The conventional explanation for gold’s rally focuses on macro conditions: real rates, the dollar, fiscal risk, and geopolitical uncertainty all matter. But they do not fully explain the durability and composition of this cycle. This article adds a market-structure lens, arguing that gold’s bid has become stratified across three distinct cohorts: central banks, private capital, and crypto-native balance sheets. Each cohort buys gold for a different reason, responds to different signals, and reinforces the cycle in a different way.

The conventional explanation for gold’s rally focuses on macro conditions: real rates, the dollar, fiscal risk, and geopolitical uncertainty all matter. But they do not fully explain the durability and composition of this cycle. This article adds a market-structure lens, arguing that gold’s bid has become stratified across three distinct cohorts: central banks, private capital, and crypto-native balance sheets. Each cohort buys gold for a different reason, responds to different signals, and reinforces the cycle in a different way.

Gold’s behaviour as a macro hedge is widely documented but often poorly decomposed. The conventional framing describes what gold tends to do inside a portfolio: it is duration-light, inversely exposed to confidence in fiat balance sheets, sensitive to real rates and the dollar, and convex to geopolitical stress. What that framing often misses is a more important market-structure question: who has been buying, in what size, and for what reason?

That distinction matters because the marginal buyer determines the durability of a cycle. The 2022–2026 gold repricing is unusual not simply because price rose sharply, but because the bid rotated across three structurally different cohorts while remaining additive rather than substitutive. Central banks, allocation-driven private capital, and crypto-native balance sheets have all participated, but they do not share the same objective function, investment horizon, regulatory regime, or price sensitivity.

This article decomposes gold demand by purpose of holding rather than by chronology. The three cohorts overlap in time, but their demand functions are independent enough to treat them separately. The central conclusion is straightforward: gold’s repricing has not been driven by a single macro variable. It has been driven by a layered demand stack in which a policy-driven official-sector floor was later reinforced by private capital reallocation and, at the margin, by a new crypto-native balance-sheet channel.

Incremental supply has not been elastic enough to absorb this combination of demand without a higher clearing price. Mine output adjusts slowly, recycling responds only after a sufficiently large price move, and above-ground holders require compensation to part with inventories. As a result, when structurally distinct buyer groups compete for the same physical asset at the same time, the market clears primarily through price rather than through rapid supply expansion.

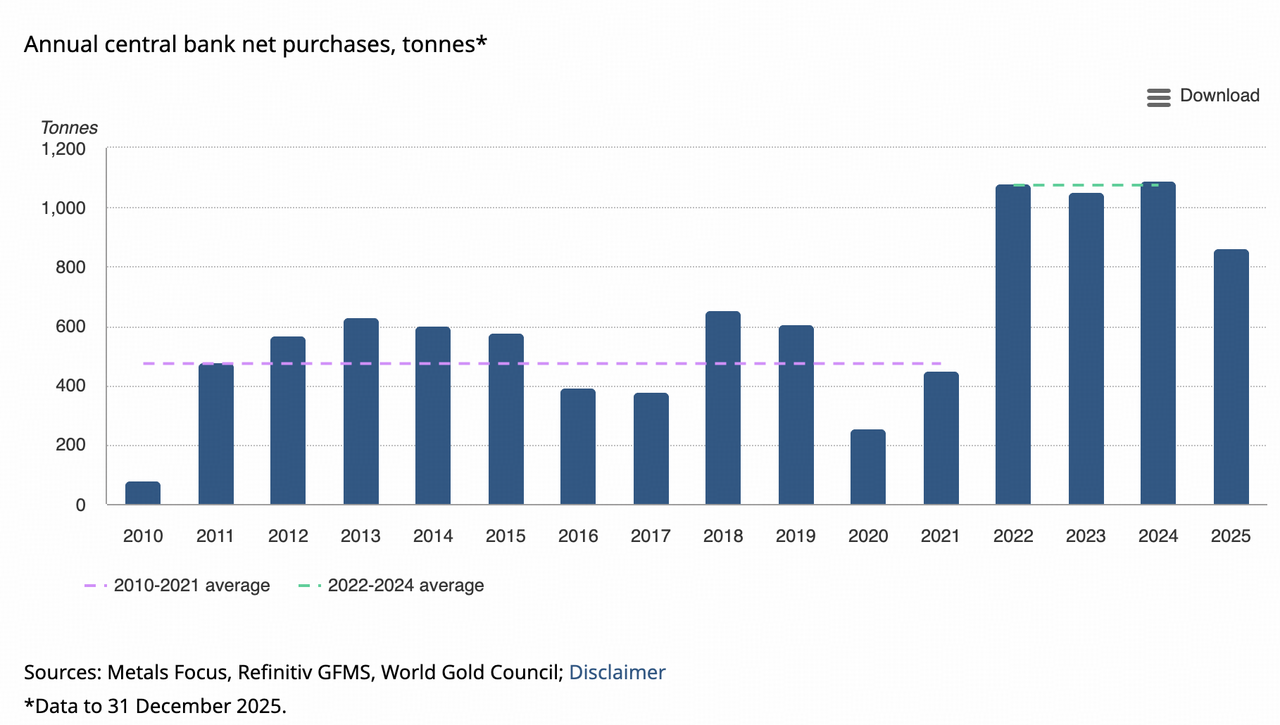

The foundation of this cycle was laid by central banks before the meaningful return of ETF and Western retail flows. Official-sector gold purchases exceeded 1,000 tonnes in each of 2022, 2023, and 2024. The three-year cumulative total was roughly 3,220 tonnes, more than double the 2014–2016 total of approximately 1,576 tonnes. The 2022 print of 1,136 tonnes was the highest annual figure in the modern series beginning in 1950.

Gold purchased by Central Bank

For context, the 2010–2021 annual average was approximately 473 tonnes. The 2022–2024 cluster therefore represented roughly 2.3 times that baseline. Even after the 2025 slowdown, official-sector purchases remained around 1.8 times the 2010–2021 average and ranked among the strongest annual reserve builds on record.

The structural feature that makes this cohort a floor is not that central banks are completely price-insensitive. They are not. At sustained elevated prices, the marginal cost of further diversification rises, especially for central banks where gold already represents a high share of total reserves. The 2025 deceleration is consistent with that long-run price sensitivity.

The more important point is that central-bank demand is low-turnover and mandate-driven. Reserve allocation is governed by foreign-exchange composition, sanctions risk, geopolitical fragmentation, domestic political preference, and de-dollarisation calendars. Mark-to-market P&L is not the primary decision variable. Gold is treated as a strategic reserve asset, not a tactical trade.

That explains the 2022–2024 anomaly that challenged legacy gold models: prices rose even as ETF holdings declined. The marginal bid was not coming from Western portfolio allocators. It was coming from the official sector.

In 2025, central-bank purchases moderated to approximately 863 tonnes, down around 21% year over year and the lowest annual figure since 2021. But the slowdown should not be misread as a collapse in demand. It was still an historically large number. Meanwhile, a large share of official-sector accumulation continued to appear outside immediately reported IMF data, suggesting that some central banks still prefer to build gold exposure without full real-time visibility.

The forward path is therefore nuanced. The official-sector bid is likely to moderate from the extraordinary 2022–2024 pace if spot prices remain elevated. But survey evidence and revealed behaviour suggest that the reserve-diversification floor remains intact.

The second bid arrived more visibly in 2025 with the re-engagement of ETF, bar-and-coin, and institutional allocation flows. Global gold ETF holdings increased by approximately 801 tonnes over the year, reversing roughly three years of net outflows that had previously obscured the strength of the underlying market.

Global Gold ETFs Flows

Source: https://www.gold.org/goldhub/data/gold-etfs-holdings-and-flows

The key interpretive point is that ETF flows stopped being the marginal demand signal during 2022–2024. In prior cycles, Western ETF holdings were often treated as the cleanest proxy for investment appetite. That framework failed when ETF liquidation coexisted with rising spot prices. The missing variable was official-sector accumulation.

By 2025, the cycle broadened. Sovereign accumulation continued, but private capital began layering incremental demand on top. Total annual gold demand exceeded 5,000 tonnes for the first time in the available series, while bar-and-coin demand remained strong across several jurisdictions. This was not a baton-pass from central banks to private investors. It was a stacking of demand functions.

The allocation gap is the most important variable for this cohort. Gold ETFs remain a very small share of US private financial assets, estimated at around 0.17%. That is well below the 1–2% allocation often discussed in diversified institutional portfolios. A move to even 0.5% would imply substantial incremental gold-equivalent demand.

This cohort differs sharply from central banks. Private capital is more price-sensitive and macro-sensitive. It responds to real yields, dollar direction, equity drawdown risk, fiscal credibility, and portfolio correlation regimes. But it is also allocation-anchored. A strategic reallocation into gold does not need a new buyer category to emerge. It can occur entirely through existing wealth-management, ETF, pension, family-office, and institutional channels.

The practical implication is that this cohort carries the largest near-term upside in absolute tonnage. If real yields decline, the dollar weakens, fiscal-risk premia rise, or equity-bond diversification fails again, private capital has both the motive and the available balance sheet to rebuild gold exposure.

The third cohort is the smallest by tonnage but the most novel in mechanism. It sits inside crypto-native financial infrastructure and introduces a demand channel with no direct analogue in prior gold cycles.

This cohort should not be overstated. It is not yet large enough to rival central banks or ETFs as a price-setting force by mass. Its significance lies elsewhere: it changes the topology of gold demand. Gold is no longer only a reserve asset, jewellery input, ETF exposure, or OTC macro hedge. It is increasingly being incorporated into stablecoin balance sheets, tokenised collateral systems, and on-chain structured products.

The crypto-native bid has three sub-components.

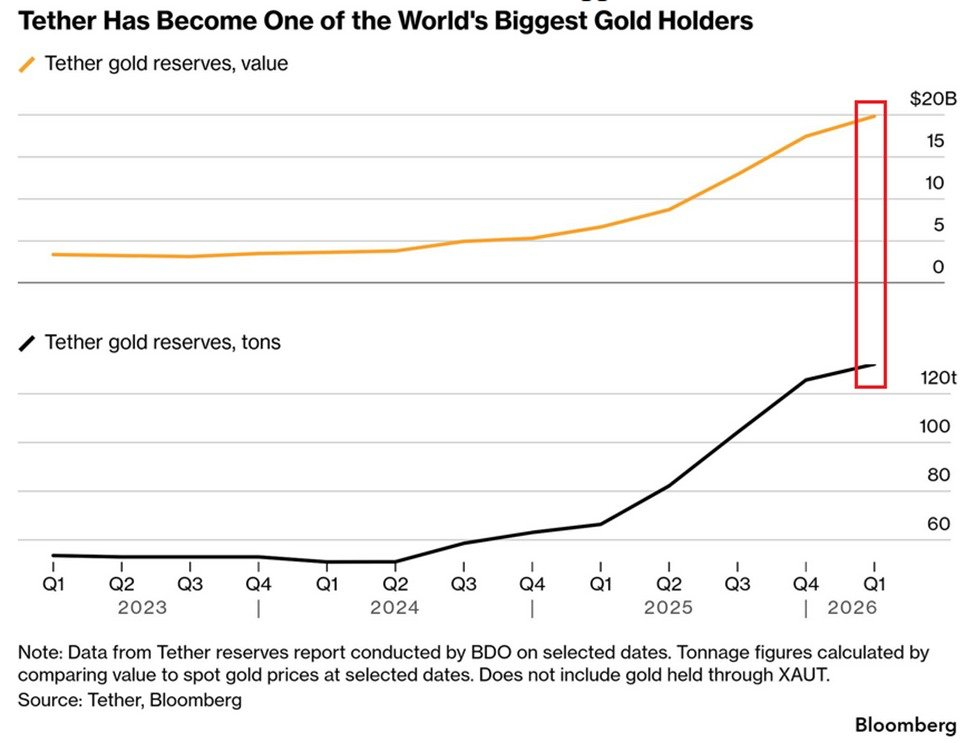

The largest near-term contributor within this cohort is stablecoin reserve growth, and within that category Tether is the central actor.

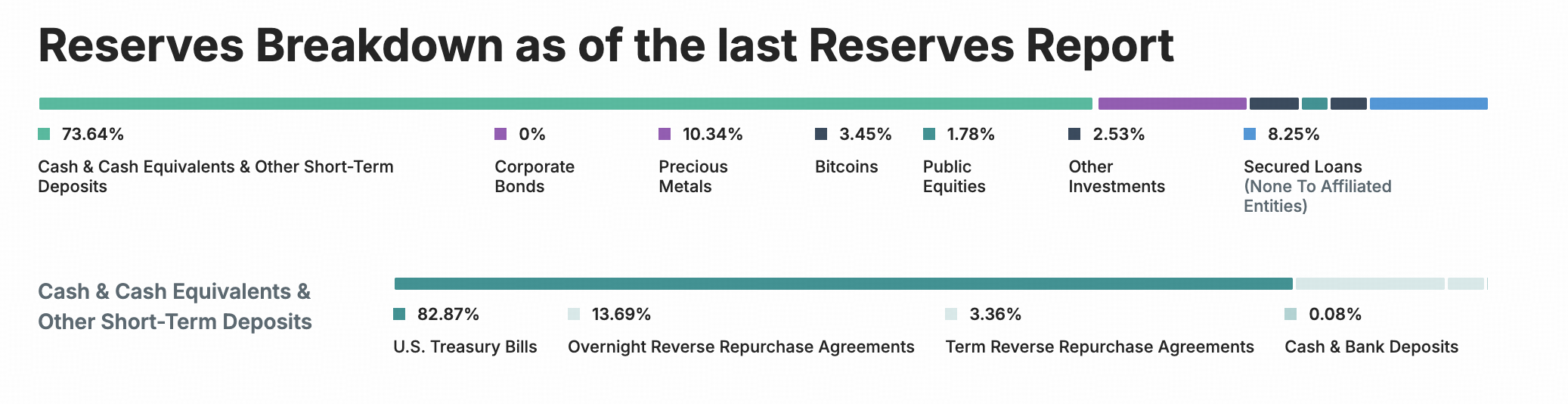

As of its Q1 2026 disclosure, Tether reported approxiately $183 billion of USDT liabilities and a reserve base still dominated by short-duration US Treasury exposure. The company’s direct and indirect Treasury exposure was approximately $141 billion. Alongside that Treasury-heavy reserve structure, Tether has also held meaningful exposure to physical gold and Bitcoin.

Tether USDT's Reserve

These figures should be interpreted carefully. The key analytical distinction is between USDT reserves, Tether group capital, excess reserves, and the separate gold backing of Tether Gold, or XAUT. Combining them without qualification can overstate the precision of the gold-demand estimate. Still, the broad conclusion is robust: Tether has become a meaningful non-sovereign holder of physical gold, and its reserve behaviour matters at the margin.

The mechanism is important. Tether’s gold demand is not conventional portfolio allocation. It is linked to the growth of USDT liabilities and the company’s reserve-management preferences. When offshore dollar liquidity demand rises, USDT circulation can expand. When USDT liabilities expand, Tether must allocate reserves. If the company continues to hold a material share of reserves or excess capital in gold, then stablecoin growth transmits into physical gold demand.

This creates a new channel:

crypto dollar liquidity demand → USDT issuance → reserve allocation → physical gold accumulation

That channel did not exist in previous gold cycles.

The regulatory backdrop makes the mechanism more important. The US GENIUS Act framework restricts compliant payment stablecoin reserves to highly liquid dollar assets such as cash, bank deposits, short-dated Treasuries, qualifying repo or reverse repo arrangements, government money-market funds, and similar approved instruments. Gold and Bitcoin are not eligible reserve assets under that framework.

This creates a bifurcation in stablecoin balance sheets. Growth in US-compliant stablecoins such as USDC should primarily translate into demand for the front end of the Treasury curve. Growth in Tether, to the extent its current reserve philosophy persists, may continue to include some gold and Bitcoin exposure. The two issuer regimes therefore have different balance-sheet effects.

This point should not be pushed too far. Tether’s allocation is not a mechanical formula in which every new dollar of USDT is automatically split into a fixed reserve mix. Reserve composition can change with regulation, redemption risk, profitability, interest rates, custody considerations, and management preference. But the existence of the channel is itself important. It links offshore stablecoin demand to the physical gold market through a corporate balance sheet rather than through ETF subscription flows.

Tokenised gold has moved from niche experiment to a visible, though still small, segment of the gold market. These products typically represent blockchain-based claims on allocated physical bullion held in audited vaults. The leading instruments, including Tether Gold and Paxos Gold, account for the overwhelming majority of circulating supply.

The tonnage remains small. It is not a macro driver when official-sector demand is measured in hundreds of tonnes and ETF flows can move by similar magnitudes in a single year. The structural function matters more than the current mass.

Tokenised gold converts a vault-bound asset into programmable collateral. It can be transferred across borders with blockchain settlement, posted in selected DeFi venues, integrated into on-chain structured products, used as margin in crypto-native derivatives, or held by users who want gold exposure without traditional brokerage or ETF rails.

That said, trading volume should not be confused with net physical demand. Reported tokenised-gold turnover can be large, but turnover includes secondary trading, arbitrage, exchange activity, and routing across venues. The physical gold impact comes from net minting and redemption, not gross trading volume. For gold-market balance purposes, tokenised gold should be analysed through changes in underlying bullion backing rather than headline volume alone.

Tokenised gold is not yet a dominant source of incremental tonnage, but it is an important market-structure innovation. It expands the set of use cases for physical gold from “store of value” to “digitally mobile collateral.”

The most experimental sub-layer is yield-bearing tokenised gold. The basic mechanism is familiar to commodity and structured-product investors: hold a spot gold claim through a tokenised instrument, hedge price exposure through futures or forwards, capture carry when the curve and financing conditions permit, and potentially add incremental return by lending tokenised positions into crypto-native credit venues.

The conceptual appeal is clear. Gold is traditionally a non-yielding asset. If tokenisation and derivatives hedging can convert gold into productive collateral, the addressable investor base broadens.

But the implementation risk is substantial. The structure inherits several frictions that plain gold exposure does not have:

Therefore, the main problem is whether the yield remains attractive after hedge slippage, custody fees, basis volatility, smart-contract risk, and the capital cost of maintaining the structure. For now, yield-bearing gold remains the smallest and most experimental part of the crypto-native demand stack. It is more important as a signal of product direction than as a current driver of physical demand.

The three-cohort framework produces a directional rather than point forecast.

Cohort 1 is likely to remain a floor, but not necessarily at the extraordinary 2022–2024 purchase rate. Elevated spot prices are already creating more discipline among central banks. The relevant question for 2026 is not whether central banks continue to buy. It is whether purchases remain materially above the pre-2022 baseline. If they do, the official sector continues to reduce downside elasticity.

Cohort 2 carries the largest near-term upside in absolute tonnage. Western investors remain under-allocated relative to common strategic allocation benchmarks. If real rates fall, the dollar weakens, equity volatility rises, or fiscal-risk premia continue to build, ETF and institutional demand can expand without requiring a new buyer class. The 2025 ETF inflow showed that private capital can re-enter rapidly once the macro narrative and price momentum align.

Cohort 3 is unlikely to rival the first two cohorts by tonnage over a 12-month horizon. Its importance lies in optionality and market structure. Stablecoin balance sheets create a new reserve-management channel. Tokenised gold makes physical bullion more composable as collateral. Yield-bearing structures experiment with turning gold into a productive asset. These mechanisms may remain small in mass while still being meaningful for the composition of marginal demand.

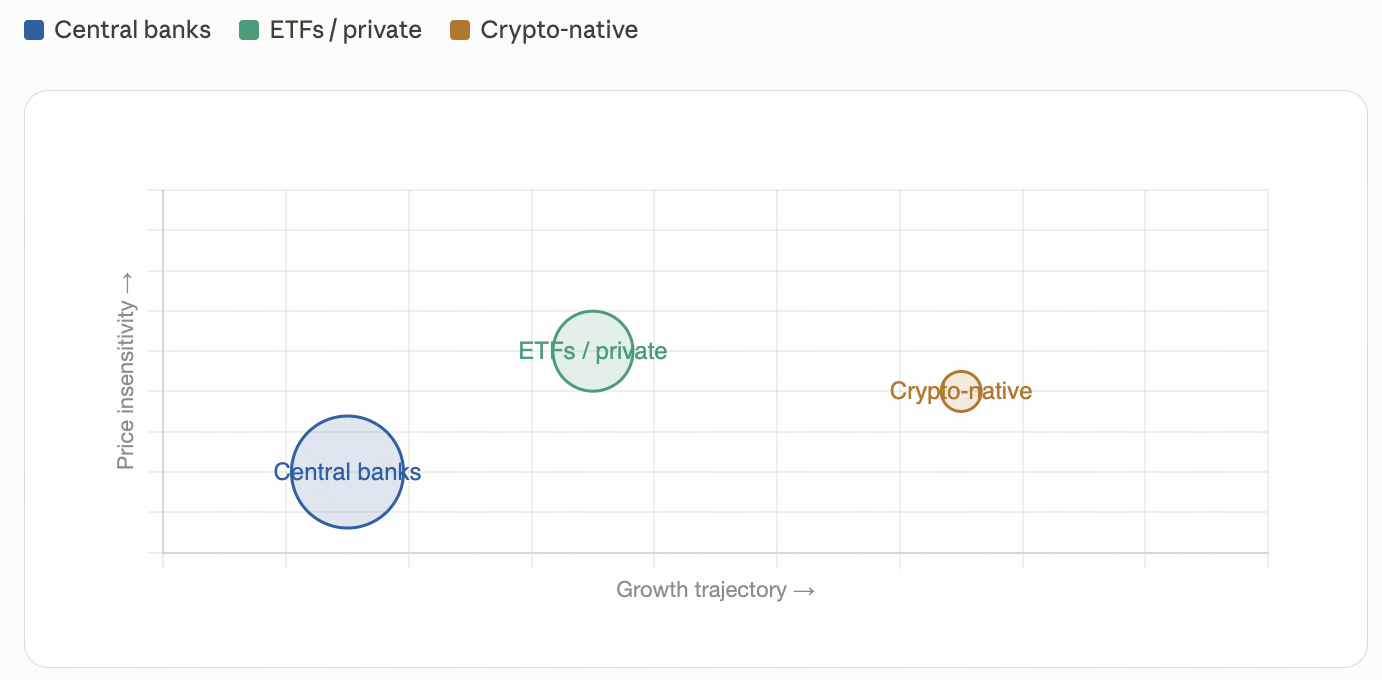

The strategic value of this decomposition is that each cohort responds to different signals, has a different growth ceiling, and is controlled by a different decision authority.

Cohort comparison: scale, sensitivity, and trajectory

The central implication is that gold is no longer being repriced by a single macro story. It is being repriced by the intersection of reserve politics, portfolio allocation, and digital collateral architecture. That makes historical analogies to 1979 or 2011 analytically incomplete. Those cycles had inflation fear, real-rate repricing, and speculative flows. The current cycle has those elements too, but it also has persistent official-sector reserve diversification and an emerging crypto-native balance-sheet channel.

For the first time in the modern gold market, the marginal tonne is being competed for by buyers who do not share an objective function, do not respond to the same signals, and do not face the same regulatory regime.

That is the defining feature of the cycle.

APP

APP