Radiant Capital's recent performance has been quite impressive. After the Aribitrum airdrop, the price of $RDNT surged, and TVL increased sharply from over 20 million at the beginning of the year to over 100 million. After the launch of v2, its price even rose to a high of $0.48, nearly ten times the price at the beginning of the year. So, does Radiant still have room for price growth in the future? Will it continue to climb or will it burst like a bubble? I believe these are the questions that most investors want to know.

Radiant Capital's recent performance has been quite impressive. After the Aribitrum airdrop, the price of $RDNT surged, and TVL increased sharply from over 20 million at the beginning of the year to over 100 million. After the launch of v2, its price even rose to a high of $0.48, nearly ten times the price at the beginning of the year. So, does Radiant still have room for price growth in the future? Will it continue to climb or will it burst like a bubble? I believe these are the questions that most investors want to know.

We conducted in-depth research on Radiant Capital. After analyzing the data and information related to Radiant, we have come to the following conclusions:

So in the long run, Radiant Capital's price could see a significant downward trend after the Arbitrum boom.

Radiant Capital is a native lending protocol on Arbitrum, similar to AAVE and Compound. However, unlike traditional lending protocols, Radiant's lending service includes cross-chain functionality. Users can deposit collateral on chain A and then borrow from chain B. This feature can help Radiant improve its scalability on both aspects, blockchains and assets.

The cross-chain functionality of Radiant v1 is implemented through Stargate's cross-chain router. It allows users to deposit assets on Arbitrum and borrow on any EVM chain supported by Stargate. v2 is supported by Layerzero's OFT technology, which can help Radiant deploy new chains more quickly and eliminate dependence on Stargate.

Omnichain Fungible Token (OFT) is a cross-chain token standard that enables native assets to be transferred natively between blockchains, without the need for wrapped assets, intermediary chains, or liquidity pools.

After introducing the basic information of Radiant Capital, let's focus on its recent trend. In this section, we will analyze the recent trend of Radiant Capital from multiple dimensions through data and compare the data with leading lending protocols such as AAVE and Compound. Hopefully, this will give everyone a more intuitive understanding of the recent situation of Radiant Capital.

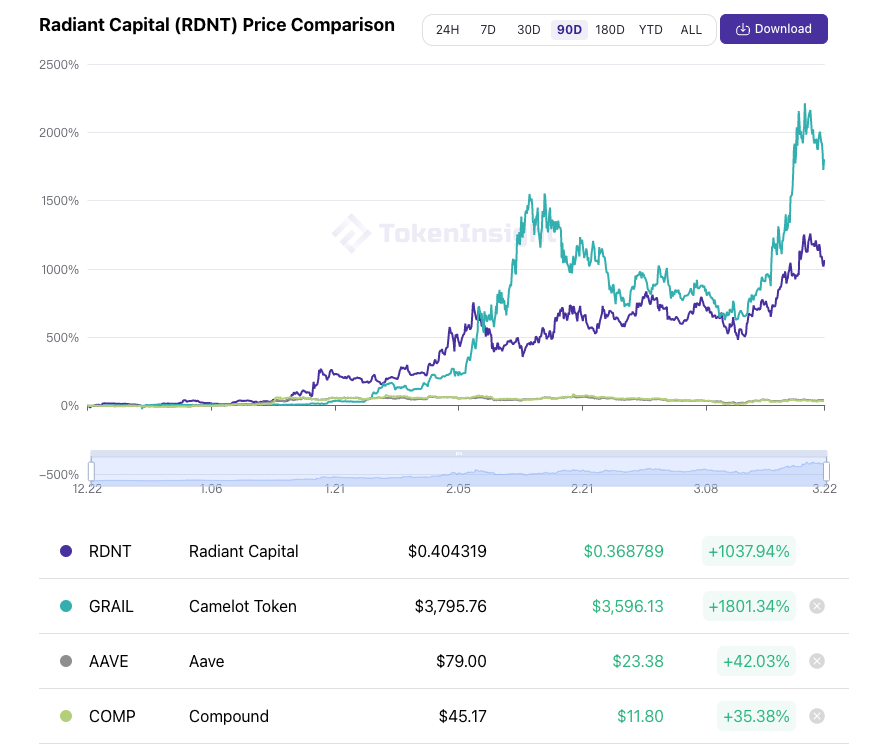

First of all, from the perspective of token price, there is no doubt that the price of $RDNT has risen significantly. Compared to 90 days ago, the price of $RDNT has grown nearly 10 times, from $0.04 to $0.4. Compared to lending protocols such as Aave and Compound, Radiant Capital's growth is also particularly outstanding, with a price increase of approximately 25 times more than theirs. It is the best-performing lending protocol in terms of price in 2023.

However, when analyzing the fundamental reasons for the price increase, the rise of $RDNT's price is actually not closely related to the development of the protocol itself but rather closely linked to the Arbitrum ecosystem. Since the beginning of the year, Arbitrum has attracted a lot of attention due to rumors of upcoming token issuance. Many tokens of projects related to the Arbitrum ecosystem have also skyrocketed in price due to its influence (such as Arbitrum's native DEX, Camelot). Therefore, as Arbitrum's native lending protocol, Radiant Capital has naturally been positively impacted, and its price has been rising all the way up. The Arbitrum airdrop announced on March 16th pushed the price of $RDNT to over $0.3. Later, the official launch of Radiant v2 further boosted its price, reaching a high of $0.48.

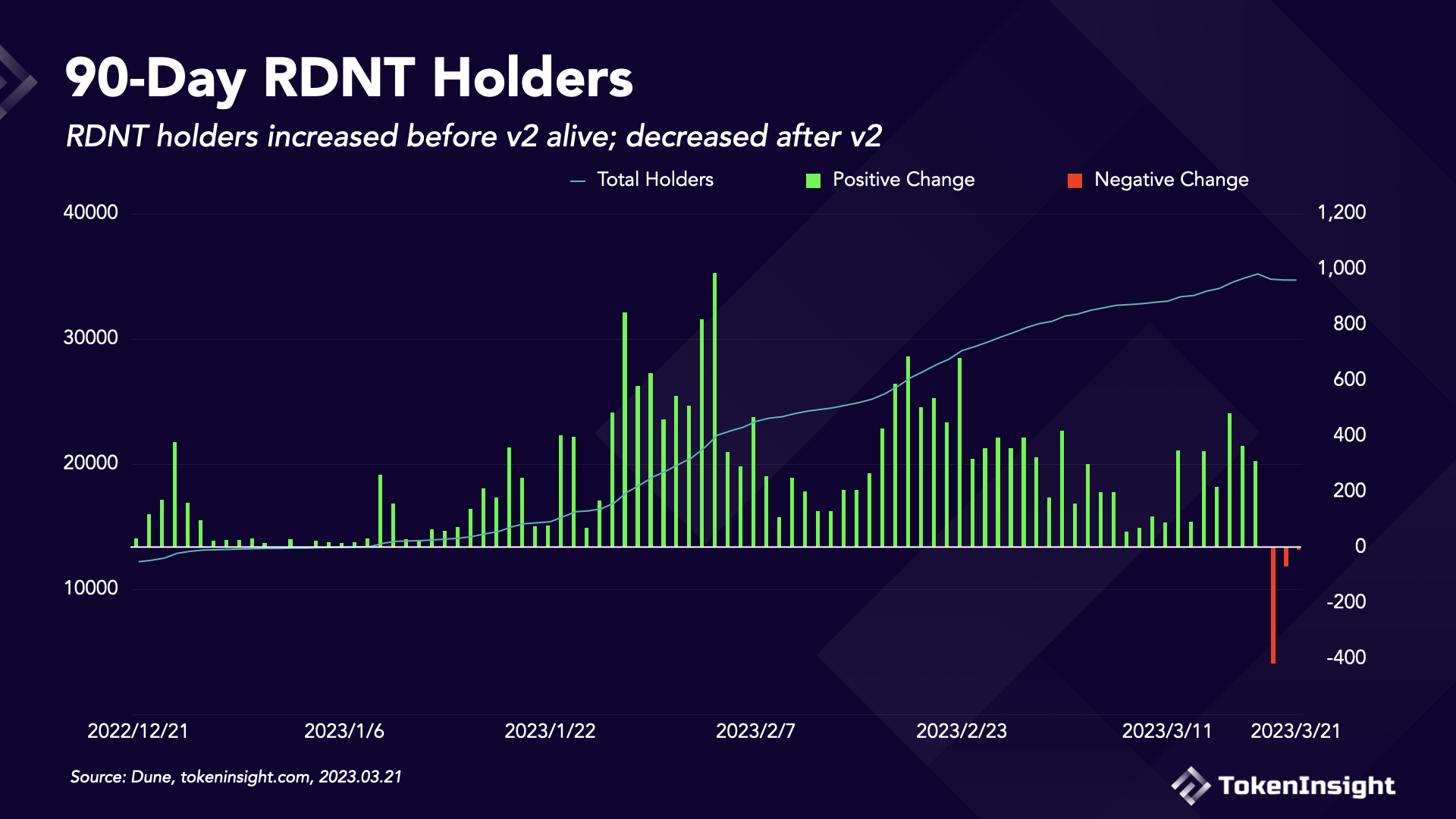

At the same time, we can see that the number of $RDNT holders has also increased to a certain extent. According to the $RDNT holder data on Dune, it can be seen that before March 19th (the date of Radiant v2 launch), the number of $RDNT holders had almost always been on the rise. Investors were frantically buying $RDNT. However, after the launch of v2, the number of $RDNT holders decreased significantly.

Regarding token releasing, in v1, the $RDNT tokens allocated to the community and team were originally planned to be released over a period of two years. With the update to the token economy in v2, the release time for these two portions has been extended to five years. At the same time, the team portion has changed from being directed entirely towards the release on Arbitrum to being released proportionally based on TVL on each chain. For example, if Radiant's TVL on Arbitrum accounts for 70% of the total TVL, and BNB Chain accounts for 30%, then the proportion of next month's release will be 7:3.

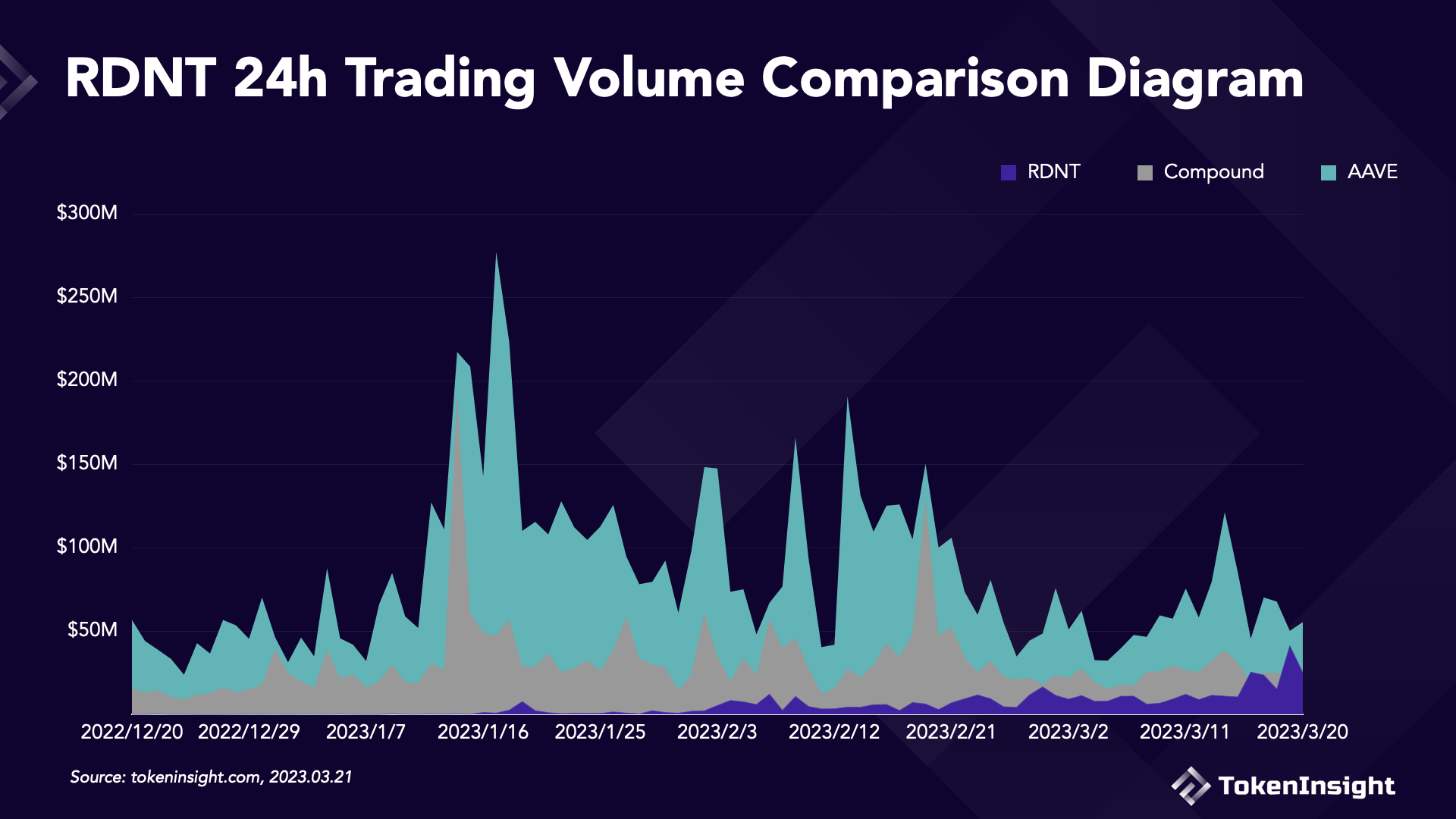

In addition, based on trading data, the 24-hour trading volume of $RDNT has continued to rise since the beginning of 2023, from less than $100,000 to a peak of $40 million. However, according to the latest data on March 20th, the 24-hour trading volume of $RDNT on that day has almost halved, dropping to around $25 million. Compared to the leading lending protocols in the market, AAVE and Compound, the current trading volume of $RDNT is on par with $COMP, but still has a large gap compared to $AAVE (with a difference of 1 times the amount on March 20th).

Before analyzing Radiant Capital's TVL, we need to first introduce the composition of TVL in DeFi protocols. Generally speaking, TVL refers to the total value of assets locked by users in a platform/protocol. However, the calculation of TVL generally includes multiple dimensions, such as Staking, Borrowing, etc. Their meanings are as follows:

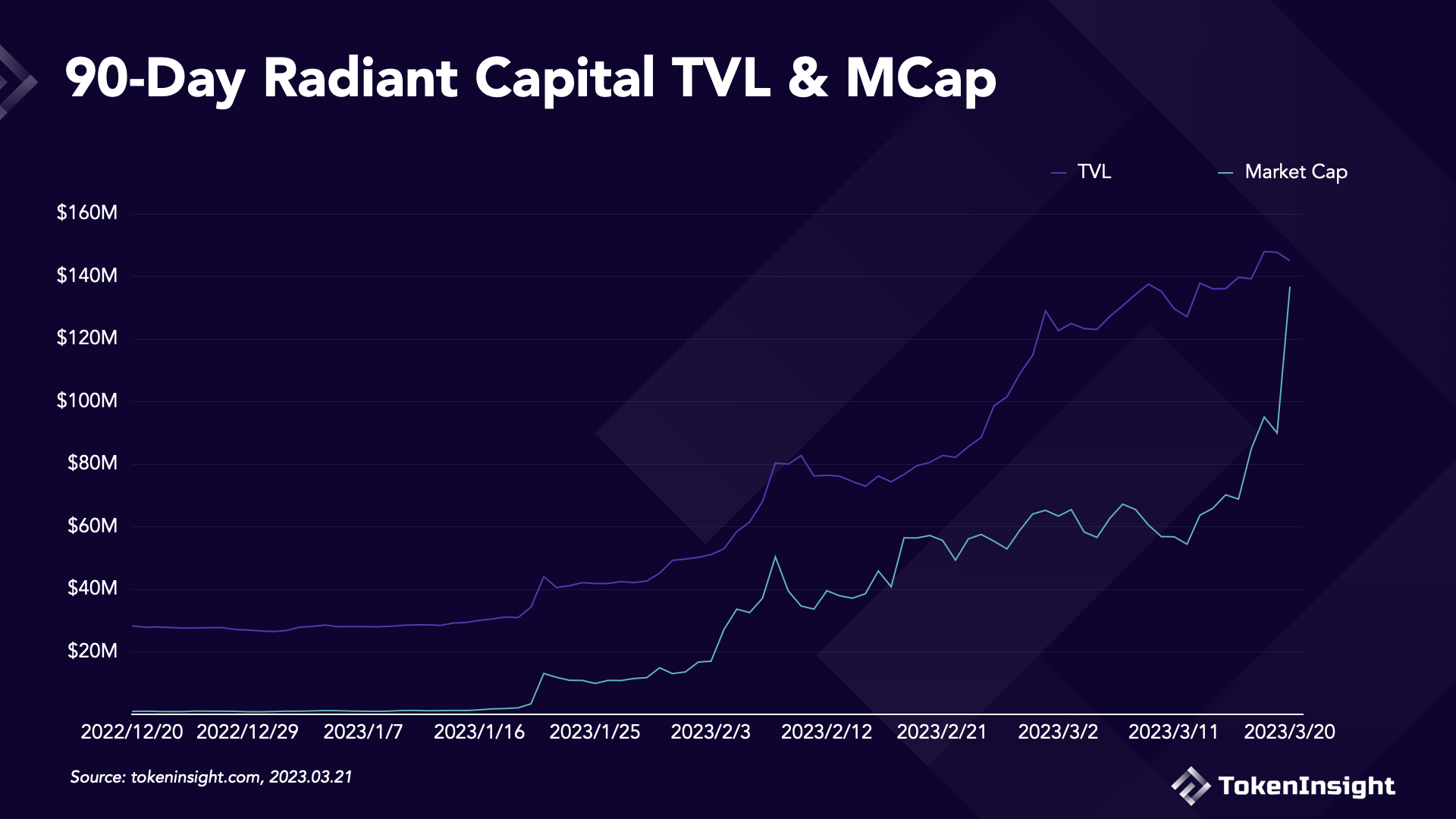

Therefore, when analyzing the protocol's TVL, these dimensions are usually calculated separately. According to data from Defillma, Radiant Capital's net TVL (excluding various dimension TVL) has been affected by the development of the Arbitrum ecosystem, rising from over $25 million at the beginning of 2023 to a peak of $148 million ($318 million). Currently, it ranks 6th among all lending protocols. Borrow TVL and Staking TVL have reached $178 million and $18 million respectively ($322 million), accounting for 48% and 5% of the total TVL (including all dimension TVL), both higher than AAVE.

However, on the other hand, Radiant Capital's market capitalization has soared from one million in January to 136 million (3.20). This has resulted in its market cap/TVL ratio increasing from around 0.03 previously to approximately 0.94. Although this value cannot fully reflect the value of Radiant Capital, it truly has the highest MCap/TVL ratio among the top ten lending protocols in the market. According to DefiLlama's data, when comparing the MCap/TVL values of the top ten lending protocols including AAVE and Compound, their results are mostly below 0.3. Among them, Benqi Lending, which has a TVL similar to Radiant's, has an MCap/TVL (3.20) that is only a quarter of Radiant's, at 0.26.

Therefore, this is actually not a very good sign. Because in DeFi protocols, the larger the MCap/TVL ratio, the greater the "bubble" of the protocol and indicates a lower value.

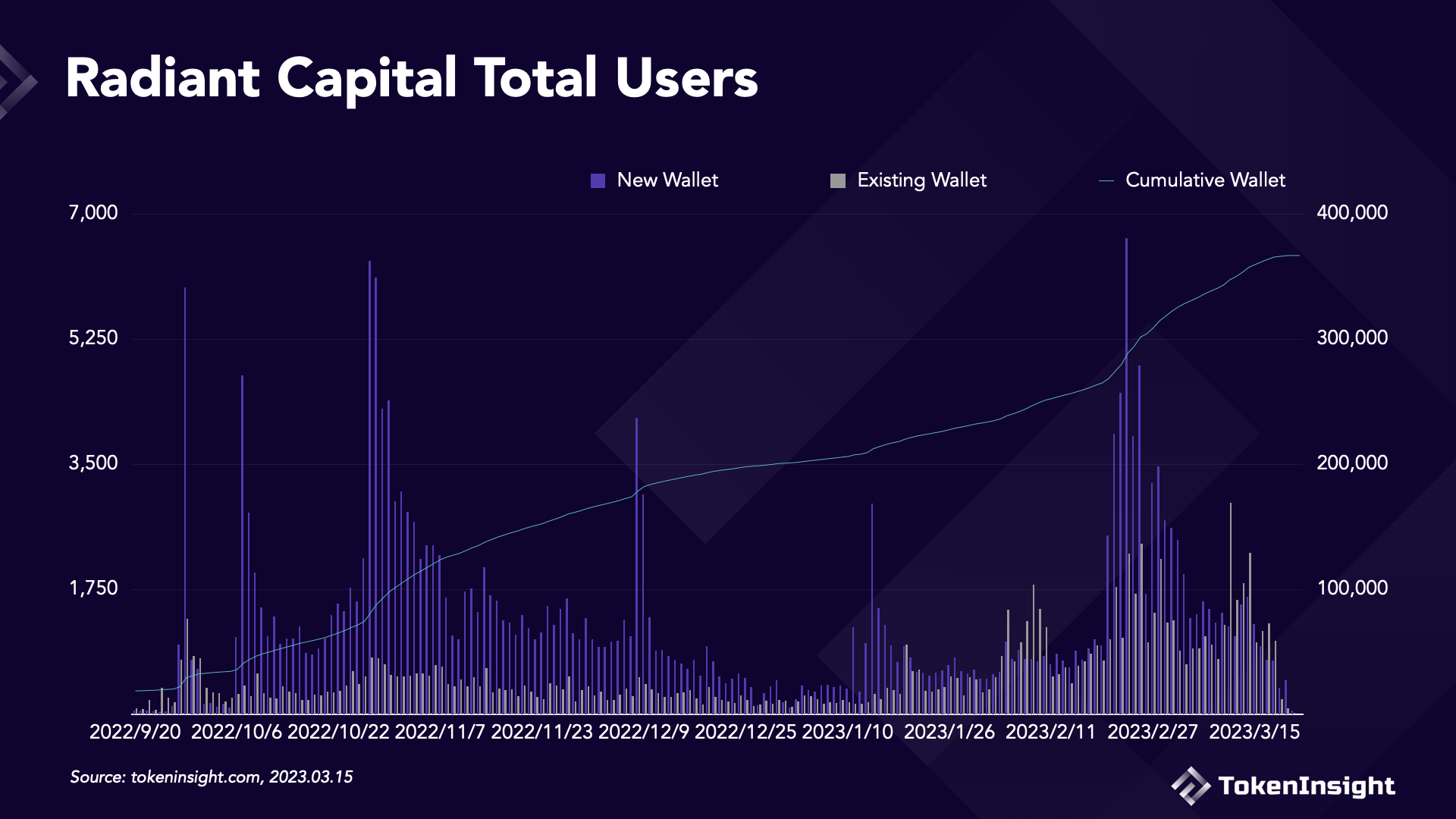

In terms of active users, according to user data from Radiant Capital on Dune, it can be seen that since the protocol went live, Radiant has experienced two relatively large waves of growth in user numbers, which occurred in the third quarter of 2022 and during the Arbitrum frenzy in January of this year. However, after the launch of v2, the rate of user growth for Radiant has noticeably declined, with the number of new wallets and existing wallets both dropping from hundreds to tens, with a decrease of over 90%. Currently, Radiant Capital has a total of 366,776 users (as of March 22).

Additionally, based on the list of $RDNT stakers, it can be seen that the top four historical $RDNT stakers are all Radiant teams. Currently, all of their stakes have expired, and based on their wallet history, the locked $RDNT has all been unlocked and stored in the team wallet, which may bring some concentration risk to Radiant. According to the list, the account with the largest locked $RDNT amount during the staking period is currently Radiant DAO Its assets on Arbitrum are worth about 25 million US dollars, of which the locked $RDNT amount is 19,192,096.

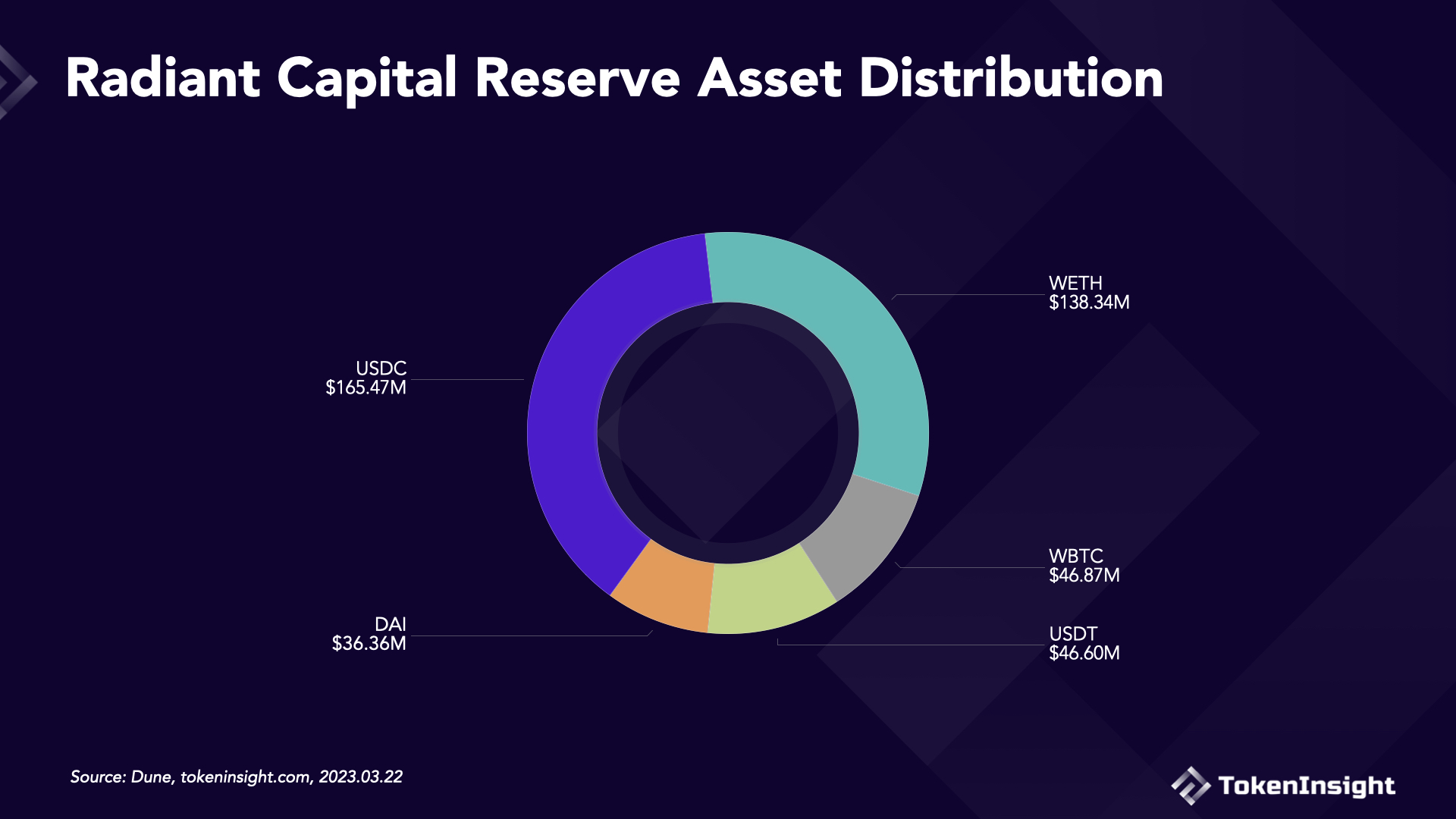

Currently, Radiant Capital supports 5 types of lending assets, namely $USDC, $DAI, $USDT, $ETH, and $WBTC.

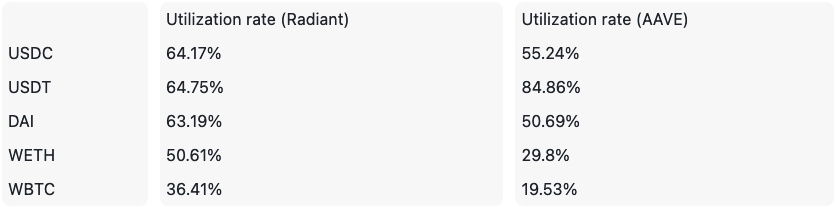

Among them, the largest reserve asset is $USDC, which is approximately $165 million, accounting for 38.16% of Radiant's total reserve assets. It is also the largest lent and borrowed asset on Radiant. The asset with the highest utilization rate on Radiant is $USDT, at 64.75%; its borrow interest rate is also the highest, at 24.99%. In terms of utilization rate, compared with the data of AAVE Arbitrum v3, the utilization rate of almost all types of assets on Radiant is higher than that of AAVE. At the same time, compared with other lending protocols on the market, Radiant's utilization rates are generally higher in numerical terms.

Compared to v1, Radiant Capital v2 mainly changes in two aspects:

Regarding the cross-chain mechanism, as mentioned earlier, the Stargate router will be replaced by the latest OFT cross-chain standard. This will help Radiant deploy new chains more quickly and eliminate reliance on third-party cross-chain bridges (Stargate). At the same time, Radiant's cross-chain lending functions will be expanded from previously only supporting Stargate-related EVM chains to supporting cross-chain lending on all EVM chains. This will provide Radiant Capital with more liquidity from different chains and enrich the variety of borrowing and lending assets.

In terms of token economics, Radiant Capital has introduced the concept of dLP to address the issue of $RDNT inflation. This can help Radiant extend the overall release time of its tokens and incentivize its long-term value growth. Simply put, instead of unrestricted release of $RDNT (which can be obtained by interacting with Radiant), only users who provide liquidity to Radiant Capital can obtain $RDNT (by locking dLP tokens) in v2.

After analyzing the five dimensions mentioned above and the main changes in v2, let's now answer some questions that investors are interested in:

In summary, after analyzing the five dimensions of price, liquidity, TVL, user numbers, and lending assets, Radiant Capital's performance in each dimension is as follows:

Among the five dimensions, token price and lending assets have performed positively. The price of $RDNT has shown a clear upward trend, and the asset utilization rate is significantly higher than the market average. However, token liquidity and user numbers of Radiant have both shown a declining trend. $RDNT's 24-hour trading volume has significantly decreased, and the number of new and existing wallets has gradually decreased. The overall protocol TVL has increased, but the MCap/TVL ratio is higher than the market average, indicating a significant "bubble" exists. Therefore, we believe that Radiant Capital's current price is generally overvalued. After the hype around Arbitrum subsides, there is a high possibility that the price of $RDNT will decrease in the future.

APP

APP