There has been a lot of buzz around EigenLayer's restaking recently. Today, we want to focus on EigenLayer's business model. So, how does EigenLayer's business model work? Can EigenLayer be profitable? Let's dive in and find out.

There has been a lot of buzz around EigenLayer's restaking recently. Today, we want to focus on EigenLayer's business model. So, how does EigenLayer's business model work? Can EigenLayer be profitable? Let's dive in and find out.

We conducted an in-depth analysis of EigenLayer's business model. After researching relevant data and information, we have come to the following conclusions:

EigenLayer's overall value is overestimated. In the long term, EigenLayer's business model might struggle to sustain profitability once the initial novelty wears off.

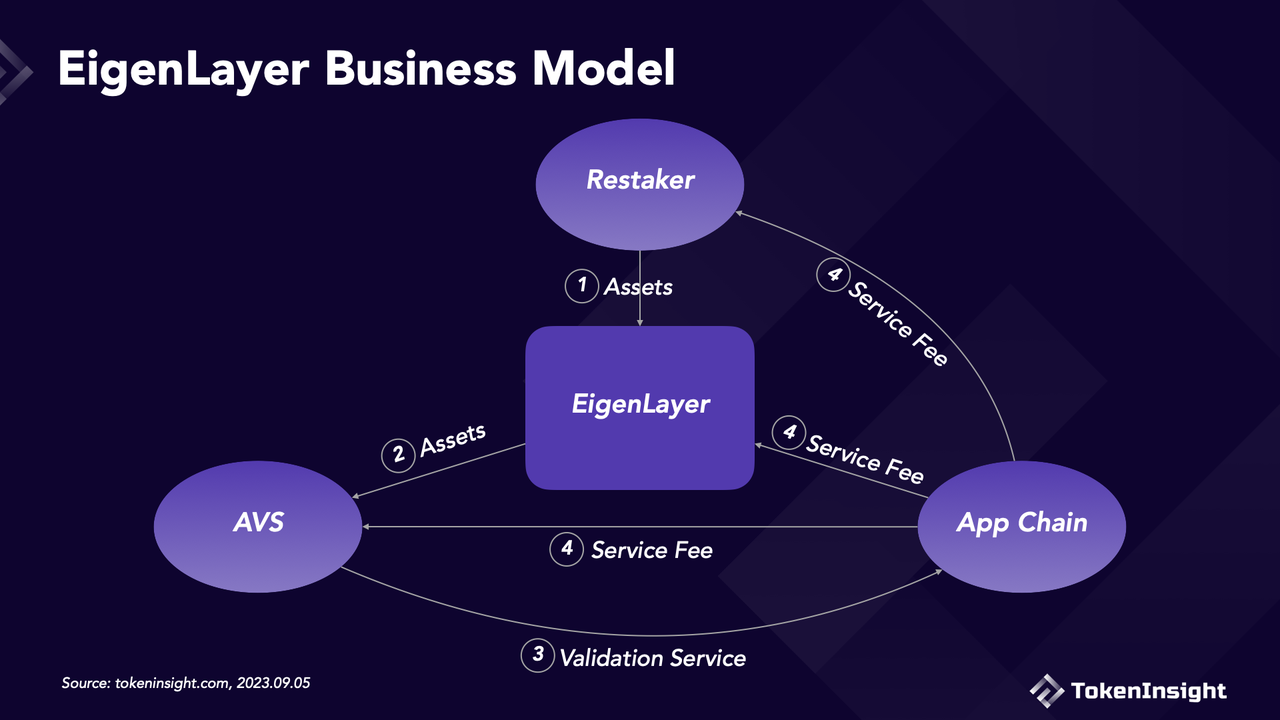

EigenLayer is a Restaking protocol based on Ethereum. It can be seen as an intermediary platform connecting Stakers, AVS, and Application chains.

The main role of EigenLayer is to act as a platform connecting these three entities. It can:

EigenLayer's business model is built around Stakers, AVS, and Application Chains. From the perspective of demand and supply:

The specific operational process of EigenLayer's business model is as follows:

From the business model perspective, EigenLayer's main customer base is small to medium-sized blockchain networks with validation requirements. It primarily facilitates Ethereum's node operators to provide validation services to non-EVM-compatible blockchain networks.

Within this entire business chain, whether it's the stakers, AVS, or EigenLayer, their revenue ultimately depends on these application chains. Therefore, when evaluating whether EigenLayer's business model can be profitable, the first question to address is whether there will be application chains willing to use EigenLayer.

Firstly, the fundamental reasons why EigenLayer might attract small to mid-sized non-EVM compatible application chains as its main customer base are twofold:

Non-EVM-compatible application chains need to establish their own trust networks and ensure network security by deploying their own nodes. However, setting up their own nodes can be costly, especially for small to mid-sized blockchain networks. Hence, there's a demand for more cost-effective validation services provided by third-party node operators. EigenLayer's integrated AVS protocols can offer these application chains a more cost-competitive verification service marketplace.

For non-EVM-compatible small to mid-sized application chains, achieving the same level of security as Ethereum is highly appealing. EigenLayer claims that it can leverage LSD as collateral to provide the same level of security as Ethereum. This will undoubtedly address a pain point for these application chains.

From a cost perspective, EigenLayer indeed caters to the need of small to mid-sized application chains to reduce node deployment costs. However, in terms of security, it's arguable whether EigenLayer can truly "borrow" Ethereum's security to provide the same level of security as Ethereum.

Regarding the staking mechanism, EigenLayer primarily uses LSD as collateral to provide protection for AVS. But this doesn't necessarily imply that the validation services offered by AVS can provide the same level of security as Ethereum. Ethereum's robust security is derived from its large number of nodes and the amount of ETH staked. It boasts over 10,000 nodes and 25 million ETH staked, making its network highly secure. On the other hand, the validation services purchased by application chains from EigenLayer won't match Ethereum's equivalent levels in terms of node count and staked assets. Hence, EigenLayer can't fully address the security pain points of customers.

Furthermore, from a sustainability perspective, small to mid-sized application chains won't be using EigenLayer for an extended period. In their early stages of development, these application chains may opt to purchase AVS services from EigenLayer due to cost considerations. However, as they progress into the mid to late stages of development and issue their own native tokens, there's a high likelihood that they will transition to using their native tokens as collateral and build their own secure networks. This transition is inevitable for the growth of blockchain networks.

Hence, for the reasons outlined above, the number of customers EigenLayer can attract won't be substantial, and there's a significant likelihood that this number will gradually decrease in the future.

For AVS, the potential income they can earn from the application chains is a significant reason to join EigenLayer.

Essentially, AVS integrated into EigenLayer are earning extra income. They are performing additional verification work on EigenLayer, on top of their Ethereum validation duties. But how much additional income can they generate from this extra work?

If we refer to Lido Finance's data, AVS joining EigenLayer can earn revenue in the range of 5%-10% of the service fees. Lido charges a 10% fee, which is divided between node operators and Lido itself, with 5% going to node operators. However, since EigenLayer is in its early stages, there's a high probability that they will implement incentives to attract AVS by offering them a larger share of the fees.

However, while EigenLayer brings additional income to these node operators, the extra validation work also increases the security risks for validation nodes. Vitalik Buterin has expressed similar concerns about this. He believes that EigenLayer's practice of using Ethereum node operators to validate other blockchain networks could lead to an overload of the Ethereum network's consensus. The restaking mechanism could compound attack risks and potentially affect the overall security of the network.

Therefore, we believe that in the early-stage AVS may be attracted due to the income, but considering the accompanying security risks, the overall situation for AVS entering EigenLayer may not be very optimistic. In other words, the additional income they receive from application chains might not be sufficient to compensate for potential losses.

Users choose to stake assets in EigenLayer mainly because of the staking rewards they can earn from restaking and potential airdrop rewards in the future.

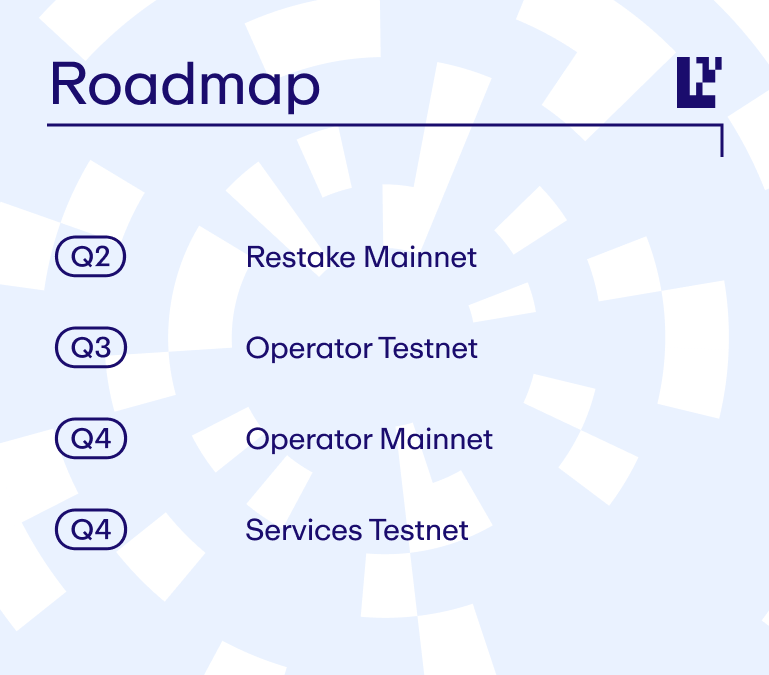

According to EigenLayer's roadmap, EigenLayer is currently in the first stage: Restake Mainnet, which only offers the platform's restaking functionality. Node staking based on LSD assets and AVS services are not yet available. This means that users can only deposit assets into EigenLayer at the moment, but there are no staking rewards available. Additionally, for a significant period in the future, until the Service phase is opened, users will not receive any staking rewards.

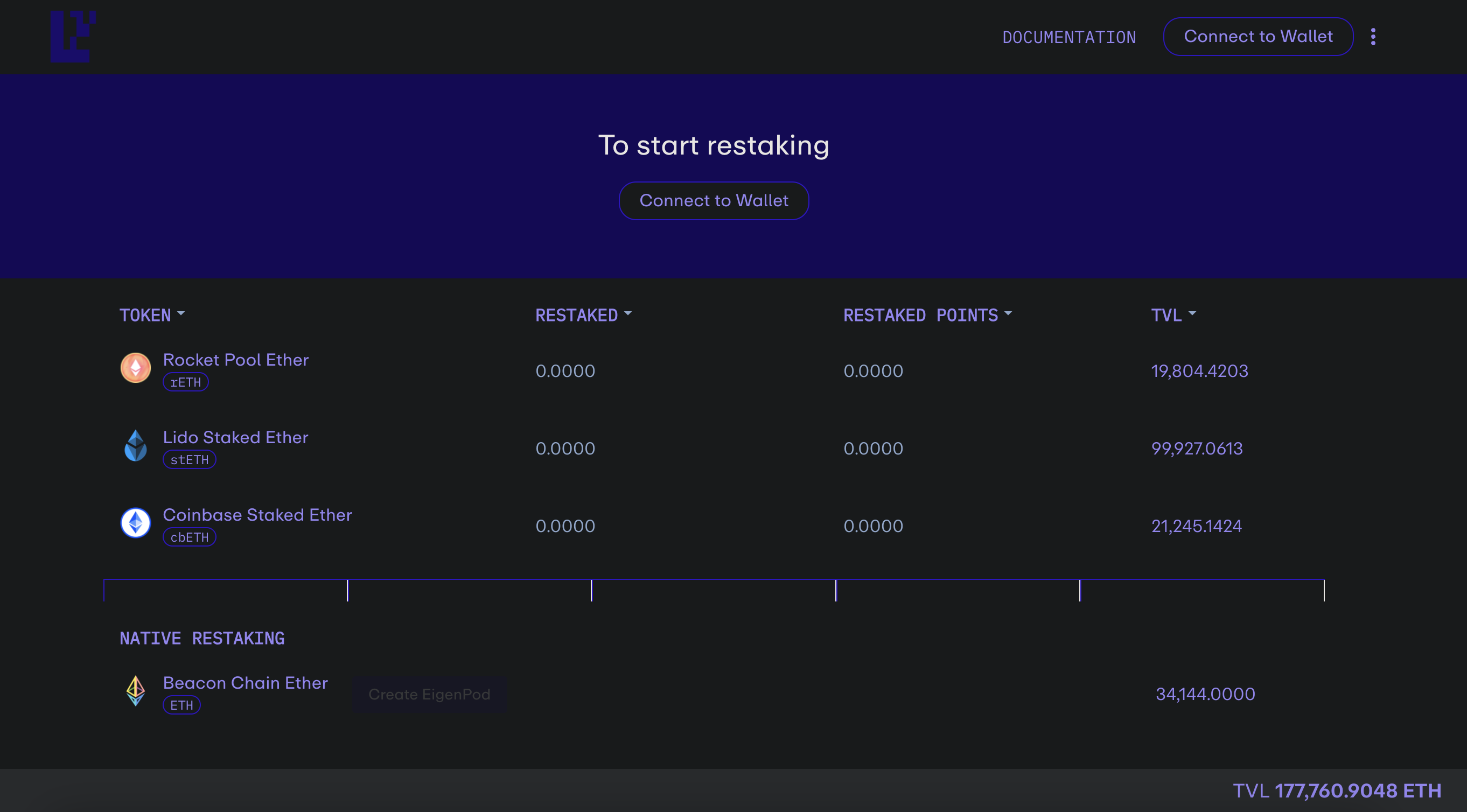

However, according to data from EigenLayer's official website, there are currently quite a few users staking assets on the platform. In just over two months since the launch of the mainnet staking feature, EigenLayer's total staking amount has exceeded 177K ETH. A significant portion of this is likely due to users hoping to become early supporters of the project to receive potential future airdrop rewards. However, this kind of promise to attract users with potential rewards, while effective in the early stages, can lose its appeal over time. After all, users can not receive any substantial returns in the short term, and this is the most critical issue for EigenLayer.

Furthermore, looking at it from a long-term perspective, LSD holders can easily find node operators to stake their assets with without using EigenLayer. EigenLayer essentially eliminates the step of users having to search for this information themselves by providing a platform that connects them with node operators. So, unless EigenLayer offers staking rewards that are significantly higher, it may not be able to attract a large number of users to continue staking assets on its platform.

Therefore, we believe that while there are currently quite a few users staking assets on EigenLayer, the potential for a significant increase in the number of users in the future is limited.

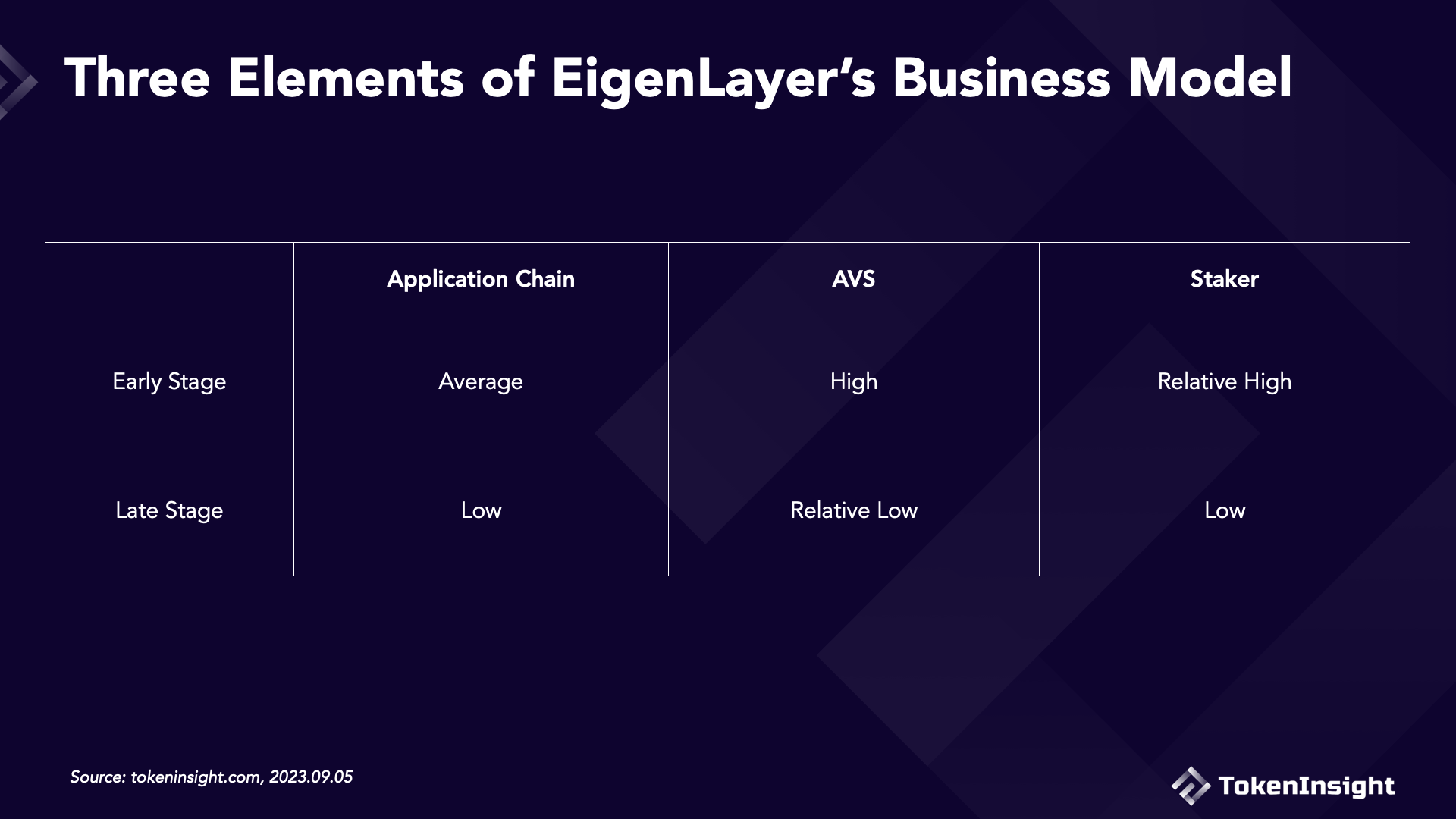

In summary, for EigenLayer, the three key elements of application chains, AVS, and users are all essential.

Therefore, we believe that EigenLayer, as a king project in restaking, may have been overly hyped and overestimated. Its business model may not be sufficient to sustain profitability once the initial excitement wanes.

APP

APP