5m

5m

Ethereum Exchange-Traded Funds (ETFs) have emerged as a major bridge between traditional finance and the crypto market, offering investors exposure to ETH without the complexities of self-custody or blockchain transactions. Unlike retail investors who buy and store ETH directly, institutions prefer regulated, easily accessible financial instruments. Spot Ethereum ETFs, approved in mid-2024, marked a pivotal moment by allowing traditional market investors to gain direct exposure to ETH.

One major limitation of current Ethereum ETFs is the lack of staking—a feature that differentiates ETH from Bitcoin. Ethereum transitioned to a proof-of-stake (PoS) consensus model with the Merge in 2022, allowing ETH holders to earn rewards by securing the network. However, existing ETFs do not stake their holdings, meaning investors miss out on these additional yield opportunities.

Recent developments suggest this may soon change. In February 2025, the Cboe BZX Exchange filed a request with the SEC to allow staking within the 21Shares Core Ethereum ETF, potentially setting a precedent for other issuers. If approved, Ethereum ETFs could generate passive income through staking rewards, making them more attractive to institutional investors.

The introduction of staking-enabled Ethereum ETFs could be a major catalyst for the crypto market. If institutions can earn yield on their Ethereum holdings through regulated ETFs, it could drive massive inflows similar to what we saw with Bitcoin ETFs. Additionally, with more ETH being locked in staking, supply-side pressure could further boost ETH’s price.

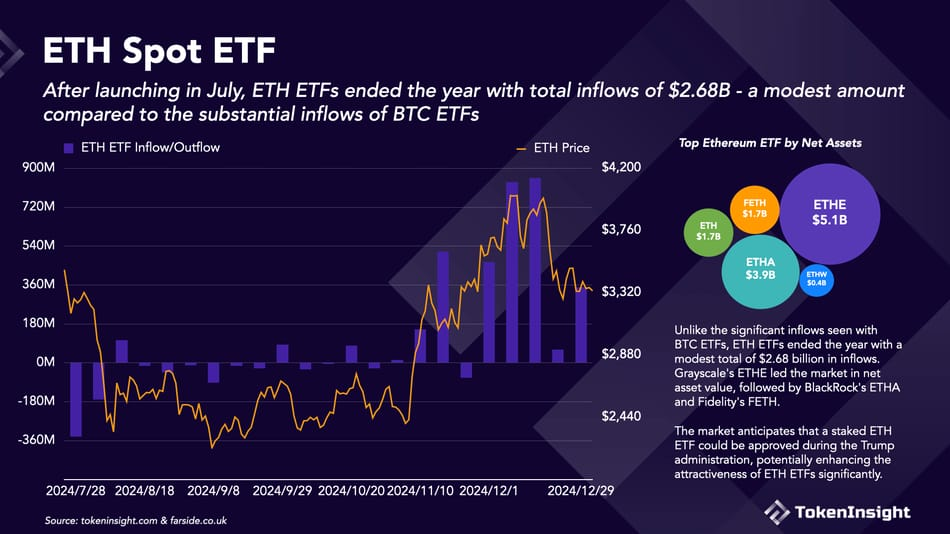

The approval of spot Ethereum ETFs in July 2024 was expected to be a transformative moment for institutional adoption. Major asset managers—including BlackRock, Fidelity, Grayscale, and VanEck—secured regulatory approval to launch ETFs that directly hold ETH, mirroring the success of spot Bitcoin ETFs earlier that year.

However, Ethereum ETFs have failed to generate the same level of inflows as their Bitcoin counterparts. While Bitcoin ETFs saw billions of dollars in net inflows within weeks, Ethereum ETFs have struggled to attract similar institutional interest. Analysts point to multiple reasons, but one key factor is the lack of staking rewards. Unlike Bitcoin, Ethereum offers native yield through staking, making ETH more than just a store of value. Without staking, these ETFs only track Ethereum’s price, missing out on one of its most attractive features.

Source: TokenInisght

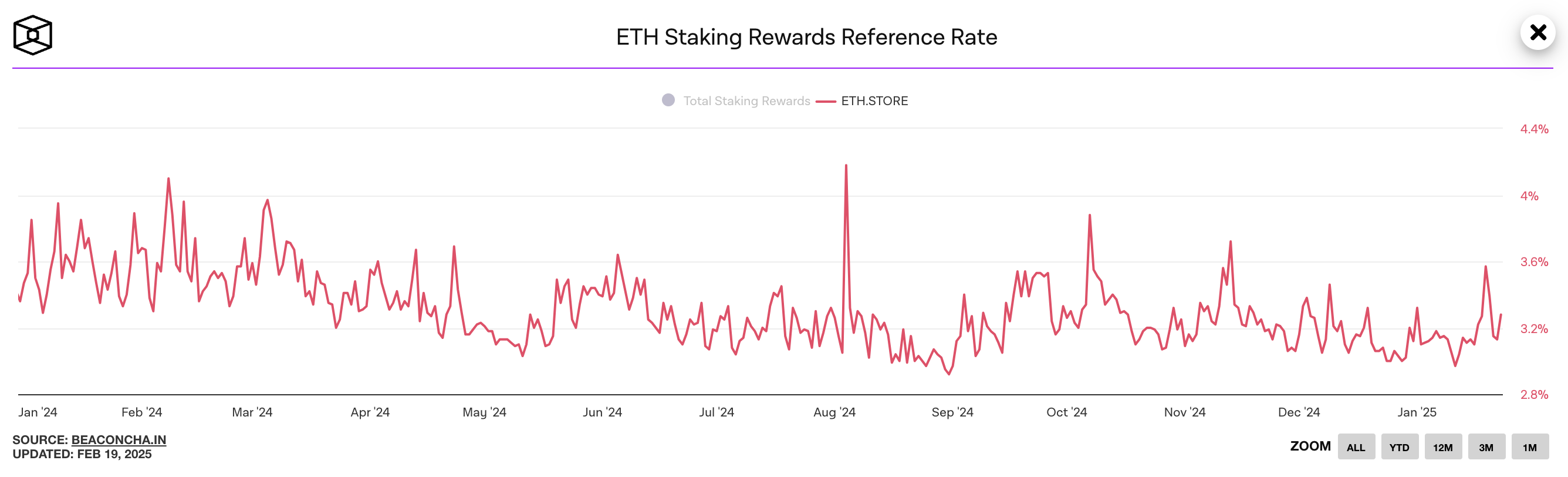

Ethereum operates on a proof-of-stake (PoS) consensus mechanism, allowing ETH holders to earn staking rewards by locking up their tokens to help secure the network.

Despite the benefits of staking, the U.S. Securities and Exchange Commission (SEC) did not permit it in the first wave of Ethereum ETFs due to several concerns:

A significant step forward came on February 12, 2025, when 21Shares, a major ETF issuer, proposed adding staking to its Core Ethereum ETF (CETH) in a filing with the Cboe exchange. This filing, which seeks SEC approval, has sparked excitement in the crypto community, with some interpreting it as a sign that staked Ethereum ETFs are imminent.

Elsewhere, staking in Ethereum ETFs already exists. In jurisdictions like Canada, Switzerland, and Hong Kong, ETFs such as the Purpose Investments Ether Staking Corp ETF (ETHC.B) and 3iQ Ether Staking ETF allow investors to earn staking rewards, typically around 3-4% annually, though yields can vary with network activity.

The introduction of staking-enabled Ethereum ETFs could be a game-changer for institutional and retail investors alike. While traditional ETFs rely solely on price appreciation, staking offers an additional revenue stream in the form of staking rewards. This not only increases the attractiveness of Ethereum ETFs but also strengthens the Ethereum network and its long-term value proposition.

One of the primary benefits of staking-enabled Ethereum ETFs is the ability to generate passive income in addition to price appreciation. Traditional ETFs rely on capital gains, dividends, or interest payments, but Ethereum staking offers a unique yield-generating mechanism where investors can earn staking rewards, typically ranging from 3% to 5% annually.

For ETF investors, this means:

Many institutional investors, such as hedge funds, pension funds, and mutual funds, have been hesitant to stake Ethereum directly due to:

A staking-enabled Ethereum ETF solves these issues by providing institutions with a regulated, hands-off solution to earn staking rewards without direct exposure to staking risks. This could unlock significant institutional capital that has remained on the sidelines due to these challenges.

Ethereum’s Proof-of-Stake (PoS) model relies on stakers to secure the network, validate transactions, and maintain decentralization. If major ETFs begin staking their ETH holdings, this could:

While staking in Ethereum ETFs offers exciting opportunities, it also introduces complex risks that must be carefully managed. Two of the biggest concerns are liquidity and redemption risks, as well as the question of who controls the staking process. Both of these factors could influence regulatory approval and investor confidence in staking-enabled ETFs.

One of the biggest challenges with integrating staking into Ethereum ETFs is the illiquid nature of staked ETH. Unlike traditional financial assets that can be bought and sold instantly, Ethereum staking requires a withdrawal process that is subject to network delays. The Ethereum protocol imposes an exit queue, meaning that when validators choose to unstake, they must wait for a certain number of blocks before their ETH is released. If the network is congested or if a large number of validators exit at once, this process can take days or even weeks.

For ETF issuers, this presents a serious issue. ETFs are structured to allow investors to buy and sell shares on demand, and issuers must be able to redeem assets accordingly. If a significant portion of an ETF’s ETH is staked and locked within the network, the fund may struggle to meet redemption requests in real-time. This could lead to liquidity mismatches, where investors expect immediate cash withdrawals but are instead forced to wait for the staking withdrawal process to complete.

To mitigate this risk, ETF issuers may need to hold a portion of their ETH unstaked to ensure liquidity for redemptions. However, keeping ETH unstaked reduces the potential yield, which diminishes one of the main advantages of staking-enabled ETFs. Another possible solution is the use of liquid staking derivatives, such as Lido’s stETH or Rocket Pool’s rETH, which allow staked ETH to remain liquid. While this could improve ETF liquidity, it also introduces additional risks, such as reliance on third-party protocols, smart contract vulnerabilities, and potential depegging issues in the event of market stress.

Beyond liquidity concerns, another major issue is how the staking process will be managed. ETF issuers have several options: they could operate their own staking infrastructure, use a centralized staking provider, or rely on a decentralized staking protocol. Each approach comes with its own set of trade-offs.

Running their own validators would give ETF issuers full control over the staking process, eliminating the need for intermediaries and reducing counterparty risk. However, managing staking infrastructure requires technical expertise, significant operational costs, and ongoing maintenance, which could make this option less appealing to traditional financial institutions.

Using a centralized staking provider like Coinbase, Kraken, or Binance would simplify the process, as these companies already have the infrastructure to stake ETH on behalf of institutional clients. However, the SEC has previously taken enforcement action against centralized staking services, arguing that they could constitute unregistered securities offerings.

Decentralized staking protocols such as Lido, Rocket Pool present a third option. These platforms distribute staking responsibilities across a network of independent validators, reducing reliance on a single centralized entity. While this approach aligns with Ethereum’s decentralization ethos, it also introduces risks related to smart contract security, governance, and liquidity.

The choice of staking method will likely be a key factor in the SEC’s decision on whether to approve staking-enabled Ethereum ETFs. Regulators may require issuers to use only approved staking providers or limit their reliance on third-party protocols.

The potential introduction of staking-enabled Ethereum ETFs could be one of the most significant developments in crypto investment products. If approved, these ETFs would provide investors with not only exposure to Ethereum’s price but also the ability to earn staking rewards, making them a more attractive option compared to traditional ETH holdings. Institutional investors who have hesitated to stake ETH due to custody, security, and regulatory concerns could finally gain passive exposure to staking yields through a fully regulated financial product.

The next few months will be crucial in determining whether Ethereum staking ETFs become a reality. The SEC is expected to review proposals from the Cboe BZX Exchange for the 21Shares Core Ethereum ETF and from NYSE Arca for Grayscale’s Ethereum Trust staking amendment. The outcome of these filings will set the tone for whether other asset managers, such as BlackRock and Fidelity, pursue similar products.

APP

APP