Currently, there are at least 5 protocols building on top of GMX's $GLP for the "real ETH yield" it offers. Among all of them, JonesDAO's jGLP & jUSDC vault is the new player and is performing well. According to @defimochi' dashboard, jGLP has taken over 28% GLP shares since launching on late January 2023, in addition to lots of shares of Mugen and Plutus.

So what is jGLP and how does it attract such an amount of GLP so fast? In this article, we're going to breakdown the basic mechanism of jGLP and jUSDC vault into detail.

Currently, there are at least 5 protocols building on top of GMX's $GLP for the "real ETH yield" it offers. Among all of them, JonesDAO's jGLP & jUSDC vault is the new player and is performing well. According to @defimochi' dashboard, jGLP has taken over 28% GLP shares since launching on late January 2023, in addition to lots of shares of Mugen and Plutus.

So what is jGLP and how does it attract such an amount of GLP so fast? In this article, we're going to breakdown the basic mechanism of jGLP and jUSDC vault into detail.

Previously called DAOJones, Jones DAO is a yield strategy protocol built on Ethereum and Arbitrum.

Its main yield mechanism is building types of vaults that execute different strategies. Currently it provides three types which are:

GMX is a leverage DEX on Arbitrum (Avalanche supported also). Anyone can provide liquidity to GMX by minting GLP. GLP is the pool token representing the liquidity position in the shared pool consisting of a mixed-basket of assets that are used for renting to traders for leverage trading.

The basket target asset split is roughly 50:50 between stable and non-stable assets. The GLP token holders (LPs) serve as the counterparty for all traders on GMX, and earn 70% from GMX protocol fee (vested weekly in $ETH, real yield!).

If you are not familar with GMX, we recommand this thread.

Note that even though the GLP token is an ERC20, it cannot be transfered or traded outside of GMX because it does not have a normal transfer contract (GLP contract on Arbitrum). It can only be utilized to redeem the assets locked during the minting process. However, stakedGLP can be transferred like any regular ERC20.

In GMX, the 50% stable asset composition allows traders to short any basket asset, meanwhile offset potential volatile risk for LPs (GLP holders). But this may discourage LPs to provide liquidity since all stables are opportunity cost for them. Because they can easily find more attractive yield opportunities when they anticipate the market is in an upward trend.

If you want to know more about what could happen to GMX in the bull market, here is an interesting deep dive discussing by our colleague @QuantumZebra. As he states, the shortingless market (bull market) makes the GLP pool less capital-efficient because the stablecoin half of the pool will be useless. Traders will only borrow $BTC and $ETH from the pool to make long bets.

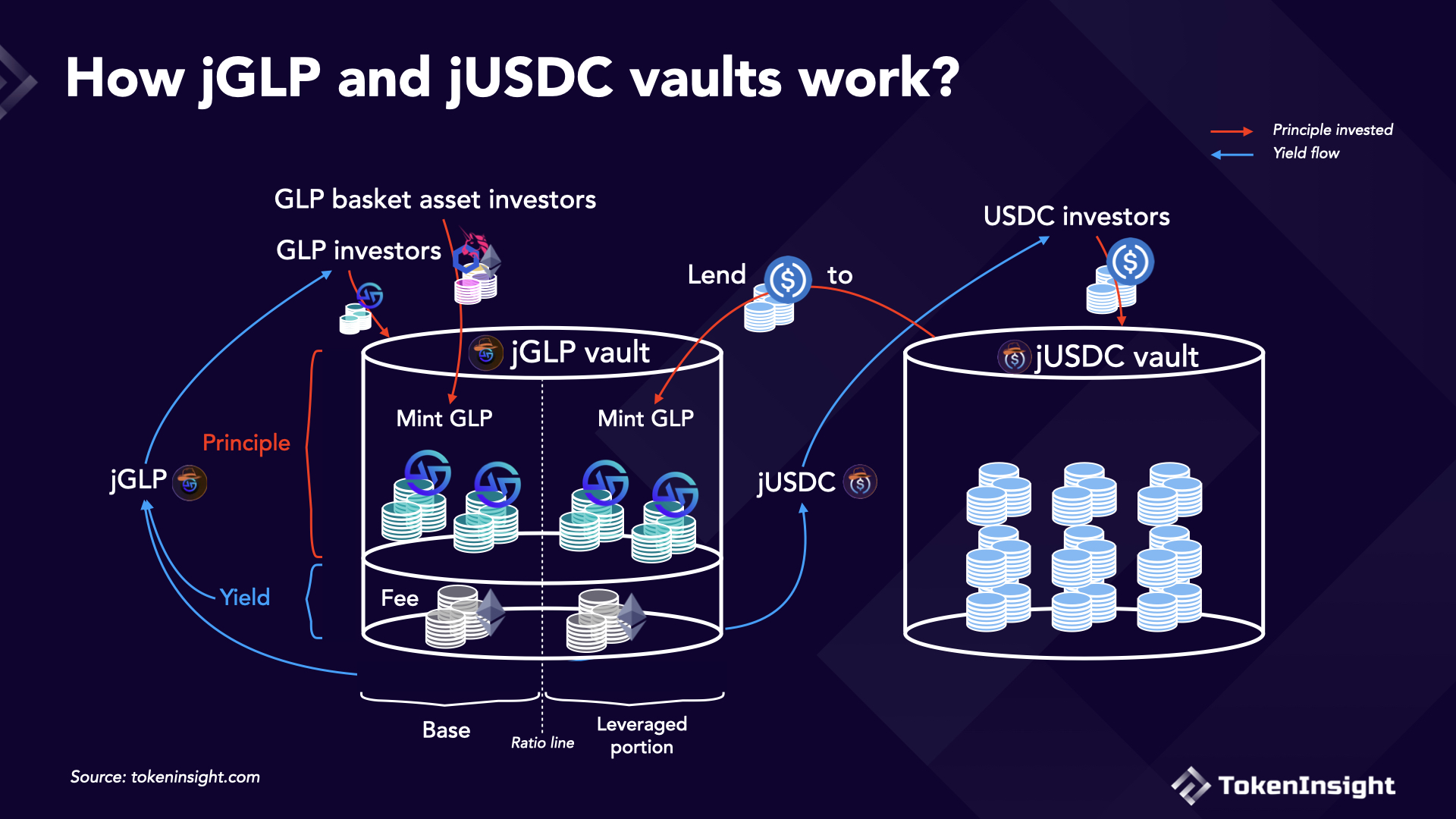

To retain liquidity providers, Jones DAO innovatively creates jGLP and jUSDC vaults. They used a so-called "over-the-counter" matching mechanism to leverage and boost GLP holders' incentives meanwhile providing a less risky yield product to $USDC holders.

jGLP vault can boost GLP stakers yield by borrowing $USDC from jUSDC vault to mint more GLP (earning more $ETH fee) and absorbing a portion of its yield.

Note that users can withdraw GLP or any GLP constituent token from the jGLP vault at any time. Vaults will help you redeem from GMX. But that will incur a fee.

Currently we cannot find the exact figure to show the exact leverage ratio, but JonesDAO has a dynamic leverage ratio moving opposite to the market trends. When market goes down, it will move higher, and vise versa.

According to its doc, it only states "borrow $USDC within specific risk parameters, and uses targeted leverage ranges".

jUSDC vault is the liquidity source of jGLP leverage. This vault is suitable for risk averse users. Because its stables-staking yield is higher than the interest rate in lending protocols like AAVE or Compound.

Note that users can signal their intent to withdraw $USDC from the jUSDC vault, and will be available for withdrawal 24 hours later.

jGLP stakers will earn yields mostly from three sources:

Advanced incentives: autocompounding rewards and withdraw punishment

Withdrawing from jGLP need to pay 3% of your total position. Of which, 1/3 will be distributed to other stakers as reflexive incentives. 2/3 will be distributed to stakers who selected auto-compounding (who hold jGLP receipt token)

jUSDC stakers will earn yields mostly from leveraged portion yields. jUSDC stakers also need to pay 0.97% of his/her position size fee to withdraw to other jUSDC stakers as retention incentives.

But the remained jUSDC stakers' actual received retention incentives are the difference between the above amount and the cost of burning GLP to $USDC from GMX. When the cost is more than the 0.97%-fees, there will be no retention incentives occurs.

Note that when exiting $USDC from jUSDC vault, the first liquidity source is from unused $USDC in jUSDC vault. Any further withdrawls need to burnt GLP in GMX.

Keep in mind that the mechanism shows that "jGLP + jUSDC" does not eliminate any opportunity costs or counterparty risks of GLP, rather it only amplifies the yield of directly holding GLPs, by borrowing money from other risk-averse users hands.

In this way, JonesDAO can gain more GLP by providing attractive yields, meanwhile offer a relatively high yield product for risk-averse users.

But for the latter (jUSDC depositors), they actually indirectly bear the liquidity risk of holding GLP, as their own $USDC is taken for mint GLP without getting 100% of that risk premium (most of which is taken by jGLP) but only a fraction of it. If GMX does experience a fomo squeezing on $USDC redemptions, jUSDC holders will be affected seriously.

As for whether the portional risk premium can cover the risks they are bearing, we still lack data support. The official docs and whitepaper are lack of leverage ratio data and detailed fee structure. So DYOR and excerise carfully. We will keep digging.

APP

APP