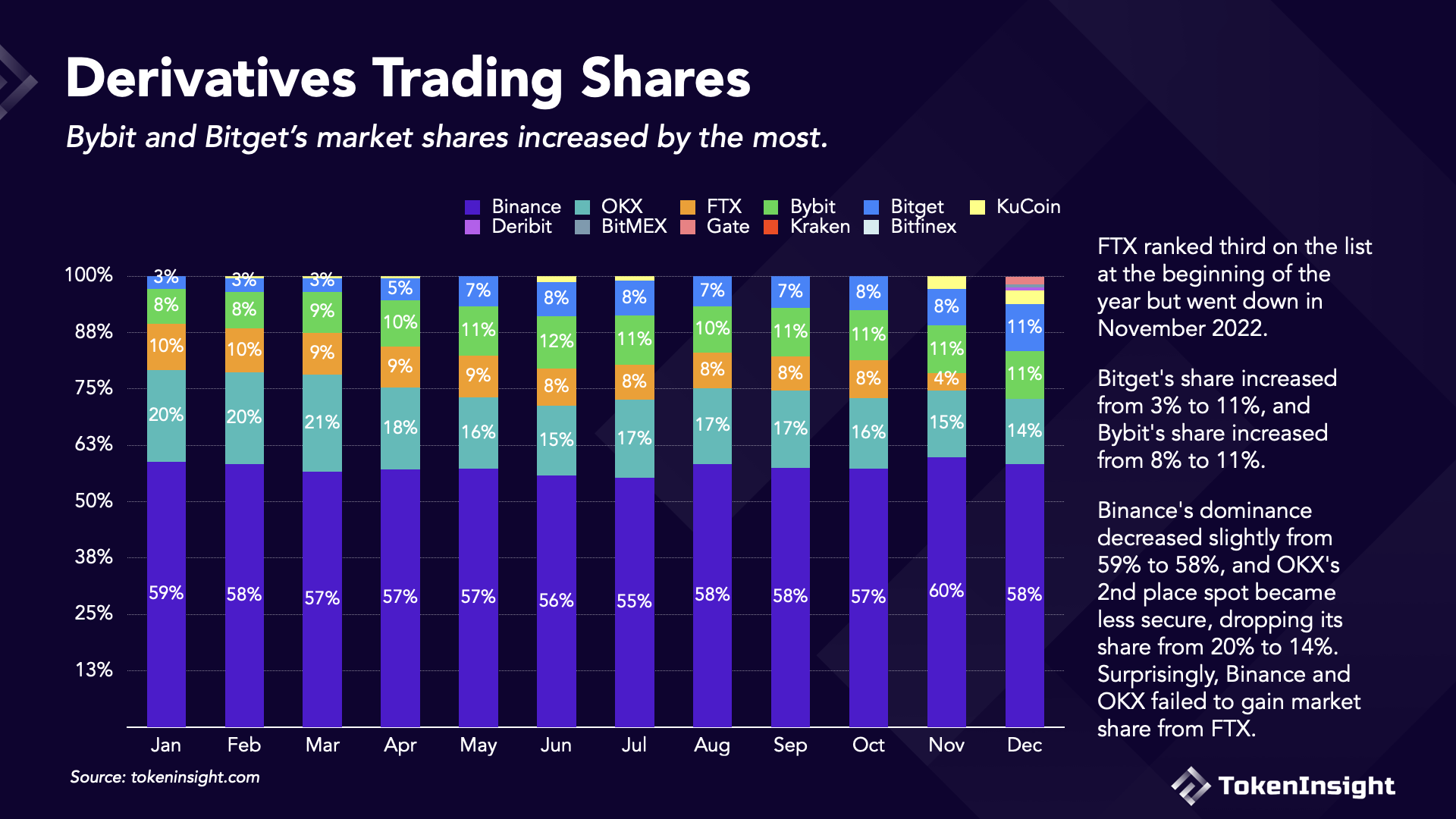

On the derivatives front, Bybit and Bitget benefitted the most from the collapse of FTX. FTX ranked third on the list at the beginning of the year but went down in November 2022. Bitget's share increased from 3% to 11%, and Bybit's share increased from 8% to 11%.

Binance's dominance decreased slightly from 59% to 58%, and OKX's 2nd place spot became less secure, dropping its share from 20% to 14%. Surprisingly, Binance and OKX failed to gain market share from FTX.

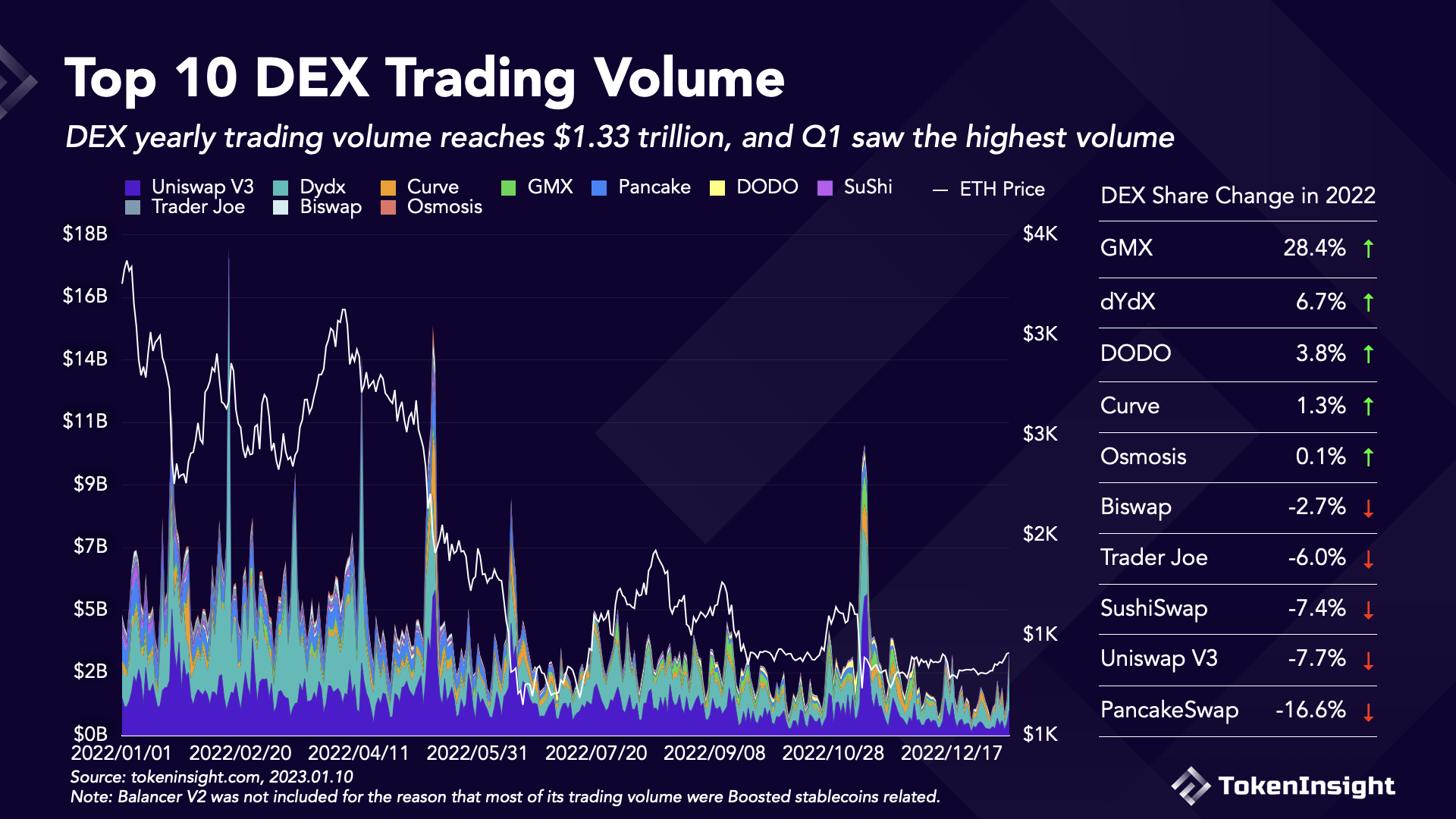

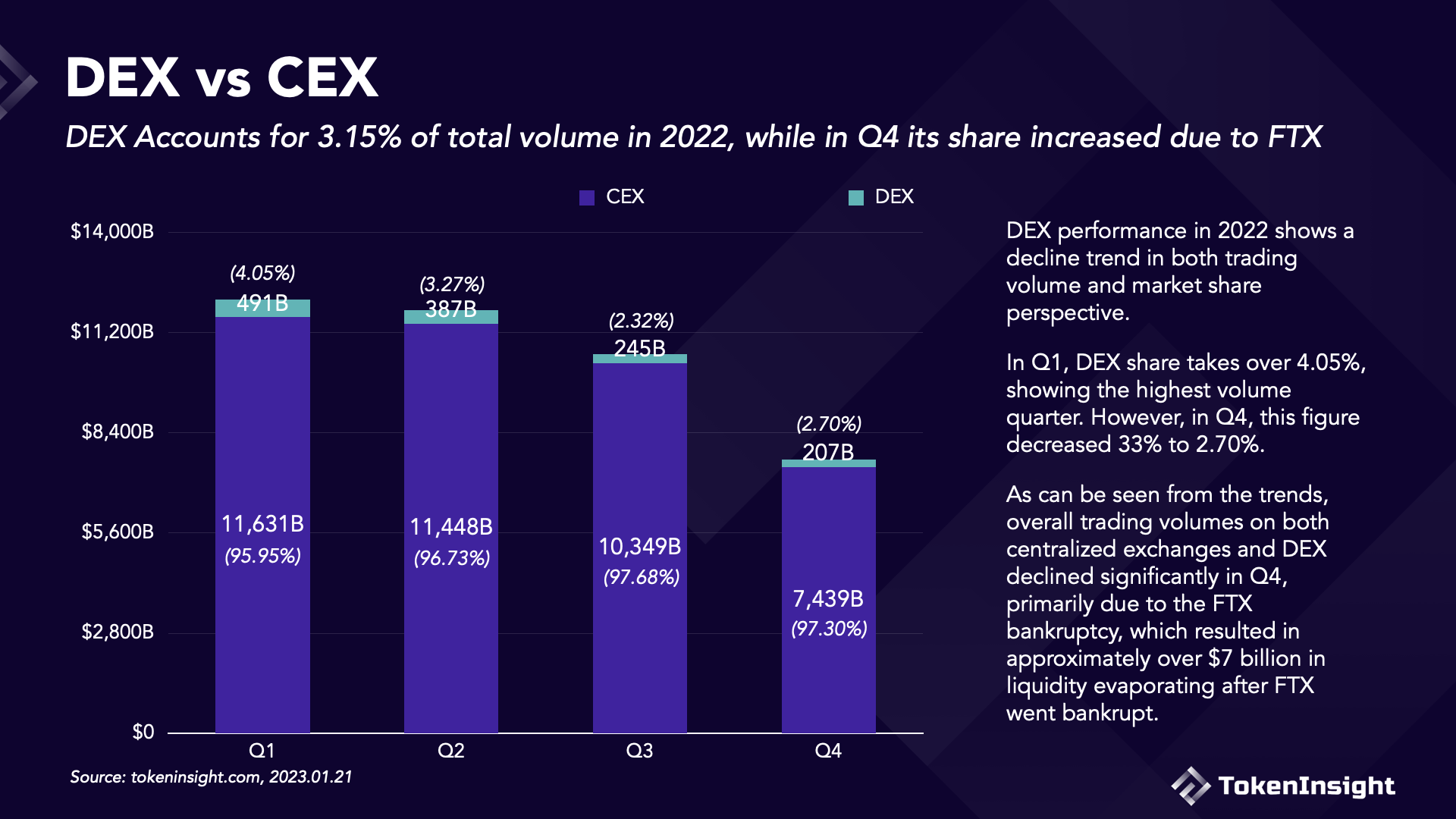

DEX's performance declined in trading volume and market share between Q1 and Q4.

In Q1, DEX represented 4.05% of the trading volume, the highest in 2022. This figure decreased by 33% to 2.70% by the end of Q4.

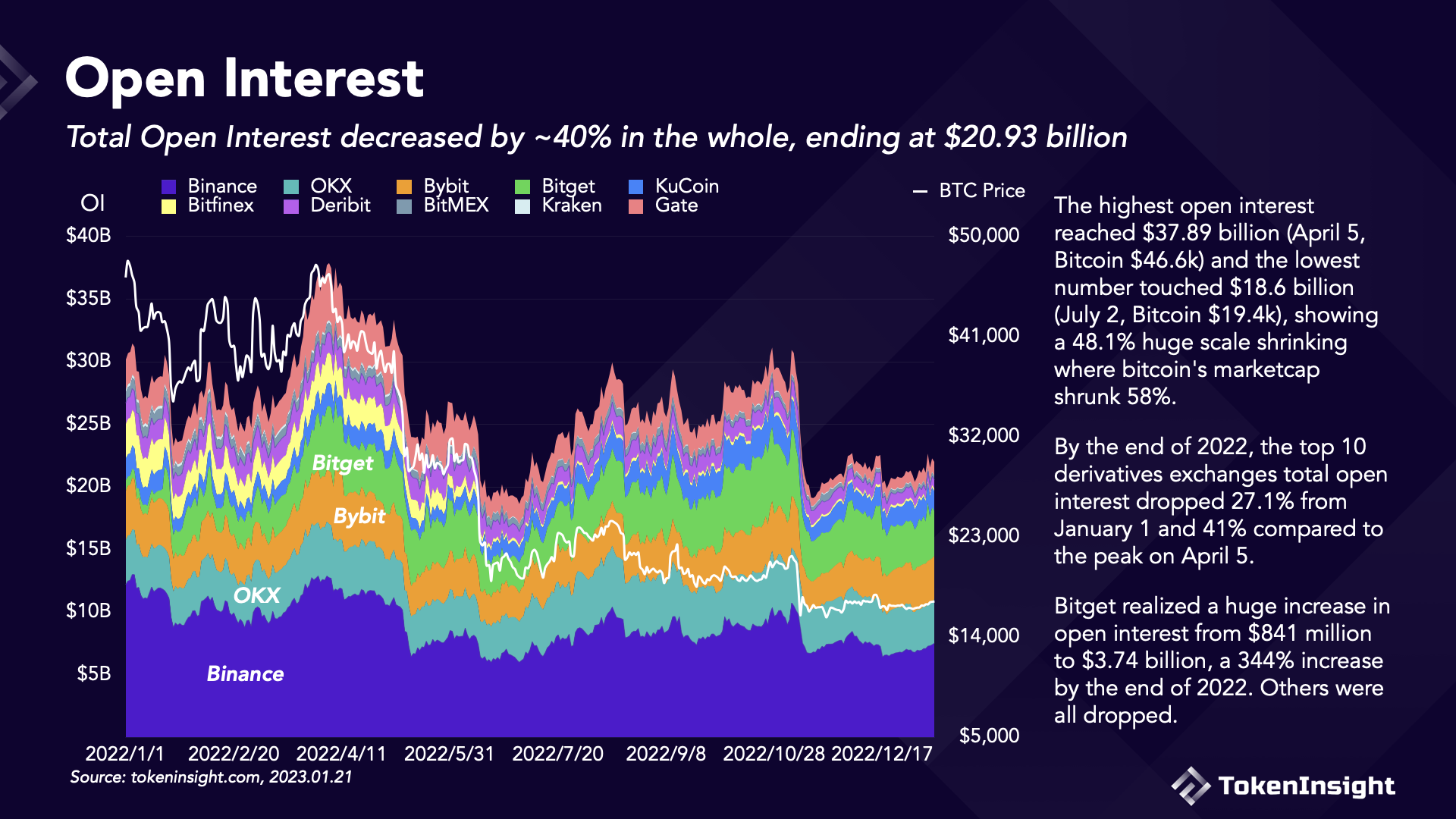

Trading volume on both centralized exchanges and DEX declined significantly in Q4, primarily due to FTX filing for bankruptcy, which resulted in approximately over $7 billion in liquidity evaporating from the exchange.

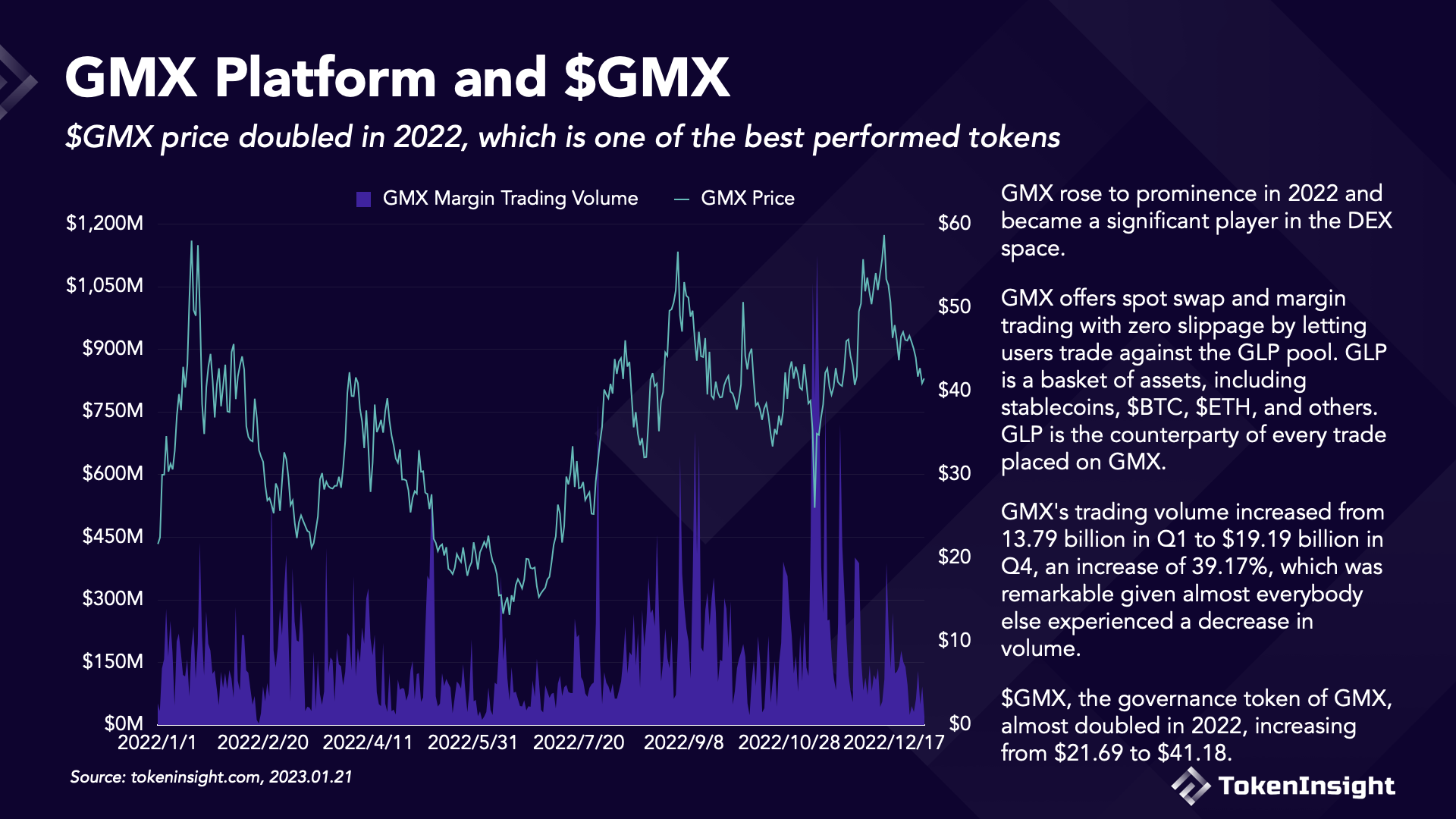

GMX rose to prominence in 2022 and became a significant player in the DEX space. GMX was launched on Arbitrum on September 1, 2021. It offers spot swap and margin trading with zero slippage by letting users trade against the GLP pool. GLP is a basket of assets, about 50% of which are stablecoins, and the other half are cryptocurrencies like $BTC (15%) and $ETH (35%). GLP is the counterparty of every trade placed on GMX.

GMX's trading volume increased from 13.79 billion in Q1 to 19.19 billion in Q4, an increase of 39.17%, which was remarkable given almost everybody else experienced a decrease in volume. $GMX, the governance token of GMX, almost doubled in 2022, increasing from $21.69 to $41.18.

FTX bankruptcy is one of the most massive debacles in crypto history. The collapse took place over ~10 days in November 2022.

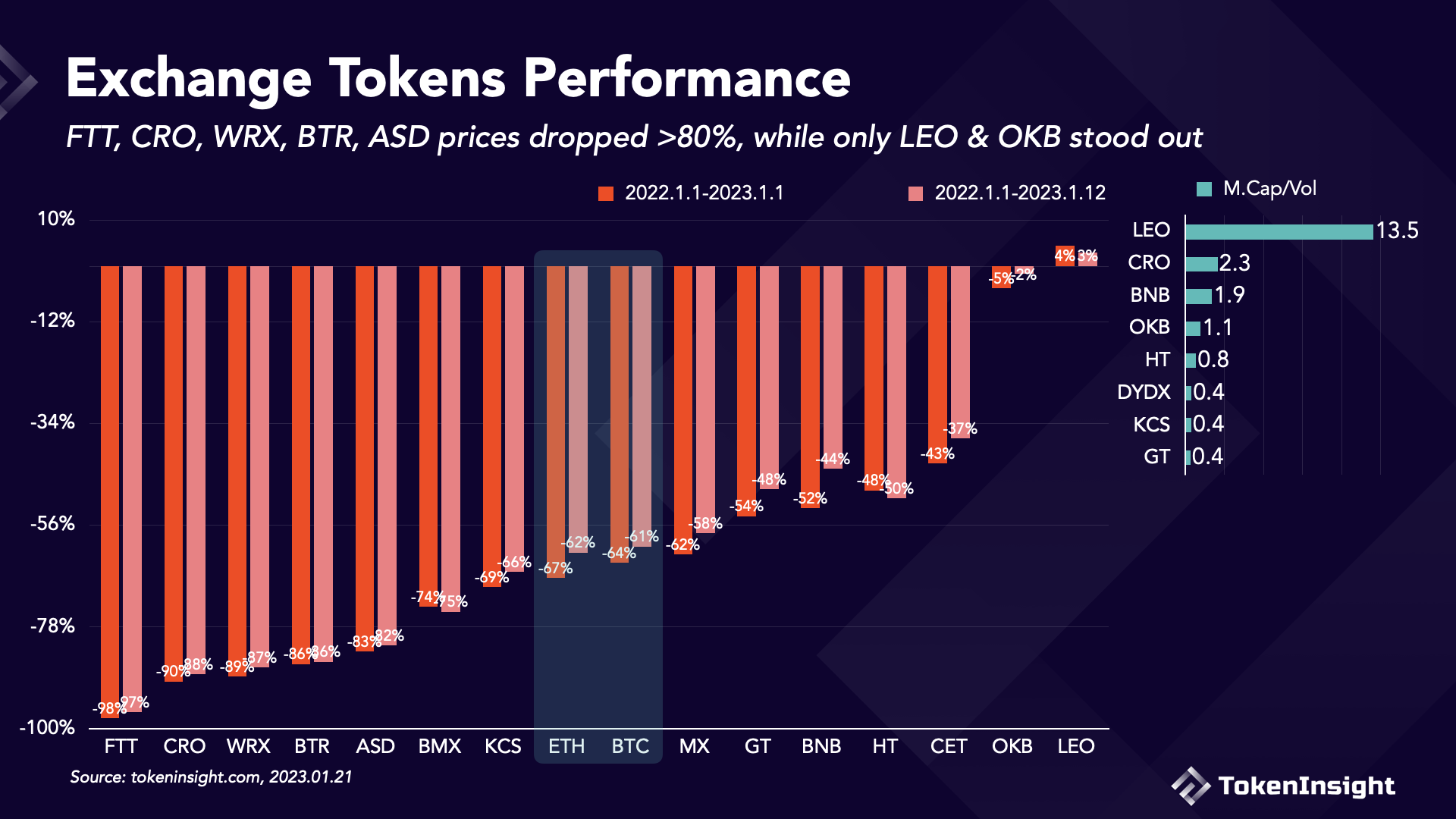

Almost all exchange tokens suffered significant losses in 2022. FTT, CRO, WRX, BTR, and ASD prices dropped by more than 80%, while LEO and OKB showed relative strength.

LEO increased by 3% in 2022, while OKB decreased by only 5%. Other than FTT, tokens issued by bigger exchanges performed better than smaller exchanges. For example, although HT, GT, and BNB also dropped a lot, they outperformed BTC and ETH in 2022.

In terms of market cap/trading volume, a higher ratio indicates a higher valuation. The ratio of HT, DYDX, KCS, and GT was <1, showing they could be undervalued. The ratio of CRO, BNB, and OKB was >1, while LEO was at the bottom of the table with a ratio of 13.5.

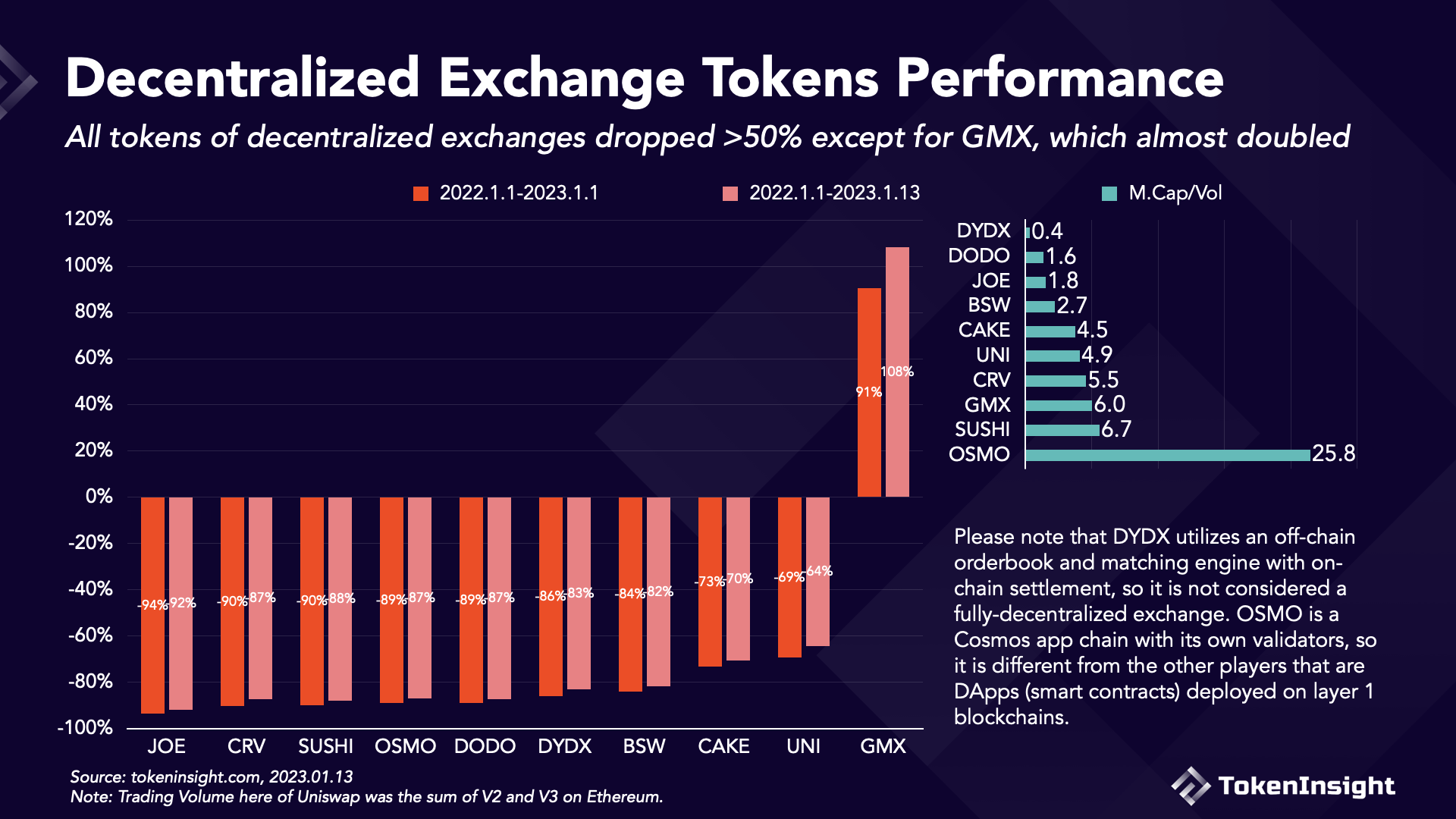

Similar to centralized exchange tokens, prices of decentralized exchange tokens suffered significant losses in 2022 except for GMX. Sector leader UNI dropped by 69%, while other players dropped even more. JOE was the worst with a decrease of 94%. On the other hand, GMX's price almost doubled in 2022, increasing by 91%, standing out from the rest of the crowd.

In terms of market cap/trading volume, JOE, DODO, and DYDX seemed undervalued with ratios of 1.8, 1.6, and 0.4, respectively. SUSHI, GMX, and CRV had relatively high valuations with respect to the volume they processed, and OSMO seemed to be the most overvalued with a ratio of 25.8.

Please note that DYDX utilizes an off-chain orderbook and matching engine with the on-chain settlement, so it is not considered a fully-decentralized exchange. OSMO is a Cosmos app chain with its own validators, so it is different from the other players that are DApps (smart contracts) deployed on layer 1 blockchains.

APP

APP